Beyond the Index

15+ Themes Defining India’s Next Growth Phase

Indian equity markets in mid-2026 are navigating a distinctive phase. Corporate India remains fundamentally healthy, but the opportunity set is becoming increasingly selective and capability-driven. The market’s reward system has shifted decisively: investors are gravitating toward companies with visible structural growth, differentiated technology or manufacturing depth, genuine operating leverage, and disciplined capital allocation. The era of rising-tide-lifts-all-boats is behind us. Maybe this time one has to choose the right boats that do not get destroyed by the tides…

The most striking feature of the current environment is the clear preference for B2B and industrial-facing businesses particularly companies linked to power infrastructure, data centres, industrial capex, electronics manufacturing, defence, auto ancillaries, CDMOs, and niche technology platforms. In contrast, NBFCs and some traditional B2C segments are drawing comparatively lower investor interest, reflecting a more discerning capital allocation mindset.

Several cross-cutting concerns remain on management watchlists: fuel price volatility, raw material inflation (particularly in metals and specialty chemicals), logistics disruptions, currency movements, and intermittent material availability. However, balance sheets across corporate India are demonstrably stronger than at any point in the past decade, and medium-term growth visibility remains encouraging across several structural pockets.

Five Structural Forces Shaping Indian Equities

Before diving into individual themes, it is worth articulating the five macro forces that cut across sectors and create interconnected investment opportunities:

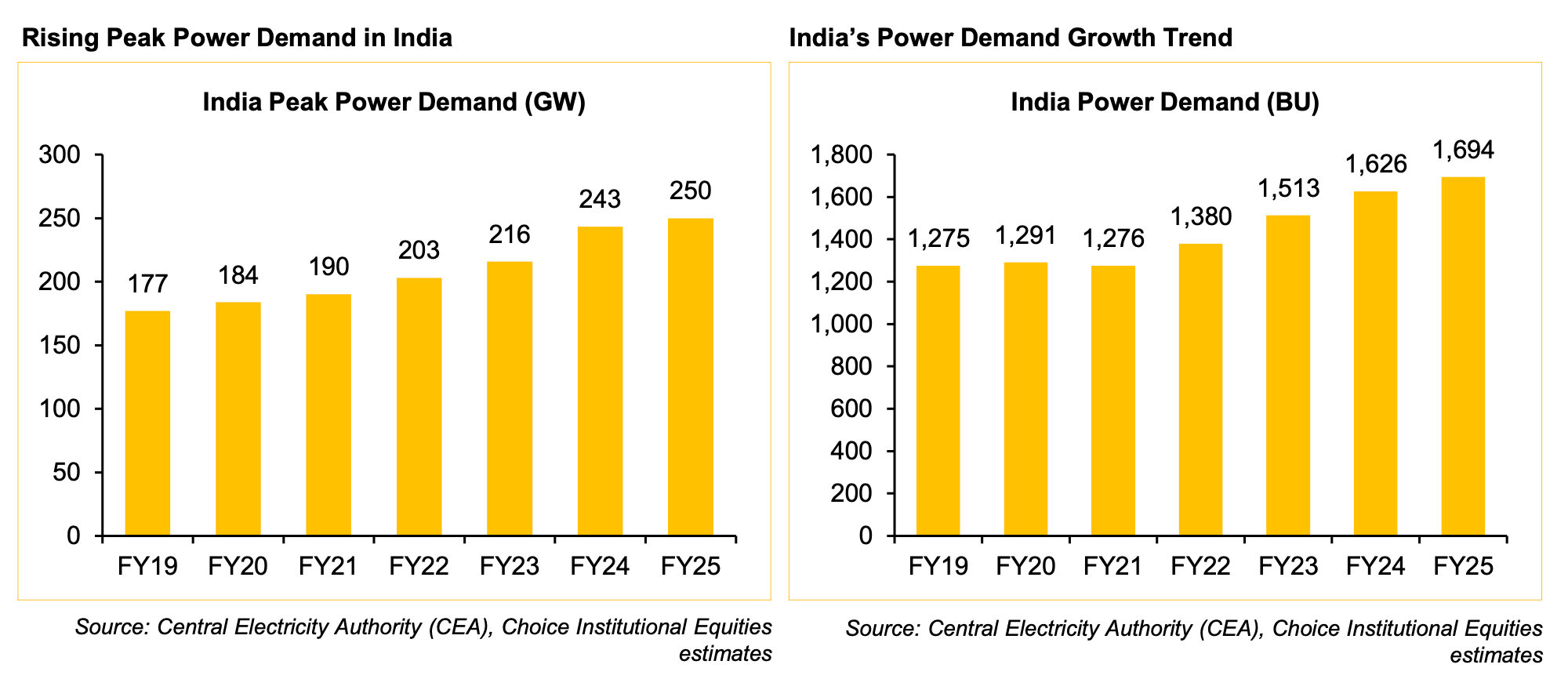

1. The Energy Infrastructure Supercycle. India’s National Electricity Plan envisages ₹9.15 lakh crore of investment to meet a projected peak demand of 458 GW by 2032. This translates into 123,577 circuit km of new transmission lines, thousands of new substations, and a fundamental upgrade of the grid from 220 kV to 400/765 kV and HVDC corridors. This is not a one-year theme — it is a decade-long structural capex cycle.

2. The China+1 Reconfiguration. Global supply chains are actively diversifying away from China across pharmaceuticals (BIOSECURE Act), electronics manufacturing (PLI 2.0), specialty chemicals, textiles, and industrial components. India is the primary beneficiary, but only for companies that have already invested in capability, quality systems, and customer relationships.

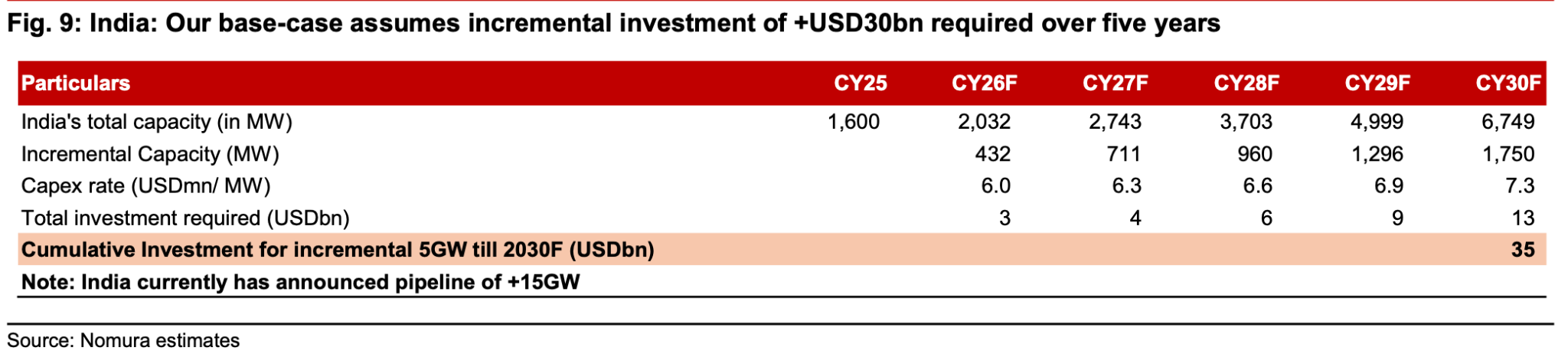

3. Digital Infrastructure Build-Out. India’s data centre capacity crossed 1,700 MW in 2025 and is projected to grow 30% YoY in 2026 with an additional 500 MW of fresh supply. The Union Budget 2026-27 introduced a tax holiday till 2047 for eligible foreign cloud service providers. Global data centre investments are projected to exceed $180 billion in 2026. This creates derivative demand across power equipment, cooling systems, cabling, real estate, recycled metals, and EMS.

4. Financialisation and Formalisation. SIP flows continue to compound, insurance penetration is rising, wealth management platforms are scaling, and the capital market infrastructure (depositories, registrars, exchanges) is seeing structural throughput growth. Simultaneously, the formalisation of the economy is benefiting organised retailers, branded consumer companies, and lending platforms that can leverage data and technology.

5. Premiumisation and Aspiration. Indian consumption is bifurcating premium and organised segments are structurally outperforming mass categories. This is visible across alcoholic beverages (shift from brown to white spirits), fashion (branded vs. unbranded), consumer durables (premium SKUs), jewellery (organised vs. unorganised), and even healthcare (branded hospital chains). The underlying driver is rising per-capita income, urbanisation, and changing consumer preferences among younger demographics.

Disclaimer - Nothing here is a buy/sell recommendation. This is only for educational purposes.

The Structural Capex Supercycles

Theme 1 - Power, Grid & Renewable Infrastructure

The structural case: India’s power sector is in the midst of its most significant investment cycle since liberalisation. The demand side is unambiguous; peak electricity demand is projected to reach 458 GW by 2032, and the National Electricity Plan mandates massive expansion of transmission and distribution infrastructure. Between 2014 and 2024, over 193,000 circuit kilometres of transmission lines were already completed and 3,000 new substations commissioned. Yet the task ahead is larger still: 123,577 circuit km of new lines are envisaged between 2022-2027 alone.

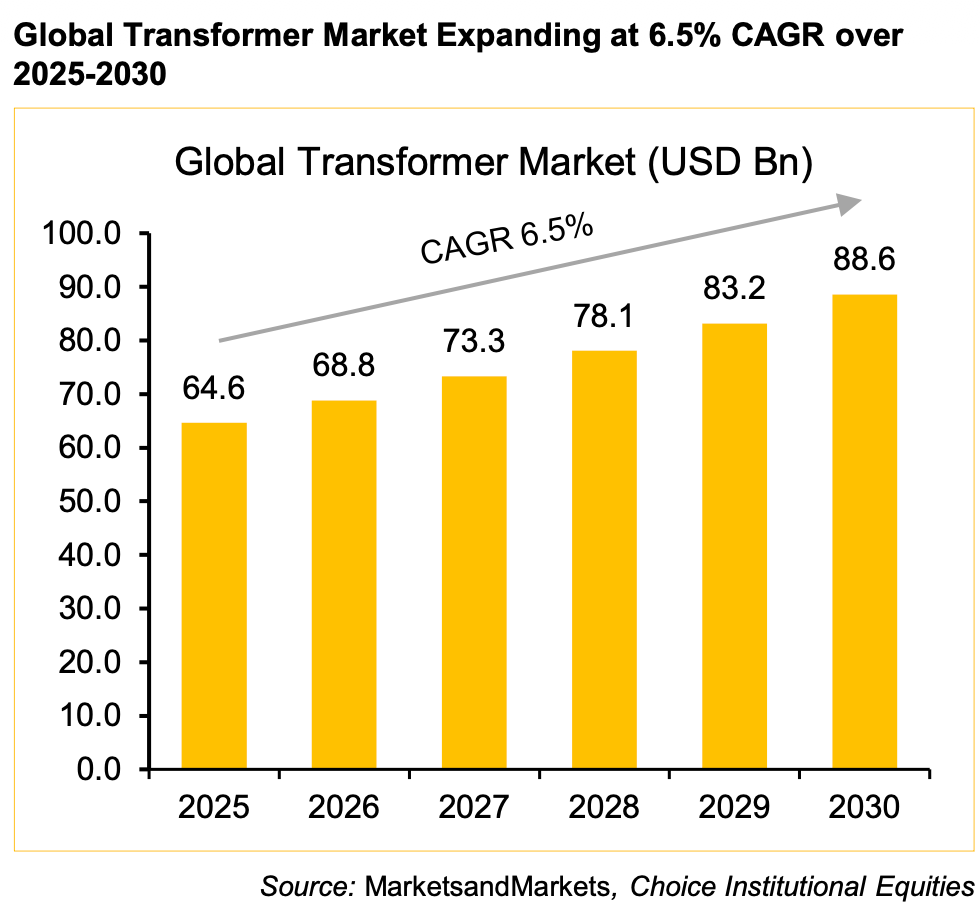

The India power transformer market, valued at approximately $3.8 billion in 2026, is projected to grow at an 8.7% CAGR to reach $8 billion by 2035. Large transformers (400 kV and above) are expanding at nearly 10% CAGR, outpacing medium and small categories, reflecting the grid’s voltage upgrade from 220 kV to 400/765 kV and HVDC corridors. Supply tightness in medium and high-voltage transformers is supporting pricing power for established manufacturers, a rarity in industrial India where pricing has historically been competitive and cyclical.

India’s transformer exports are also surging amid a global supply shortage. The global power transformer market is projected to reach $65.7 billion in 2026 and grow to $96.8 billion by 2033. Indian manufacturers with PGCIL approvals and global certifications are well-positioned to capture this export opportunity, adding a structural demand layer beyond domestic consumption.

Renewable energy integration is adding further complexity and demand. Every MW of renewable capacity requires approximately 7 MVA of transformation capacity. With India targeting 500 GW of non-fossil fuel capacity by 2030, the evacuation infrastructure transformers, cables, switchgear, Bushings, Insulators and grid-scale storage becomes a binding constraint. Companies positioned at the intersection of renewable evacuation and grid modernisation are seeing multi-year order book visibility.

What managements are saying:

The commentary across power and industrial companies is overwhelmingly constructive, with several key observations:

APAR Industries has upgraded its conductor margin guidance to ₹35,000-40,000 per tonne, reflecting strong demand for specialised conductors used in high-voltage transmission. The company is seeing healthy order inflows across conductors, cables, and oils, with T&D demand remaining the primary growth driver.

Voltamp Transformers continue to benefit from supply tightness in the medium and high-voltage transformer segment. The company’s focus on distribution and power transformers up to 220 kV has positioned it well for the ongoing grid expansion cycle. Order book visibility remains strong across both domestic and export markets.

Atlanta Electricals achieved a major strategic milestone with PGCIL approval for 400 kV power transformers in April 2026. Management indicated that 400 kV and 765 kV products will offer margins roughly 200 bps higher than the 220 kV segment once initial costs for R&D, testing, and technology tie-ups are absorbed. Production reached 22,943 MVA in FY26 across five factories, with the Vadod plant expected to reach 55% utilisation in FY27 and 100% by FY28.

Cable manufacturers like KEI Industries/ RR Kabel / Universal Cable / Polycab are seeing healthy demand across its cables and wires portfolio, driven by infrastructure, T&D, and real estate construction. The company’s distribution expansion and brand-building efforts are supporting premiumisation within the wires segment.

Component suppliers Qpower is also near its major capex completion phase and is on track to commercialise its Sanghli capex (9x the current capacity in base business) with interesting opportunities emerging in its Turkey business where it is getting good demand on the BESS front. It is kind of a tier 2 play in the HVDC capex supplying to players like Hitachi, GE and Siemens whose order book itself is growing in a strong way.

Triveni Turbine continues to see strong demand for industrial turbines, with order inflows supported by the renewable energy and industrial capex cycle. The company’s focus on aftermarket services and higher-capacity turbines is expanding the addressable market. But one has to see here how the execution plays out because approval process and get go can be time consuming in such cases

Kilburn Engineering is positioned as a niche player in drying solutions and process equipment, with increasing traction in data centre cooling and industrial applications.

CESC and NHPC represent the utility side of the power infrastructure build-out, with CESC benefiting from regulated returns and distribution expansion, while NHPC’s hydropower portfolio offers baseload capacity with renewable classification.

The Tata Power Company is executing across the entire power value chain - generation (solar, wind, thermal), transmission, distribution, and rooftop solar. The company’s renewable capacity additions and distribution expansion provide multi-year visibility.

JSW Energy is scaling its renewable capacity aggressively, with a target of 20 GW by 2030. The company’s focus on battery storage and green hydrogen positions it for the next phase of the energy transition.

How an investor should think about this theme:

The power infrastructure theme is at an unusual intersection of structural demand visibility, supply-side constraints, and pricing power, a combination that rarely persists in Indian industries. The investment case rests on three pillars:

First, order book visibility. Companies with multi-year order backlogs (1.5-3x trailing revenue) have genuine earnings visibility. The key question is whether order books are primarily domestic government (lower margins but more predictable) or a mix of private/export (higher margins but potentially lumpier).

Second, pricing vs. volume. The current cycle is unique because supply tightness is enabling pricing power alongside volume growth. This double benefit rarely persists; investors should expect pricing to normalise as new capacity comes online over FY28-29, making execution speed and cost discipline the differentiators.

Third, the voltage upgrade ladder. Companies moving up the voltage curve (from 220 kV to 400 kV to 765 kV) are not merely growing; they are entering higher-margin, higher-barrier segments with fewer competitors. This is a genuine moat-building exercise, not a cyclical uplift.

Risks to monitor: Commodity inflation (copper, CRGO steel, transformer oil) can compress margins if input costs rise faster than realisations. Raw material availability, particularly CRGO steel, remains a bottleneck. Government order execution can be lumpy and payment cycles elongated. Export demand, while structurally positive, is subject to geopolitical risk and currency fluctuations. Finally, the Middle East crisis could affect near-term export visibility and gross margins.

But the demand largely is structural in nature and to optimise for near term in such themes can be very difficult in such themes

Theme 2 - The Data Centre Ecosystem

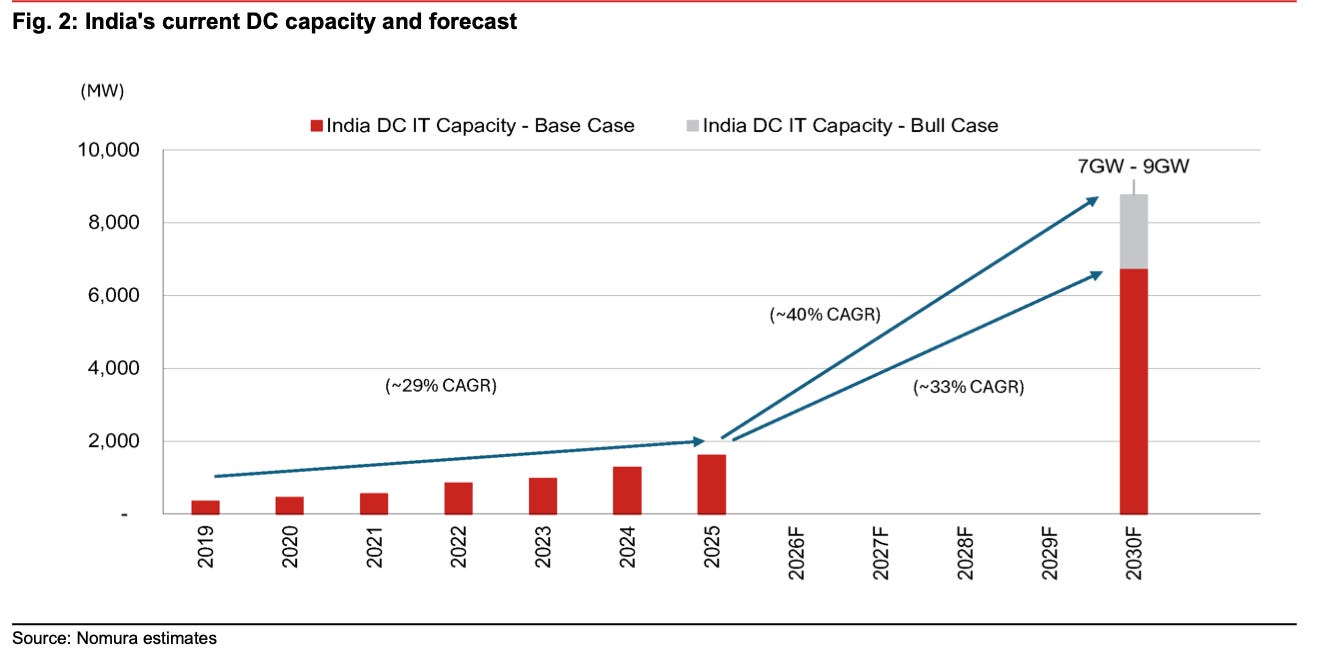

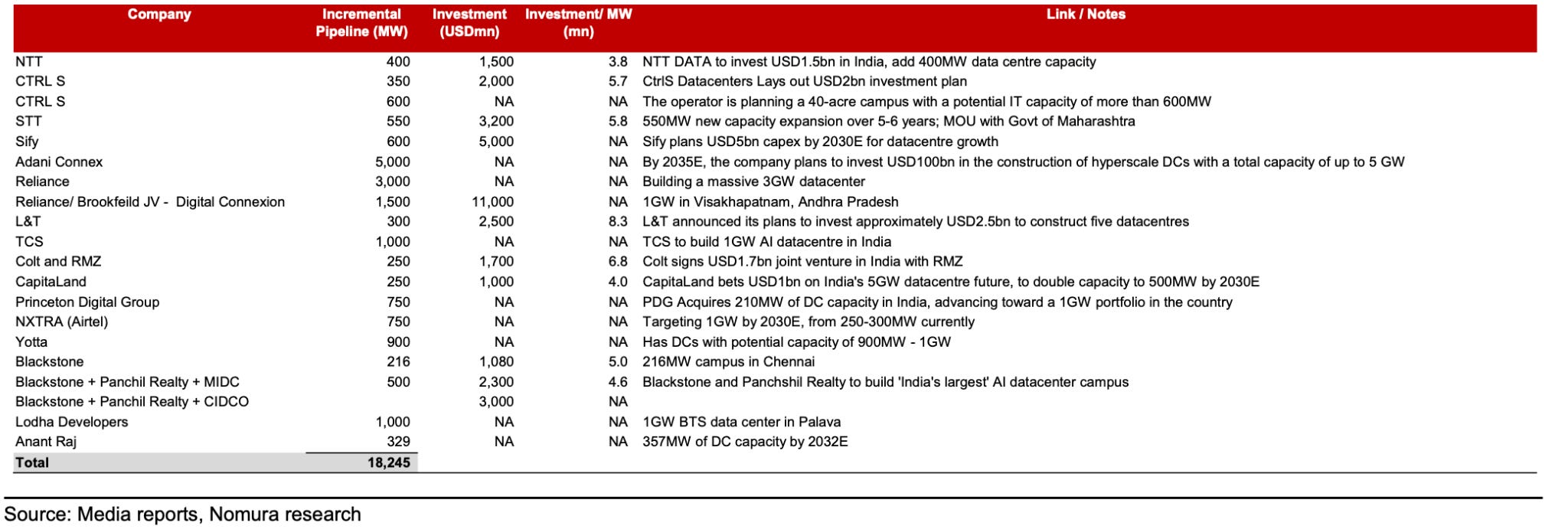

The structural case: India’s data centre market is transitioning from a “potential” narrative to an execution at scale reality. Total installed capacity crossed 1,700 MW in 2025, supported by a record supply addition of 440 MW (up 160% from the prior year). For 2026, an estimated 500 MW of fresh supply is expected, taking total capacity to approximately 2.0-2.2 GW. The market, valued at approximately $9.8 billion in 2025, is projected to reach $21 billion by 2031, growing at a 13.6% CAGR.

The Union Budget 2026-27 provided a significant policy catalyst as a tax holiday till 2047 for eligible foreign cloud service providers operating through India-based data centre infrastructure. This positions India as a preferred destination for hyperscale deployments. Globally, data centre investments reached $56.4 billion in 2025, taking cumulative commitments to $126 billion. This figure is projected to rise by approximately 45% YoY to exceed $180 billion in 2026.

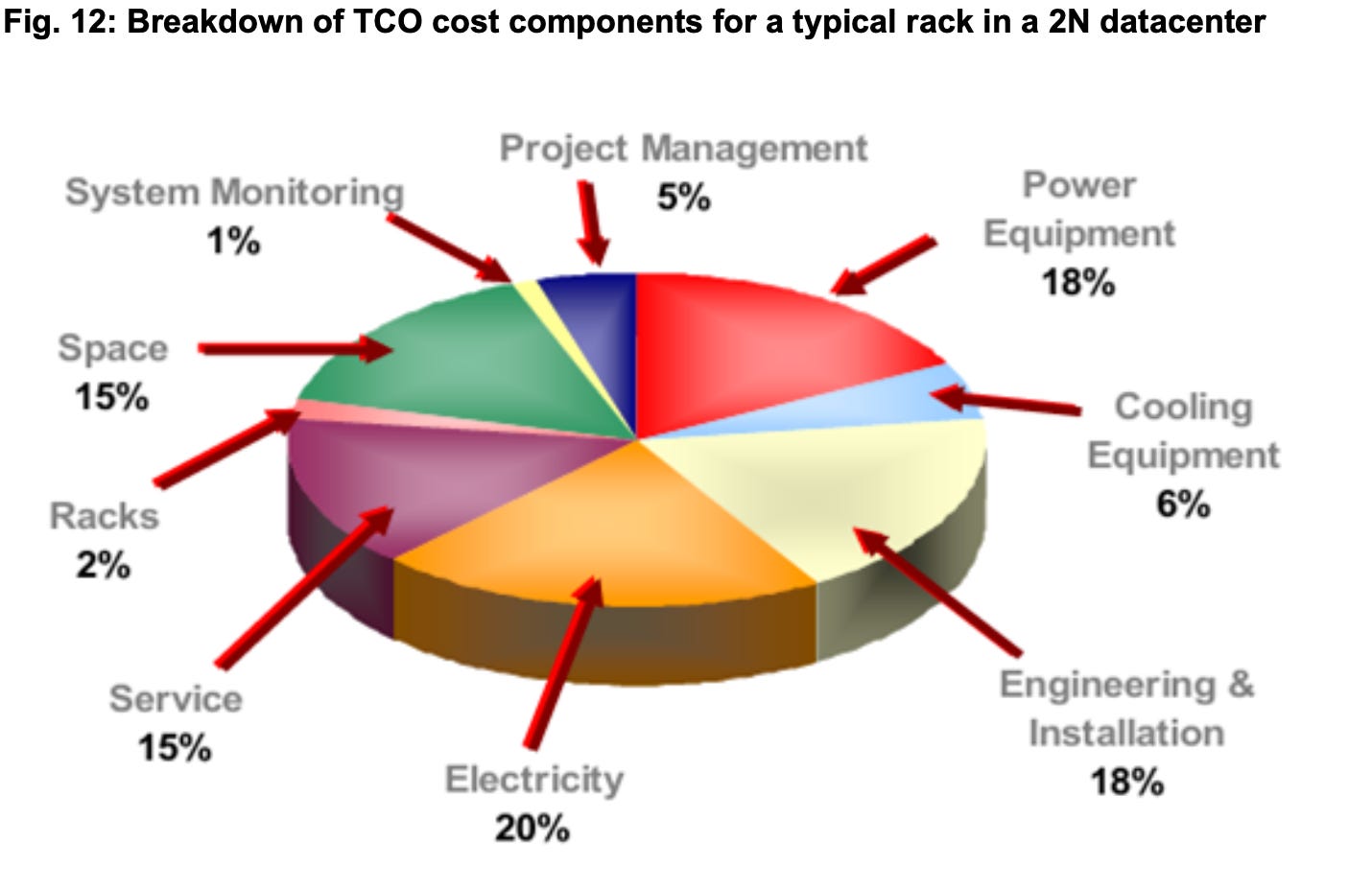

India also offers a meaningful cost advantage, with data centre construction costs at $6-7 million per MW significantly lower than mature APAC markets such as Singapore ($12-15 mn/MW) and Japan ($10-12 mn/MW). This enhances its appeal for large-scale investments.

What makes the data centre theme particularly investable in India is the breadth of derivative demand it creates across the industrial ecosystem:

Power equipment: Transformers, switchgear, UPS systems, DG sets, and power distribution units — every MW of data centre capacity requires dedicated power infrastructure.

Cooling systems: Data centres are among the most energy-intensive cooling applications; precision cooling (CRAC/CRAH units), liquid cooling systems, and thermal management are critical components.

Cables and wires: High-quality power and fibre-optic cabling is essential for data centre operations.

Real estate: Data centres are emerging as a mainstream institutional asset class, attracting REITs and institutional capital.

EMS and components: Server assembly, PCB manufacturing, and component localisation create demand for the EMS ecosystem.

Recycled metals: Data centres are significant consumers of copper, aluminium, and lead (for batteries), creating demand for the recycling ecosystem.

What managements are saying:

The data centre theme was referenced across management commentaries from at least 15 companies spanning multiple sectors, underscoring how widely the derivative demand radiates:

Blue Star is specifically positioned as a play on data centre cooling demand. Management highlighted increasing traction in precision cooling solutions for data centres, with the company investing in product development for this high-growth segment. Data centres represent a structural demand addition beyond the company’s traditional HVAC business.

Aeroflex Industries manufactures stainless steel flexible flow solutions (corrugated tubes, hoses) and is seeing increasing data centre-related demand for its products in cooling and fire suppression systems.

There also a lot of other companies in Power Piping which are also getting beneficiary of this data centre demand where players like Dee Dev (on front of HRSG pipes), Venus Pipes (on front of spooling business coming from data centre cooling solution side and even Ratnamani through its subsidiary RESS that supplies this solutions on nuclear side (indirect beneficiary as a lot of nuclear power capex is happening because of massive power demand by DC)

Mindspace Business Parks REIT benefits from data centre proximity demand and tech parks adjacent to data centre clusters see higher occupancy and rental premiums.

Across the power equipment companies - APAR Industries, KEI Industries, R R Kabel and Ram Ratna Wires - data centres were cited as a distinct demand driver alongside T&D and real estate, contributing incremental volume growth in specialised cable and wire categories.

In the recycling sector, Gravita India highlighted data centres as a growing end-use for recycled lead and copper, while Pondy Oxides & Chemicals is seeing similar demand patterns. Also smaller players in the recycling space that are into value-added products in copper recycling such as Bhagyanagar Industries are also getting good visibility from these tailwinds.

Epack Prefab Technologies / Interarch highlighted data centres as an emerging vertical for its pre-engineered building (PEB) solutions, alongside solar, EV, and warehousing-led capex. PEB as an industry should be beneficiary of a lot of this infra led capex demand as they fast track the capex process compared to traditional Brick and Mortar structures.

There are more such other opportunities and players that are there and are beneficiary of this demand. We will be going live this week (For SOIC Members) with the podcast that we have recorded with Akshay Jogani of Xponent Tribe going into depths of understanding this space.

If you are not a SOIC member and want to get the early access of this podcast here’s the link to join the membership - https://learn.soic.in/learn/SOIC-Course

How an investor should think about this theme:

The data centre ecosystem is an investable adjacency in most listed companies with data centre exposure deriving it as an incremental demand driver rather than their primary business. The investment approach should focus on three lenses:

First, pure-play vs. derivative exposure. India currently lacks large-cap pure-play listed data centre operators. The investment opportunity lies primarily in the picks-and-shovels companies power equipment, cooling, cabling, and construction that supply into the data centre build-out. This means understanding how much of each company’s revenue is genuinely data centre-linked vs. bundled into broader industrial demand.

Second, recurring vs. one-time demand. Power equipment and construction are one-time during the build phase, while cooling, maintenance, power management, and cabling upgrades are recurring. Companies with exposure to the latter have more durable demand.

Third, capacity and approval gating. Not every equipment manufacturer can supply into data centres specifications are stringent, redundancy requirements are high, and Tier III/IV certifications create qualification barriers. Companies that have already qualified with hyperscale operators or major colocation providers have a meaningful head start.

Risks to monitor: Power availability remains the biggest constraint for data centre deployment outside Tier-I metros. Water availability for cooling is an emerging concern, particularly in water-stressed regions. Regulatory uncertainty around land use, power procurement, and connectivity can delay projects. Competition from established APAC hubs (Singapore, Hong Kong, Tokyo) for hyperscale deployments.

Theme 3 - Defence & Aerospace Indigenisation

The structural case: India’s defence sector is undergoing a fundamental transformation from licence-based manufacturing and technology transfer (ToT) to indigenous intellectual property development, proprietary R&D, and exportable defence platforms. The government’s indigenisation push is backed by sustained budgetary support, with the defence procurement budget increasingly ring-fenced for domestic sourcing. The “positive indigenisation lists” have expanded to over 500 items that cannot be imported, creating a captive market for domestic manufacturers who can meet quality and timeline requirements.

The more significant shift is qualitative: the sector is moving from contract manufacturing (building someone else’s design under licence) to design-led manufacturing (creating proprietary technologies that can be sold domestically and exported). This shifts the value proposition from labour cost arbitrage to IP creation, which carries fundamentally different margin and sustainability characteristics.

What managements are saying:

Centum Electronics stood out with its clear articulation of the shift from ToT-led manufacturing towards indigenous IP and R&D. The company is investing in proprietary electronic sub-systems and modules for defence and aerospace applications, with execution capability becoming the main differentiator. Management emphasised that the competitive landscape is increasingly favouring companies with genuine design and testing capabilities over pure assembly operations.

Zen Technologies is expanding beyond training simulators into counter-drone systems, cyber security solutions, and unmanned aerial systems. The company’s product portfolio now spans anti-drone technology (a segment seeing rapid growth globally), advanced training systems for air defence and ground forces, and exported defence products.

Data Pattns is also getting strong order book visibility with in near term the company is expecting new orders worth 1000 crs that can largely double their orderbook. Also the company has strong visibility of orders coming from Brahmos Seeker front.

Primarily the Electronic warfare space is getting strong traction with the new orders flowing in for the companies across the value chain. We have discussed this theme in depth in one of our editions earlier.

Do check this out - Electronic Warfare - SOIC Trends Outlook - HQ.pdf

Several auto ancillary and engineering companies are diversifying into defence as a structural growth vertical:

Sansera Engineering is developing precision-engineered components for aerospace and defence applications, leveraging its existing capabilities in complex machining and metallurgy.

Belrise Industries highlighted defence and aerospace as an emerging revenue contributor alongside its core auto ancillary business, with investments in electronics and electromechanical assemblies.

How an investor should think about this theme:

Defence investing in India requires patience and a differentiated framework compared to conventional industrial analysis:

First, order book quality matters more than size. A company with a ₹2,000 crore order book comprising five large government orders has fundamentally different risks than one with ₹2,000 crore across 50 smaller orders with multiple customers and product categories. Concentration risk, payment cycle variability, and execution dependence on government timelines are real considerations.

Second, IP vs. assembly. The real value creation in defence is in companies that own proprietary IP - designs, testing data, certifications, and system integration capabilities. Assembly operations will face margin compression as the sector matures and competition intensifies. The question to ask: “If this company disappeared tomorrow, could its customers simply hand the drawings to another manufacturer and replicate the product?”

Third, export potential as a value multiplier. Companies that can demonstrate export capability (not just intent) have a structurally larger addressable market and better pricing power. India’s defence exports have been growing but remain small relative to the opportunity. The certification and qualification cycle for defence exports is measured in years, not quarters.

Risks to monitor: Government procurement cycles can be unpredictable, leading to lumpy revenue recognition. Payment cycles from government entities (DPSUs, ordnance factories) can stretch working capital. Technology risk in developing indigenous systems without established track records. Competition from PSU defence companies with legacy relationships and larger balance sheets.

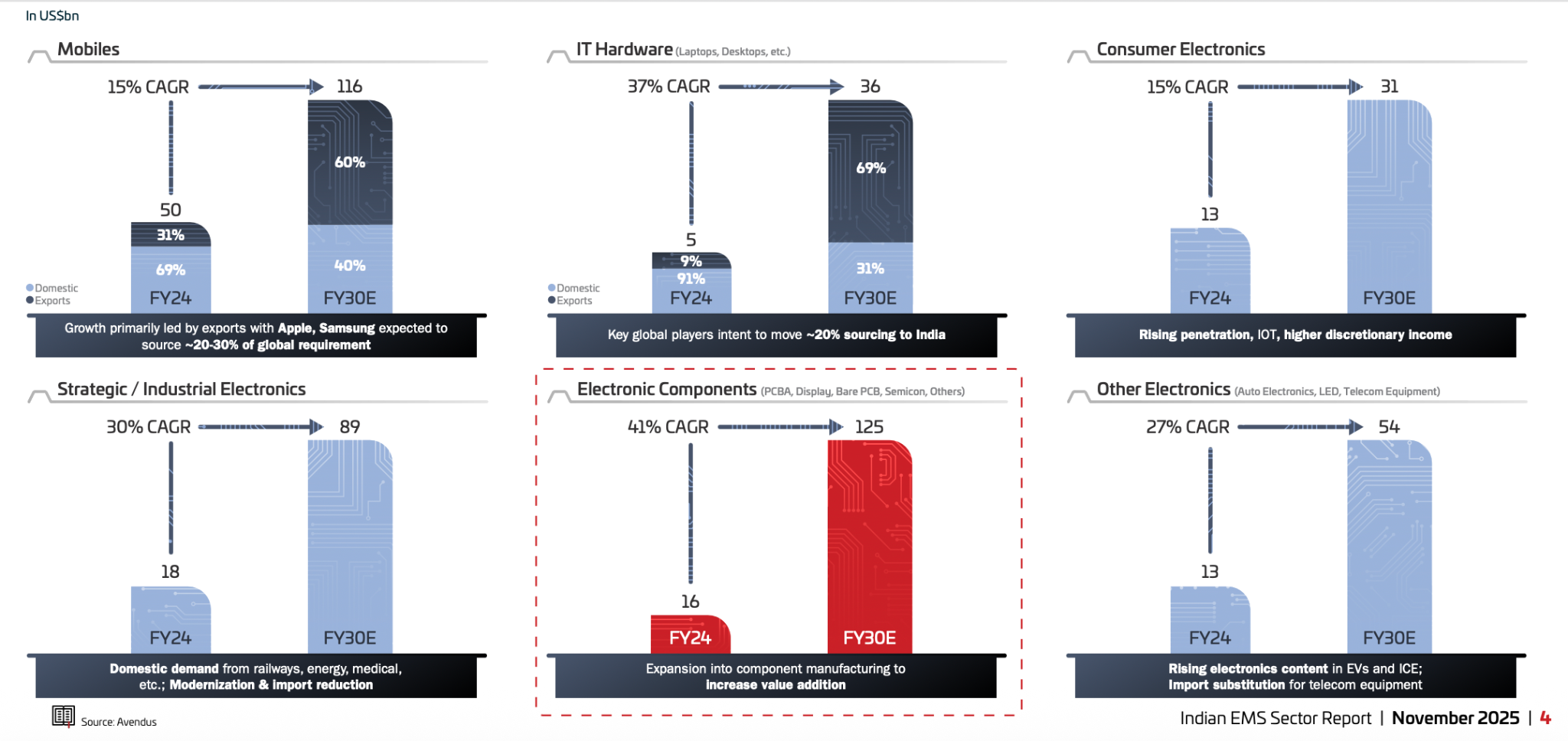

Theme 4 - Electronics Manufacturing: From Assembly to IP

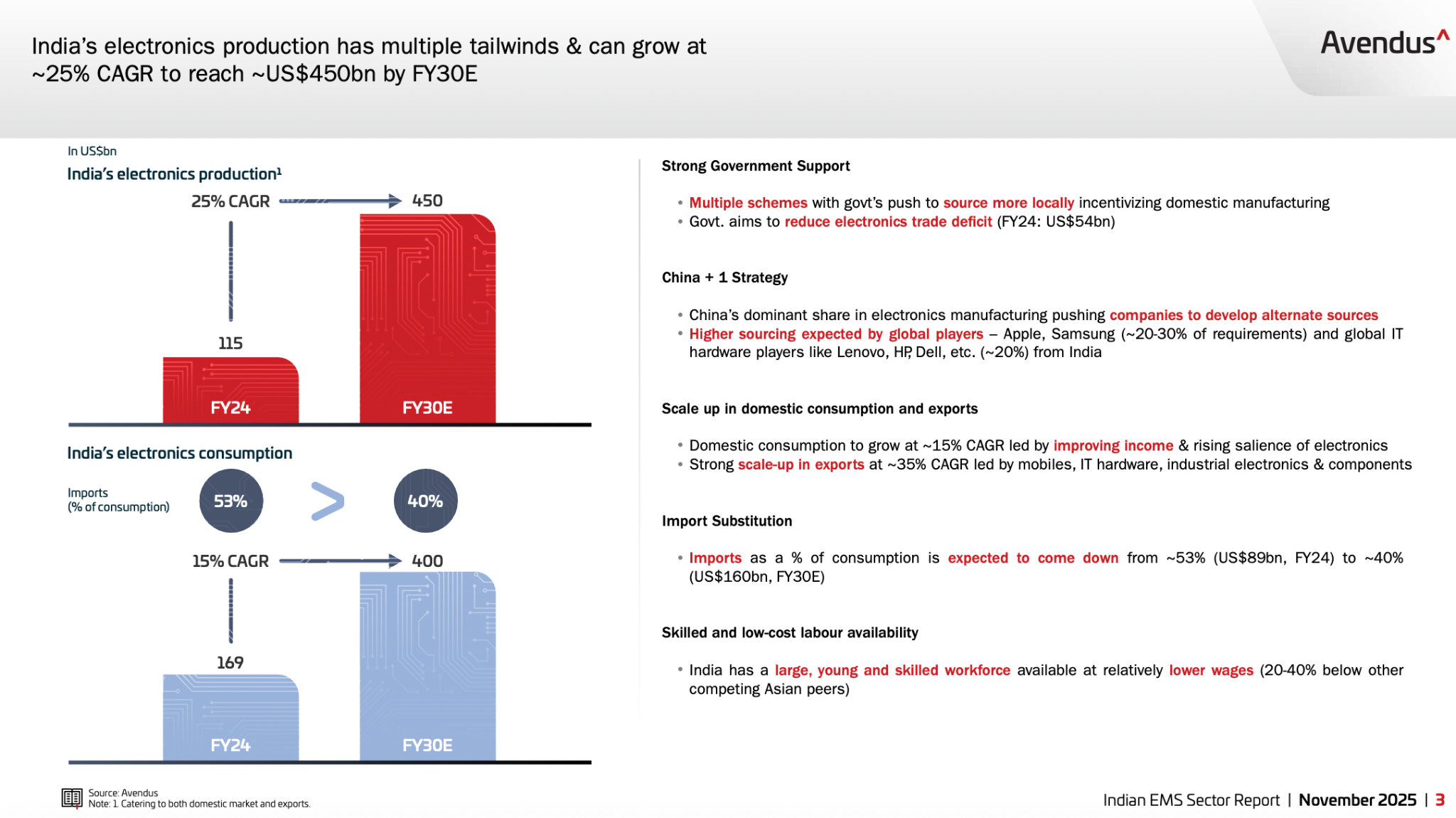

The structural case: India’s electronics manufacturing services (EMS) sector is in a genuine structural upcycle, driven by the convergence of Make in India policy support, global supply chain diversification (China+1), rising outsourcing by multinationals, and export opportunities. The India EMS market, valued at approximately $39-46 billion in 2026, is projected to grow at 10-17% CAGR through 2031-32, reaching $62-198 billion depending on the scope definition.

The PLI 2.0 scheme and the Electronics Components Manufacturing Scheme together contribute an estimated 2.8 percentage-point uplift to market CAGR by subsidising capex and output. Tamil Nadu, Karnataka, and Uttar Pradesh have emerged as key manufacturing clusters, while emerging corridors in Andhra Pradesh and Madhya Pradesh are building capacity for PCBs and copper-clad laminates.

The more important structural shift, however, is not in scale but in value addition. The sector is moving from simple assembly (populating PCBs with imported components) towards higher-value manufacturing - box-builds, original design manufacturing (ODM), PCB fabrication, component manufacturing, and semiconductor packaging. This value-chain ascent is where genuine margin expansion and customer stickiness reside. The growth this time will be led by electronic component manufacturers as the story of indigenisation gets even stronger. Also on the consumer electronics there is a new supply chain that is getting visible now is “Apple in India”. Someday we will talk in depth about this supply chain. Do mention in comments if you want a deep dive on this particular supply-chain

What managements are saying:

Syrma SGS Technology remains confident despite rising competition, emphasising its capabilities in industrial electronics, healthcare devices, and automotive electronics. Management highlighted that the competitive moat in EMS is shifting from cost to capability specifically, the ability to handle complex, multi-technology assemblies with stringent quality requirements. The company’s expansion into RFIC (Radio Frequency Integrated Circuits) and semiconductor packaging represents a deliberate move up the value chain.

Avalon Technologies is focused on the higher-margin end of the EMS spectrum medical devices, industrial controls, and aerospace electronics where qualification cycles are longer but customer relationships are stickier and margins more sustainable. Management indicated that the transition from pure PCB assembly to complete box-build and system integration is a key margin driver.

Hind Rectifiers is positioned at the intersection of power electronics and defence/railway applications, manufacturing rectifiers, transformers, and power electronic systems. The company’s focus on design-led manufacturing rather than commodity assembly gives it pricing resilience.

Centum Electronics also straddles this theme with its electronic sub-systems and modules for defence and industrial applications, representing the design-heavy end of the EMS spectrum.

Also Aimtron is structurally transforming from a commoditized EMS provider into a high-margin full-stack Original Design Manufacturer (ODM), leveraging in-house design capabilities and critical industry certifications to lock in sticky, multi-year production contracts. The company’s growth thesis is bolstered by strategic expansion into the US market via the AIC acquisition and a high-value ODM order book exemplified by a transformative data center UPS relationship—which allows for significant revenue scaling without heavy incremental capex.

EMS can be an interesting space to keep a watch on and find companies that are relatively reasonably valued and have a good order book and visibility of growth going forward.

How an investor should think about this theme:

EMS investing requires careful evaluation of where a company sits on the value-addition spectrum:

First, customer mix and concentration. Companies dependent on 2-3 large consumer electronics OEMs (smartphones, TVs) face constant margin pressure as volumes commoditise and OEMs squeeze costs. Companies serving industrial, medical, aerospace, or defence customers typically enjoy longer product cycles, higher margins, and greater switching costs.

Second, assembly vs. design. The gross margin tells the story: companies doing pure assembly at 8-12% gross margins are in a fundamentally different business than those doing design-led manufacturing at 25-35% gross margins. The latter requires years of investment in R&D, testing infrastructure, and customer qualification, creating genuine barriers to entry.

Third, the ODM transition. Companies making the leap from electronic manufacturing services (building someone else’s design) to original design manufacturing (designing the product and then manufacturing it) are capturing a larger share of the value chain. This transition typically shows up in R&D spending as a percentage of revenue, patent filings, and the nature of customer contracts.

Risks to monitor: Technology obsolescence risk in fast-moving consumer electronics segments. Working capital intensity (EMS companies often fund 60-90 days of inventory and receivables). PLI incentive dependency for margin support. Component availability and import dependency remain challenges despite localisation efforts. Competition from Taiwanese and Chinese EMS firms expanding in India.

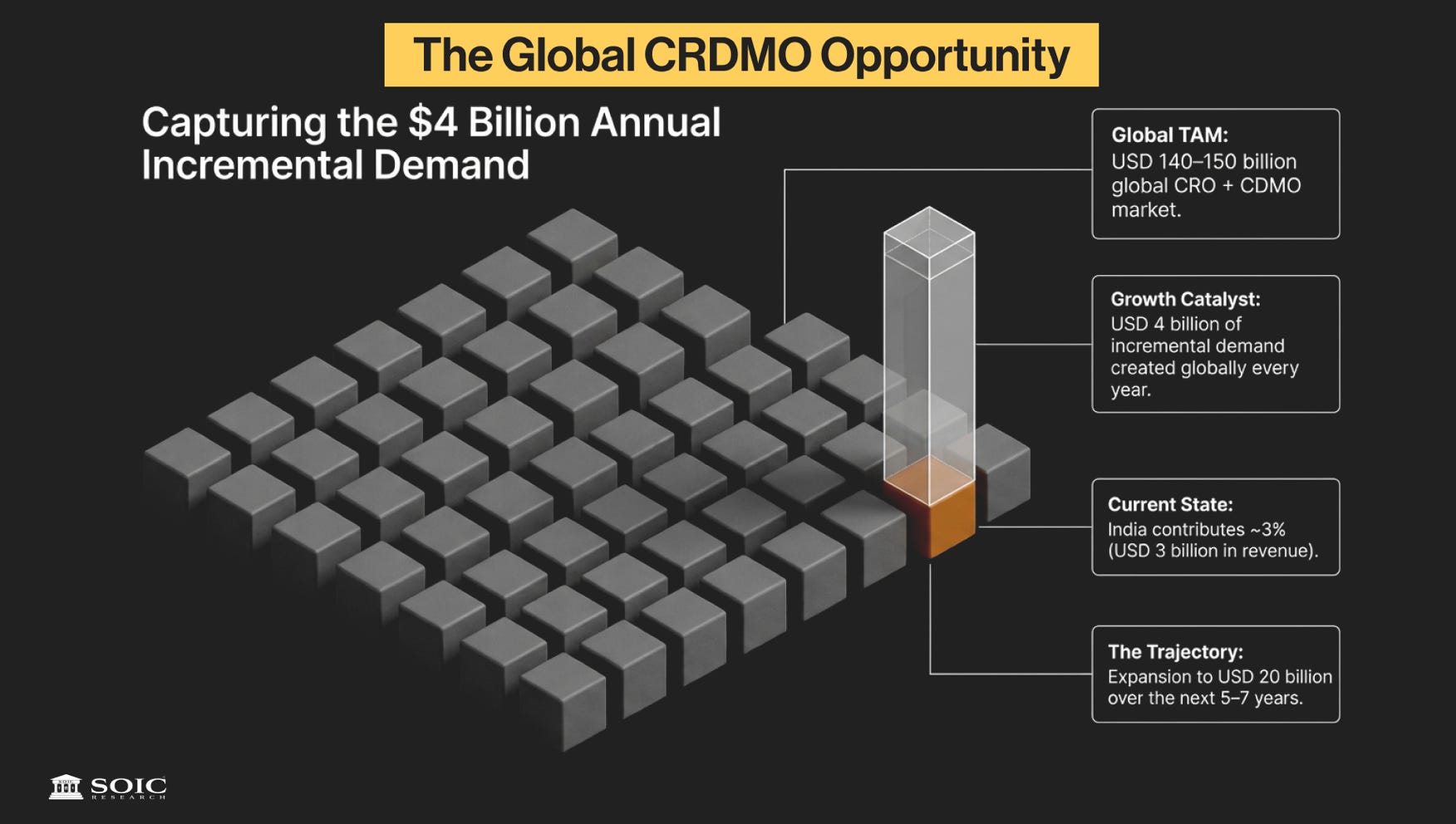

Theme 5 - Pharma’s CDMO/CRDMO Pivot

The contract development and manufacturing organisation (CDMO) segment has emerged as the single most exciting structural growth pocket in Indian pharmaceuticals. India’s CDMO market, estimated at $12-13 billion currently, is projected to grow at 13-15% CAGR to reach $18-19 billion by 2030 and potentially $55 billion by 2033, driven by rising pharmaceutical outsourcing, cost-competitive manufacturing, expanding biologics capabilities, and global regulatory compliance.

Several structural forces are converging to make this an unusually durable growth theme:

The China+1 diversification in pharma supply chains is accelerating, catalysed by the US BIOSECURE Act (a bipartisan initiative prompting pharmaceutical companies to re-evaluate outsourcing to Chinese CDMOs). India, as the world’s largest supplier of generic medications — commanding over 40% of the US OTC drug export market and producing approximately 60% of the world’s vaccines — is the natural alternative.

The complexity ladder is the key value driver. Indian CDMOs are moving from simple generic API manufacturing into complex chemistries (multi-step synthesis with hazardous intermediates), high-potency APIs (HPAPIs), sterile injectables, peptides, antibody-drug conjugates (ADCs), biologics, precision fermentation, and mRNA platforms. Each step up this ladder commands higher margins, longer contract durations, and deeper customer lock-in.

The asset-light economics of CDMO businesses create attractive return profiles. With EBITDA margins of 25-35% (versus 15-20% for traditional generic pharma), lower marketing costs, and dollar-denominated revenues, CDMOs generate structurally superior RoCE trajectories once initial capacity investments are absorbed.

What managements are saying:

Neuland Laboratories is among the most compelling CDMO stories. The company is focused on custom manufacturing services (CMS) for complex APIs, with a growing pipeline of late-stage molecules for large pharma and biotech customers. Management commentary suggested healthy pipeline progression, with molecules moving from clinical to commercial stages, providing multi-year revenue visibility.

Laurus Labs is executing its CDMO pivot after years of investment in capability and capacity. The company’s CDMO business spans small molecules, biologics (through Laurus Bio), and crop sciences, with growth driven by rising contributions from complex chemistries and late-stage molecules. Management indicated early recovery in the generic API segment after prolonged destocking and pricing pressure.

Cohance Lifesciences is positioned as a specialty CDMO focused on complex intermediates and APIs for regulated markets. The company’s capabilities in multi-step synthesis, continuous flow chemistry, and photochemistry are differentiators in the specialty chemistry space.

Aarti Pharmalabs articulated a long-term CDMO sales guidance of ₹10 bn (versus FY26 revenues of ₹2.7 bn), with 30% expected from products commercialised post-FY27. The CDMO API pipeline spans early-stage to near-commercial molecules, all patented, focused on small molecules across 21 customers. Company-level EBITDA margin guidance stands at 23-25% in the near-term, with management planning dedicated CDMO blocks of ₹2.5 bn each, adding one block annually.

Jubilant Pharmova is executing its radiopharma strategy, with the Montreal facility and Spokane Line 3 representing key near-term revenue drivers. The company’s radiopharmacy network in North America is a distinctive asset in a high-growth therapeutic segment.

Sudeep Pharma and Senores Pharmaceuticals represent the emerging tier of specialty pharma companies investing in differentiated capabilities.

Also Players like Sai Life Sciences which actually is one of the very unique CRDMO companies in India that does not have any exposure to the commodity business side which with the CDMO lumpiness can destroy the margins big time for the company. This is a CRDMO flywheel business

Among the larger formulation companies, Sun Pharmaceutical Industries and Zydus Lifesciences continue to invest in specialty therapeutics, biosimilars, and complex injectables, while Aurobindo Pharma guided for low single-digit price erosion in the US business, suggesting stabilisation in the generics environment.

How an investor should think about this theme:

CDMO investing is fundamentally different from generic pharma investing. The value drivers are pipeline quality, customer relationships, and capability differentiation not product launches, market share, and pricing dynamics.

First, pipeline stage risk. A CDMO’s revenue visibility depends on where its molecules are in the clinical pipeline. Phase III and commercial molecules provide near-term revenue certainty; Phase I molecules represent optionality but carry binary risk. The ideal portfolio has a mix across stages with a healthy funnel of molecules progressing through phases.

Second, customer concentration vs. relationship depth. A CDMO with 60% of revenue from one customer carries event risk (the customer’s molecule failing, the customer insourcing). However, deep relationships with a few large pharma customers can be more valuable than shallow relationships with many, because they indicate trust, repeat contracting, and expansion potential.

Third, capex-to-revenue conversion. CDMOs are capital-intensive during the build phase. The key metric is how quickly new capacity converts to revenue a well-managed CDMO should achieve 50-70% utilisation within 18-24 months of commissioning. Capacity that sits idle beyond this window signals either misjudged demand or qualification delays.

Fourth, the complexity premium. Margins in CDMO are a function of chemistry complexity, not scale. A company doing ₹500 crore of peptide synthesis can earn higher EBITDA margins than one doing ₹2,000 crore of commodity API manufacturing. The question is whether a company’s capabilities genuinely reside in complex chemistry (multi-step, hazardous, sterile, high-potency) or whether it is positioning commodity manufacturing under a CDMO label.

Risks to monitor: Molecule failure risk (a key molecule failing in clinical trials eliminates associated revenue). Regulatory risk (FDA warning letters can disrupt operations and customer confidence). Geopolitical risk (trade policy changes, tariffs, and reshoring initiatives can alter outsourcing flows). Capacity overshoot (too many Indian CDMOs building similar capabilities can lead to pricing pressure). The BIOSECURE Act’s final form and implementation timeline remain uncertain.

Theme 6 - Specialty Chemicals: Recovery and the Fluorination Wave

The Indian specialty chemicals sector is emerging from a two-year downcycle characterised by global destocking, pricing pressure, and subdued demand. FY27 is expected to be a recovery year, with growth led by volume ramp-up from new capacities, improving utilisation rates, and gradual pricing recovery. However, the more compelling investment thesis lies not in the cyclical recovery but in the structural positioning of select companies in super-specialty segments particularly fluorination, electrolyte additives, semiconductor chemicals, and advanced materials.

What managements are saying:

Navin Fluorine International and Gujarat Fluorochemicals are the most prominent super-specialty chemical plays. Both companies possess strong pricing power, cost pass-through ability, and exposure to value-added areas such as fluorination chemistry, advanced materials, electrolyte additives (for lithium-ion batteries), and semiconductor chemicals. Management commentary at both companies suggested potential upside risk to FY27 margins given their differentiated positioning.

Actuaas Chemicals (Ami Organics) provided detailed forward guidance: FY27E revenue growth guidance intact at 25% (chances are high for an upgrade around H2), with EBITDA margin guidance at similar levels to FY26 (approximately 36%). Management indicated confidence in maintaining margins despite the industry downturn, driven by specialty product mix and customer stickiness. By FY28E, battery chemicals and semiconductor chemicals are expected to emerge as meaningful revenue contributors.

Laxmi Organic Industries is in the midst of a capacity expansion phase, with growth expected from both its Fluorochemicals Division and the Specialty Intermediates business. The company’s investment in continuous flow chemistry and hazardous chemistry capabilities positions it for the next phase of import substitution.

NOCIL is India’s dominant rubber chemicals manufacturer, benefiting from import substitution and improving utilisation. The company’s specialty product portfolio (pre-dispersed chemicals, process aids) carries higher margins than commodity grades.

Archean Chemical Industries is focused on bromine and industrial salt, with the company improving its brine enrichment process. Capacity utilisation is expected to reach 50-60% in FY27E, with management guiding for doubling output over the medium term.

Privi Speciality Chemicals operates in aroma chemicals, a niche specialty chemistry segment with relatively stable demand dynamics and limited competition from China.

How an investor should think about this theme:

Chemicals investing requires distinguishing between cyclical recovery (which is transient) and structural positioning (which is durable):

First, pricing power as the acid test. In a commodity chemical, the company is a price-taker margins expand and contract with the cycle. In a specialty chemical, the company has some degree of pricing power through formulation complexity, qualification requirements, or customer switching costs. The key question: “If this company raised prices 5%, would customers accept it or switch?”

Second, fluorination and electrolyte additives as the structural kicker. Companies with capabilities in fluorination chemistry (Navin Fluorine, Gujarat Fluorochemicals) or battery chemical intermediates (Actuaas Chemicals) are playing into decade-long demand cycles driven by EV adoption and semiconductor fabrication. These segments carry 30-45% EBITDA margins versus 12-18% for commodity chemicals.

Third, capacity utilisation trajectory. Most chemical companies invested heavily in capacity during 2021-23. The recovery phase is about utilisation ramp-up, which drives operating leverage. A company moving from 55% to 75% utilisation on existing capacity generates significantly higher incremental margins than one still commissioning new plants.

Risks to monitor: Chinese chemical producers re-entering global markets with aggressive pricing can prolong the recovery timeline. Raw material volatility (crude oil, benzene, chlorine) affects input costs. Environmental compliance costs are rising in India, particularly for companies handling hazardous chemicals. Customer destocking cycles can re-emerge if end-market demand weakens.

Theme 7 - Metals & Materials: Execution Over Price

The investment narrative in Indian metals has shifted decisively from price-led gains (which characterised the 2021-22 commodity supercycle) to execution-led margin improvement through capacity ramp-up, cost optimisation, backward integration, and richer downstream product mix. This is a fundamentally different investment thesis, one driven by company-specific execution rather than macro commodity prices.

What managements are saying:

Usha Martin stands out as a margin-led story, driven by higher-value wire rope applications, offshore wind demand, synthetic slings, and disciplined market share gains. The company is deliberately moving its product mix towards specialty wire ropes and value-added solutions, which carry higher margins and lower cyclicality than commodity wire. This is the business where growth can come back after a long time.

Shyam Metallics and Energy offers margin upside from commissioning of new capacity across pellets, sponge iron, and downstream long products. The stainless steel backward integration and CRM (cold-rolling mill) profitability improvement represent specific margin catalysts that are independent of steel prices.

Jindal Stainless is the dominant Indian stainless steel producer, benefiting from import substitution, rising per-capita stainless consumption (India at ~3 kg vs. global average of ~7 kg), and expansion into value-added products for automotive, railways, and nuclear applications.

JSW Steel, Tata Steel and Jindal Steel represent the large-cap steel space, where the investment case is predicated on domestic demand growth (infrastructure, housing, auto), operational efficiency improvements, and capacity utilisation ramp-up.

Hindustan Zinc is benefiting from stable demand, improving gas availability, and capacity expansion in both zinc and silver. The company’s silver production is an increasingly valuable by-product given industrial and investment demand.

Welspun Corp is positioned in the pipes and structural steel segment, benefiting from energy infrastructure, water pipeline, and data centre-related demand. The company’s diversification into DI pipes and structural steel provides multiple growth vectors.

HEG Greentech is transitioning from a pure graphite electrode play to a diversified industrial platform, with investments in solar and green energy.

PCBL Chemical is focused on specialty carbon black and value-added products for tyre, rubber, and industrial applications, with new capacities in specialty grades targeting batteries and EV applications.

Also there can be a strong case for the few players in India which we have discussed multiple times in the past also that are completely backward integrated to the mine and have mines under the old mining lease. There lies the players such as GPIL, Lloyd metals, Jayaswal Neco and IMFA

How an investor should think about this theme:

First, separate the commodity from the company. The most common mistake in metals investing is conflating the commodity price cycle with the company’s value creation. A well-managed metals company can deliver 15-20% RoCE through the cycle by controlling costs, optimising product mix, and expanding downstream regardless of whether steel prices are at ₹48,000 or ₹55,000 per tonne.

Second, backward integration as margin insurance. Companies with captive raw material sources (iron ore, coal, scrap) have structural cost advantages that insulate margins from input cost volatility. GPIL, Lloyd metals, Jayaswal Neco and IMFA illustrate this well.

Third, the downstream value ladder. Moving from hot-rolled coils to cold-rolled to coated to value-added flat products, or from wire rods to wire ropes to specialty ropes, captures increasingly larger margin spreads. The capital investment is meaningful but the return profile is structurally superior. Companies articulating a clear downstream migration strategy deserve a valuation premium over commodity producers.

Global steel overcapacity (particularly Chinese exports) can depress domestic realisations. Energy cost volatility (coal, natural gas) directly impacts production costs. Regulatory risk around mining leases and environmental compliance. Currency movements affect export competitiveness and import parity pricing.

Theme 8 - Recycling & Circular Economy

The recycling sector in India is at an inflection point, driven by regulatory tailwinds (extended producer responsibility, plastic waste management rules), formalisation of the scrap value chain, and rising demand for recycled materials across copper, lead, aluminium, rPET, and e-waste. Data centres, in particular, are emerging as a significant new demand vector for recycled copper and lead (batteries), adding a structural growth layer.

What managements are saying:

Gravita India is the most diversified recycling platform, with operations across lead, aluminium, and copper recycling. The company is expanding capacity across multiple geographies (India, Africa, Asia) and is seeing increasing demand from data centres and battery manufacturers. Management highlighted the structural shift from unorganised to organised recycling, with GST compliance and EPR regulations driving formalisation. As a diversification strategy they are doing big capex and also acquired RMIL to diversify their revenue streams from Lead recycling to other verticals. Copper going forward can be a strong growth lever for the company.

Pondy Oxides & Chemicals is focused on lead and copper recycling, with growing traction in the data centre (UPS batteries) and EV battery recycling segments. The company’s recent capacity expansions position it for the next phase of volume growth.

Ganesha Ecosphere s India’s largest PET recycler, converting post-consumer PET bottles into recycled polyester fibre (rPET). The company benefits from regulatory mandates requiring minimum recycled content in textiles and packaging, as well as from global brands’ sustainability commitments.

Jain Resource Recycling is positioned in the e-waste and metal recycling space, a segment growing rapidly as electronics penetration increases and regulatory enforcement tightens.

How an investor should think about this theme:

Recycling is transitioning from a cyclical commodity-adjacent business to a structural growth opportunity. The key investor framework:

First, regulatory moat. Companies with established compliance systems, pollution control infrastructure, and EPR certifications have genuine barriers to entry. As regulation tightens (and it will), the cost of compliance rises, favouring incumbents.

Second, spread vs. volume. Recycling margins are driven by the spread between scrap procurement costs and refined material selling prices. Companies with better procurement networks (direct collection, long-term contracts with battery OEMs, municipal partnerships) have more stable spreads.

Third, the formalisation premium. As the unorganised sector shrinks (due to GST, EPR, and environmental enforcement), organised players gain market share with improving unit economics. This is a multi-year tailwind that is largely independent of commodity prices.

Input scrap availability and pricing volatility. Regulatory enforcement can be inconsistent across states. Competition from new entrants as the sector’s attractiveness increases. Commodity price cycles affect realisations even for recyclers.

Theme 9 - Premiumisation Across Consumer India

Perhaps the most visible consumption trend in India is the bifurcation of demand: premium and organised segments are consistently outperforming mass categories. This is not a cyclical phenomenon; it reflects structural shifts in demographics (younger, more aspirational consumers), income distribution (growing upper-middle class), urbanisation, and channel evolution (quick commerce and modern trade favouring premium products).

What managements are saying:

Trent continues to be the poster child for premiumisation in Indian retail, with Zudio (value fashion) and Westside (lifestyle retail) both delivering strong same-store-sales growth. The company’s ability to generate premium economics at accessible price points, backed by disciplined store expansion and inventory management, represents a distinctive competitive model.

Page Industries is India’s largest innerwear company (Jockey brand), operating in a segment where the shift from unbranded to branded is a multi-decade opportunity. Distribution expansion into tier 3/4 towns and introduction of premium product lines support volume and value growth.

Metro Brands continues to expand its store network across premium footwear formats (Metro, Mochi, Walkway), with strong same-store-sales and improving unit economics as stores mature.

Senco Gold represents the organised jewellery opportunity with organised retail penetration in jewellery still below 40%, the runway for branded players gaining share from family jewellers remains substantial.

Radico Khaitan is targeting P&A (Prestige & Above) salience of nearly 80% of the business over the next three-four years, reflecting a structural shift in consumer preferences from brown spirits toward white spirits, particularly among younger consumers. Management guided for EBITDA margin expansion of 125-150 bps, supported by premiumisation and favourable product mix improvements.

United Spirits highlighted that premiumisation trends remain structurally healthy with no visible signs of saturation in P&A categories. Karnataka excise reforms (duty slabs reduced from 16 to 8) are structurally positive for the industry, enabling smoother pricing actions.

Godrej Consumer Products and Marico are focused on volume-led growth, premiumisation, innovation, and distribution expansion despite renewed input cost pressures. Quick commerce, e-commerce, and modern trade are becoming increasingly important channels for premium products.

Emami is investing in new product categories (wellness, functional foods, personal care) to diversify beyond its core portfolio, with premiumisation driving the growth in these newer categories.

Tata Consumer Products is executing a portfolio transformation — from a commodity tea/coffee company to a branded FMCG platform spanning beverages, foods, and snacking. Distribution expansion and innovation in healthier/premium variants are supporting growth.

V-Mart Retail operates in the value fashion segment, targeting tier 2/3 markets where organised retail penetration remains low. The company’s store expansion strategy, improved sourcing, and private label focus are driving profitability improvement.

Shoppers Stop is repositioning as a premium department store format, with AI-led analytics, loyalty programmes, and private labels becoming competitive advantages.

In the similar we discussed in depth the Electronic Warfare space we have also put out a while back a deep dive on Premiumisation and consumer trends that are playing out and can play out going forward.

Do check that out too - SOIC Theme Premiumisation - August 2025.pdf

How an investor should think about this theme:

First, premiumisation as a margin lever, not just a growth lever. The shift from mass to premium products is not merely about top-line growth it structurally improves gross margins, reduces promotional dependence, and enhances brand equity. A company’s premium product mix percentage (and its trajectory) is a more useful metric than aggregate revenue growth.

Second, channel evolution as a structural driver. Quick commerce, modern trade, and e-commerce disproportionately benefit premium products because discovery and trial are easier, assortment is wider, and delivery convenience suits premium consumers. Companies that are investing in digital distribution and direct-to-consumer channels are building a structural advantage.

Third, the organised vs. unorganised shift. In categories like jewellery, fashion, eyewear, and personal care, the organised share of the market is still below 40-50%. The formalisation of the economy (GST, digital payments, compliance requirements) is a structural tailwind for branded/organised players, regardless of the macro environment.

Input cost inflation (crude-linked inputs, packaging, gold prices) can compress margins if premiumisation momentum stalls. Quick commerce channel economics remain evolving deep discounting by platforms can erode brand equity if not managed carefully. Rural demand recovery remains uncertain, which can constrain volume growth for mass-premium products. Consumer confidence is sensitive to employment trends and income growth.

Theme 10 - Banking: Quality Over Growth

Indian banks enter FY27 in a position of fundamental strength asset quality is the healthiest it has been in over a decade, capital adequacy is comfortable, and balance sheets are well-provisioned. The investment narrative has shifted from an asset quality clean-up (which drove the 2020-24 re-rating) to a growth and profitability optimisation phase, where the key questions are: how quickly can loan growth accelerate, how will NIMs evolve in a declining rate environment, and which segments offer the best risk-adjusted growth?

The sector is gradually shifting loan growth towards retail and MSME segments, while remaining selective in unsecured lending (following RBI’s macro-prudential tightening in late 2023). Deposit competition remains intense, which may keep NIMs range-bound. Private banks are generally preferred given more attractive valuations versus PSU banks, though select PSU banks with improving return profiles offer value.

What managements are saying:

ICICI Bank continues to deliver industry-leading profitability metrics with a well-diversified loan book and strong provisioning buffers. The bank’s focus on digital customer acquisition, cross-selling, and premiumisation of the retail portfolio is driving sustainable RoA of 2%+ levels.

Axis Bank has guided for asset growth of 300 bps above the industry average, with the retail and MSME segments driving incremental growth. The bank’s transformation under new management is yielding improving cost-to-income ratios and better cross-sell metrics.

IDFC FIRST Bank is executing a deposit-led growth strategy, with its high-quality savings franchise reducing funding costs and supporting NIM sustainability. The bank’s retail-focused model and high-yield consumer finance portfolio differentiate it from traditional banks, though credit cost normalisation remains a watchpoint.

City Union Bank represents the well-managed, mid-sized private bank archetype conservative underwriting, stable NIMs, healthy asset quality, and consistent dividend payouts. The bank’s focus on gold loans and MSME lending provides a niche positioning.

Equitas Small Finance Bank is leveraging its microfinance-to-SFB transformation to build a diversified retail bank with improving unit economics. The bank’s granular deposit base and focus on affordable housing/vehicle finance provide growth visibility.

Bandhan Bank expects NIM to remain range-bound as benefit from deposit repricing is offset by asset yield pressure. Management guided for a credit growth target supported by geographic and product diversification beyond microfinance.

Bank of India has guided for credit growth of 15-16% in FY27E, deposit growth of ~11%, and maintenance of RoA at 1%. The bank also expects an incremental credit cost of approximately 10 bps due to ECL adoption.

How an investor should think about this theme:

First, NIM sustainability is the key swing factor. In a declining rate environment (if RBI cuts further), banks with a higher share of floating-rate loans will see asset yields compress faster. The offset is deposit repricing banks with a higher CASA ratio and granular deposit base can manage the NIM compression better. Look for banks where the CASA ratio is above 40% and the deposit mix is tilting towards retail.

Second, credit quality is a lagging indicator. Current GNPA ratios below 2-3% are encouraging but reflect underwriting decisions made 2-3 years ago. The quality of recent vintage loans (post-Covid retail lending, unsecured personal loans, credit cards) will show up in asset quality only in FY28-29. Banks that were aggressive in unsecured retail lending during 2022-24 deserve closer scrutiny.

Third, opex leverage as the profitability lever. The next phase of bank earnings growth will be driven as much by operating leverage (technology investments reducing cost-to-income ratios) as by loan growth. Banks investing in digital infrastructure, AI-led underwriting, and straight-through processing will show widening efficiency gaps versus those relying on branch-led distribution.

Risks to monitor: NIM compression if rate cuts accelerate faster than expected. Unsecured lending asset quality deterioration. Competitive intensity in deposit mobilisation squeezing funding costs. Regulatory changes (ECL provisioning norms, risk weights on specific segments). Geopolitical or macroeconomic shocks affecting corporate credit quality.

Theme 11 - NBFCs: The New Specialists

The NBFC sector has evolved from a broad-based growth story to one defined by specialisation. The winners in the current cycle are companies that have identified specific lending niches affordable housing, gold loans, MSME financing, vehicle finance, micro-enterprise lending and are building deep underwriting expertise, operational efficiency, and technology-led scalability within those niches. The days of NBFCs competing with banks on generic lending are numbered; the survivors are the specialists.

What managements are saying:

Aadhar Housing Finance reiterated medium-term guidance of approximately 20% AUM growth, targeting a ₹500 bn loan book over three years with disbursement growth of 17-18%. Affordable housing demand is expected to remain resilient, supported by structural housing demand and PMAY-led subsidies. Spreads are expected to sustain above 5.5%. Exit cost of borrowing stands at approximately 7.7%, with FY27 borrowing cost guided at 7.7-7.75%. RoA is expected to remain stable, with RoE guidance of 17-17.5%.

Home First Finance Company India is another affordable housing specialist, with a technology-led underwriting model and direct sourcing strategy. The company’s focus on first-time homebuyers in the affordable segment (ticket size ₹10-25 lakh) provides a structural growth opportunity with lower competition from banks.

Mahindra & Mahindra Financial Services is India’s largest rural NBFC, with deep penetration in vehicle finance, tractor loans, and MSME lending in semi-urban/rural markets. The company’s extensive branch network and local market knowledge create distribution advantages that are difficult to replicate.

Can Fin Homes is focused on affordable housing finance, with a conservative underwriting approach and improving operational efficiency. The company’s connection with Canara Bank provides deposit and referral advantages.

Aye Finance is a technology-led micro-enterprise lender, focused on lending to micro and small businesses in underserved segments. The company’s data-driven underwriting approach and cluster-based lending model represent a differentiated approach to MSME credit.

MAS Financial Services operates a multi-product lending model spanning MSME loans, two-wheeler finance, and housing finance, with a focus on smaller-ticket, higher-yield segments.

Piramal Finance has completed its transformation from wholesale/real estate lending to a retail-focused NBFC, with growth driven by home loans, MSME, and personal loans.

How an investor should think about this theme:

First, niche depth vs. product breadth. The most successful NBFCs are those that have built genuine underwriting expertise in specific segments: affordable housing (Aadhar, Home First), rural/semi-urban vehicle finance (M&M Finance), gold loans (Muthoot, Manappuram), micro-enterprise (Aye Finance). Companies that try to be everything to everyone typically end up with weaker asset quality and thinner margins.

Second, operating leverage as the margin lever. Most NBFCs are in an investment phase building branches, hiring staff, and investing in technology. The key inflection point is when the cost-to-income ratio begins declining as the book scales. Companies guiding for 50-100 bps improvement in cost-to-income over the next 2 years are signalling this operating leverage phase.

Third, credit cost stability as the quality signal. In NBFC lending, the true cost of doing business is the credit cost provisions for bad loans. A company delivering 15% RoE with 1.5% credit costs is fundamentally different from one delivering 15% RoE with 0.5% credit costs. The latter is under-provisioned and carrying latent risk; the former has genuine, sustainable profitability.

Risks to monitor: Interest rate cycle rising rates help NIMs but can stress borrowers; falling rates help borrowers but compress spreads. Asset quality deterioration in micro-finance and unsecured segments. Regulatory tightening (RBI’s stance on NBFCs has become more prescriptive). Liquidity risk NBFCs remain dependent on wholesale borrowing, making them vulnerable to funding market disruptions. Competition from banks moving into NBFC lending segments.

Theme 12 - Capital Markets & Financialisation

India’s financialisation theme remains one of the most durable structural stories in the market. Mutual fund SIP flows have compounded at 20%+ annually, insurance penetration is rising, wealth management platforms are scaling, and the capital market infrastructure (exchanges, depositories, registrars, brokers) is seeing structural throughput growth. The total mutual fund AUM has crossed ₹65 lakh crore, and SIP monthly contributions are running at ₹25,000+ crore creating a self-reinforcing cycle of equity market participation.

What managements are saying:

360 ONE WAM continues to follow an advisory-first model, offering clients a portfolio view rather than a product view. Wealth Management AUM reached ₹2.17 lakh crore (ARR) in FY26, growing at a 30% CAGR over FY21-26. The company’s RM base of approximately 200 seasoned bankers (8-10 years of experience) represents a high-quality, high-productivity distribution capability. Management indicated that listed equity strategies currently earn yields of approximately 60 bps+, and fees are fairly stable.

HDFC Asset Management Company and Nippon Life India Asset Management continue to benefit from steady SIP flows and market expansion. The AMC business model offers operating leverage incremental AUM growth flows through at high margins given the fixed-cost infrastructure.

Aditya Birla Sun Life Asset Management Company is positioned to benefit from improving equity inflows and the structural shift towards passive and alternative products alongside active equity.

Computer Age Management Services (CAMS) and KFin Technologies are the picks-and-shovels plays on financialisation transaction processors and registrars whose revenues scale with AUM and transaction volumes across the mutual fund, insurance, and alternatives ecosystem. These businesses are asset-light, high-margin, and benefit from network effects.

Prudent Corporate Advisory Services represents the mutual fund distribution opportunity, with a rapidly scaling IFA (Independent Financial Advisor) network and growing SIP book.

BSE has seen significant growth in derivatives volumes and is increasingly diversifying into commodities, currency, and SME listings. The exchange’s operating leverage model means incremental transaction volumes flow through at very high margins.

Angel One is leveraging AI-generated content and expects AI investments to drive long-term cost efficiencies, representing the technology-led disruption in retail broking.

Motilal Oswal Financial Services is increasingly diversifying into alternatives, wealth management, and asset management alongside its traditional broking and institutional equities businesses.

Life Insurance Corporation of India and HDFC Life Insurance Company represent the life insurance segment, where protection penetration remains low relative to global benchmarks. ICICI Lombard General Insurance and Go Digit General Insurance represent the general insurance opportunity.

How an investor should think about this theme:

First, structural vs. cyclical. Within capital markets, certain businesses are structural (penetration-driven, with multi-decade compounding potential) while others are cyclical (volume-dependent, with significant correlation to market direction). AMCs, registrars (CAMS, KFin), insurance, and wealth management are primarily structural. Broking, investment banking, and proprietary trading are cyclical. A portfolio should be weighted towards structural plays.

Second, operating leverage as the dominant margin driver. Capital market infrastructure businesses (exchanges, registrars, depositories) have high fixed costs and low marginal costs — each additional transaction or unit of AUM flows through at near-100% incremental margin. Companies that have built scale already will see margin expansion accelerate as the industry grows.

Third, the alternative opportunity. The fastest-growing segment in wealth management is alternatives AIFs, PMS, real estate funds, and private credit. Companies building AIF and PMS capabilities (360 ONE, Motilal Oswal) are positioning for a higher-fee, higher-margin segment that is still in early stages of penetration.

Risks to monitor: Equity market corrections can temporarily reduce AUM (and therefore fee income), SIP flows, and trading volumes. Regulatory changes (SEBI’s TER framework, commission structures, F&O restrictions) can affect profitability. Competitive intensity in broking and distribution is driving fees towards zero in some segments. Technology disruption can commoditise distribution services.

Theme 13 - Internet & Technology Platforms

Indian internet companies are at an interesting juncture. AI is being positioned as an enabler rather than a threat, with vertical platforms (domain-specific, deeper context) better placed than horizontal models (broad, shallow). Near-term challenges are transient or segment-specific, while AI-led efficiency gains should help platforms solve more problems, improve user utility, and strengthen monetisation over time.

What managements are saying:

CarTrade Tech and BlackBuck stood out as vertical platform businesses with deepening competitive moats. CarTrade operates across the automotive marketplace (new, used, auctions), while BlackBuck (Zinka Technologies) is building a digital operating system for India’s trucking industry, a large, fragmented, and under-digitised market.

Affle (India)continues to benefit from the structural shift towards ROI-linked mobile advertising. Management expects AI to structurally accelerate ROI-led advertising adoption through better personalisation, automation, and audience targeting.

IndiaMART InterMESH is India’s largest B2B marketplace, connecting buyers and suppliers across manufacturing, industrial, and services categories. The platform’s network effects (more buyers attract more sellers and vice versa) create a durable competitive advantage.

Nazara Technologies operates across gaming, esports, and gamified learning segments where India’s young, mobile-first demographics provide a large addressable market with low current monetisation.

RateGain Travel Technologies is a SaaS platform for the travel and hospitality industry, providing data analytics, distribution, and brand engagement solutions. The company’s position as a mission-critical technology provider to hotels and airlines creates subscription-based recurring revenue.

Amagi Media Labs is a cloud-based SaaS platform for broadcast and connected TV (CTV), enabling content owners to launch, distribute, and monetise live and VOD content. The company’s NEWSPULSE agentic AI product targeting news networks represents the next generation of media technology.

Unicommerce eSolutions provides SaaS-based e-commerce enablement solutions order management, warehouse management, and multichannel selling for brands and retailers.

Protean eGov Technologies operates India’s tax processing (PAN) and pension (NPS) infrastructure, with expansion into GST and electronic invoice platforms. This is essentially a government infrastructure play with predictable cash flows and expansion potential.

How an investor should think about this theme:

First, vertical depth vs. horizontal breadth. The market is clearly rewarding vertical platforms (deep domain expertise, proprietary data, high switching costs) over horizontal platforms (broad but shallow, competing on price and convenience). Vertical platforms typically show higher gross margins, lower customer acquisition costs, and more predictable revenue.

Second, unit economics first, revenue growth second. For internet companies, the key valuation anchor is contribution margin and customer economics not top-line growth alone. A company growing at 25% with 50% contribution margins is more valuable than one growing at 50% with 10% contribution margins.

Third, AI as a margin lever, not just a product feature. Companies that are deploying AI to reduce their own cost structure (AI-generated content for customer support, AI-led fraud detection, AI-driven personalisation) are building operating leverage. Companies that are merely adding AI features to attract users without clear monetisation are burning cash.

Risks to monitor: Platform businesses are subject to network effects but network effects can work in reverse if user engagement declines. Regulatory risk (data privacy, digital competition, platform liability) is evolving globally. Competitive intensity from well-funded startups and global platforms. Unit economics can deteriorate during growth phases, masking underlying business model weaknesses.

Theme 14 - IT Services & Digital Engineering

Indian IT services companies are navigating the post-GenAI landscape, where the key question is no longer “will AI displace IT services?” but rather “where do Indian IT companies add genuine value in an AI-augmented world?” The answer is increasingly clear: domain-specific engineering, enterprise workflow automation, data platform modernisation, and regulatory-compliant implementations — areas where human judgment, industry knowledge, and system integration skills remain essential.

What managements are saying:

KPIT Technologies is positioned as a pure-play automotive software and embedded systems company, serving global OEMs on EV platforms, autonomous driving, and connected vehicle technologies. The company’s domain depth in automotive engineering differentiates it from horizontal IT services peers.

Mastek is focused on healthcare and government digital transformation, with a growing US healthcare technology practice. The company’s specialisation in Oracle and cloud-native applications provides niche positioning.

Indegene is a differentiated technology player serving the life sciences and pharmaceutical industry, with AI-led solutions for clinical operations, regulatory submissions, and medical affairs. The company’s deep domain expertise in pharma makes it less susceptible to AI-led commoditisation than generic IT services firms. We also last weekend did a deep dive into this business. Do check that out to find out how we find this to be a unique business - 1 AI proof IT Business?

Sonata Software and Zensar Technologies represent mid-tier IT services companies investing in cloud, data analytics, and digital engineering capabilities to differentiate beyond traditional application maintenance.

How an investor should think about this theme:

The post-GenAI IT services landscape rewards specialisation and domain depth. Companies that are vertical specialists (pharma IT, automotive software, healthcare tech) command premium valuations and margins versus horizontal IT services firms competing on headcount and rate cards. The key question for each company: “What do you do that GenAI cannot replicate or commoditise in the next 3-5 years?”

Risks to monitor: GenAI-led productivity improvements can reduce project sizes and headcount requirements for traditional IT services. Rupee appreciation can compress margins. Client budget compression during macro slowdowns. Visa and immigration policy uncertainty for US-dependent companies.

Theme 15 - Auto & Mobility Transition

The structural case: India’s auto sector is navigating multiple simultaneous transitions — EV penetration in two-wheelers and passenger vehicles, electrification of commercial fleets, rising electronic content per vehicle, and increasing export competitiveness. For auto ancillary companies, the key question is whether they are positioned for the increase in content per vehicle (more electronics, more sensors, more thermal management) or whether they are making components that become obsolete in an EV world (exhaust systems, ICE-specific parts).

Bosch is the quintessential auto ancillary platform with exposure to ICE, hybrid, and EV platforms across electronics, braking, thermal management, and mobility solutions. The company’s R&D depth and global technology access provide long-term competitive advantages.

Tata Motors continues to gain market share across key segments, with HCV market share reaching its highest level in nearly a decade. The EV portfolio across trucks, buses, and SCVs is expanding.

Sundram Fasteners , Sansera Engineering , Sandhar Technologies , Suprajit Engineering , and ZF Commercial Vehicle Control Systems India, Samvardhana Motherson represent the diversified auto ancillary space, where companies are mitigating EV transition risk by expanding into non-auto adjacencies (defence, aerospace, industrial) and increasing electronic content in their product portfolios.

Balkrishna Industries is a global leader in off-highway tyres, serving agriculture, mining, and industrial equipment — a segment with limited EV disruption risk and structural growth from global farm mechanisation.

Castrol India is navigating the ICE-to-EV transition by expanding into EV fluids and coolants, though the core lubricants business faces long-term structural headwinds from EV adoption.

Investor framework: Auto ancillaries with increasing electronic content per vehicle (sensors, ECUs, battery management systems, thermal management) are structurally advantaged. Companies with 40%+ revenue from non-auto applications (defence, aerospace, industrial, off-highway) carry lower transition risk. Focus on companies articulating a clear content-per-vehicle increase story alongside export growth.

Theme 16 - Textiles Revival

The Indian textiles sector is showing signs of genuine recovery after two to three years of weak demand and depressed profitability. The recovery is being driven by better spinning spreads, normalised cotton parity, strong Chinese demand for Indian yarn, and capacity rationalisation. India is also benefiting from sourcing shifts and disruptions in competing markets (Bangladesh political instability, China cost inflation), while the sector is moving towards higher-value areas such as garmenting, technical textiles, performance fabrics, and sourcing services.

Arvind is India’s largest integrated textile company, with operations spanning fabrics, garments, and advanced materials. Current garment capacity stands at 55 million pieces, with a target of reaching significantly higher levels. Management expects RoCE to recover from initial levels as new investments scale.

KPR Mill is a vertically integrated textile company (spinning to garmenting) with industry-leading margins, driven by operational efficiency, backward integration, and a growing garment export business.

Vardhman Textiles is India’s largest yarn manufacturer, benefiting from improved spinning spreads and better product mix (specialty yarns, dyed yarns).

PDS operates as a sourcing services platform for global fashion brands, with a capital-light model that is well-positioned to benefit from sourcing shifts away from Bangladesh and China.

Investor framework: Textile recovery investing is about timing and operating leverage. Companies with high fixed-cost bases (spinning, weaving) see dramatic margin expansion when utilisation improves. The China+1 tailwind is structural but not automatic — only companies with quality certifications, established buyer relationships, and competitive lead times will capture incremental orders. Watch for spinning spread normalisation, export order trends, and cotton-polyester parity as lead indicators.

Theme 18 - Infrastructure, Logistics & Cement

The structural case: India’s infrastructure build-out continues to provide a multi-year demand runway for cement, construction materials, and logistics services. Government capex on roads, railways, urban infrastructure, and water supply remains elevated, though execution timing can be lumpy. The cement sector is seeing gradual demand recovery, with pricing discipline returning after a period of competitive aggression.

Larsen & Toubro is the bellwether of Indian infrastructure, with an order book providing multi-year revenue visibility across power, defence, urban infrastructure, water, and transportation segments.

Kalpataru Projects International is focused on T&D contracting, railways, and civil construction, with a strong order book visibility. Management guided for FY27 order inflows of ₹300 bn, with an expected mix of approximately 60% T&D.

Afcons Infrastructure is a diversified EPC company with capabilities in marine, oil & gas, surface transport, and urban infrastructure. Management expects approximately ₹10 bn of receivables and contract assets to be realised in the near term.

The Ramco Cements is a well-managed South Indian cement company benefiting from capacity expansion and improving demand in its core markets.

Container Corporation of India is the dominant rail container logistics player, benefiting from the government’s push towards rail freight modal shift and dedicated freight corridors.

The Great Eastern Shipping Company remains focused on fleet renewal and balance sheet flexibility. Tanker day rates have reverted to pre-war levels as Middle East rerouting benefits fade, but firm asset prices and tight fleet supply continue to support the cycle.

Thomas Cook (India) (CMP: ₹91, Mcap: ₹43 bn, BUY) represents the travel and tourism recovery, benefiting from pent-up leisure demand, corporate travel normalisation, and the structural growth of outbound Indian tourism.

TVS Supply chain management is now looking to move to build a business around managing defence supply chain that is higher margin business as compared to the base business for them.

Investor framework: Infrastructure companies trade on order book visibility and execution track record. Look for companies with order book-to-revenue ratios above 2.5x, working capital cycles below 60 days, and improving cash flow generation. In cement, the key metric is cost per tonne companies with lower fuel and logistics costs per tonne have sustainable margin advantages. Logistics businesses should be evaluated on asset utilisation, yield per unit, and the balance between asset-heavy (fleet ownership) and asset-light (brokerage, technology platform) models.

Cross-Theme Risk Matrix