Chasing Uniqueness is better than Perfect ROCE

Why investing in unique capabilities can create more value than just chasing for perfection

What’s actually common across TD Power, Wockhardt, Sansera, HBL, Sai Life Sciences, Shilpa Medicare, Dynamatic, Privi, Acutaas, Motherson Sumi, Azad Engineering, Navin Fluorine, Data Patterns, Aditya Infotech and Amber Enterprises+Multiple other cos?

Strip away the stock charts and one trait binds this list together.

Each of these businesses kept investing in building unique capabilities without obsessing over what it would do to current ROCE and in doing so, seeded optionalities that are only now visible in the numbers. They sacrificed the return ratios of today to build capabilities that the market is rewarding today plus seven years. They looked past the quarterly print and asked a different question: what can this become five to seven years out?

That patience is what made them unique. The business world is a brutally competitive space. To stay differentiated, you have to be genuinely differentiated in the products you sell or the services you offer and that kind of difference is almost never built inside a single quarterly reporting cycle. It is built in the years when the reported ROCE looks ugly, the capacity sits idle, and the R&D line refuses to show up in revenue.

Here is how seven of these companies thought about the long term and why looking beyond reported ROCE is often where the real edge lies.

Just before going forward discussing any names here is the standard disclaimer that nothing in here is buy/sell recommendation and everything present in this blog is for educational purposes

1. Navin Fluorine - buying a capability in 2011, harvesting it a decade later

In 2011, Navin Fluorine acquired a 51% stake in UK-based Manchester Organics for ~£4.3 million (buying out the rest by 2015). On the surface it was a tiny deal. What it actually bought was cutting-edge fluorination chemistry and early-discovery R&D capability +The ability to undertake far more complex fluorination projects than a refrigerant gas and inorganics player ever could. For years this barely moved the needle. The CRAMS/CDMO division stayed small and revenue was lumpy: if an innovator’s molecule failed a trial, the campaign simply vanished.

Fast forward, and that 2011 capability is the engine of the story. The CDMO arm which is now rebranded Navin Molecular runs as a specialised outsourced partner for global pharma and biotech, and the company has moved from one-off campaigns to multi-year, dedicated long-term contracts (the Fermion supply agreement, the Chemours data-centre liquid-cooling fluids collaboration). The capability seeded over a decade ago is now showing up exactly where it should: in large, deliberate capex and in revenue visibility. The market took ~13 years to price what was effectively bought in 2011. Now, Navin has gone from one cGMP plant to 5 more.

2. TD Power Systems - building capacity when nothing was happening

TD Power had its own design capability up to ~55–60 MW. The strategic move was licensing two-pole generator technology from Siemens (up to ~250 MVA), a design capability it could not have built organically and then laying down capacity and global infrastructure through 2013–2020, precisely when India’s thermal power capex cycle was dead and the segment looked unloved. It set up subsidiaries across the US, Japan, Germany and a manufacturing base in Turkey while the reported economics gave nobody a reason to get excited.

Then the cycle turned. The global AI and data-centre buildout has created a structural new demand for reliable captive power, and industrial decarbonisation has piled on top. Revenue has gone from roughly 514 crore in FY20 toward an 1,800 crore annualised run-rate, with the Siemens-licensed high-speed generators now relevant for exactly the high-end turbine applications coming into demand. The dead decade of capacity-building was the optionality and it’s just that the numbers needed the world to catch up. Always track capabilities by being a business analyst. Technicals will guide you about the right time to enter. But being prepared is what Fundamentals of a business teaches us.

3. Privi Speciality Chemicals - a decade of R&D off the listed balance sheet, now merging in

Privi’s quiet edge has been Privi Biotechnologies, which has run a biotechnology R&D lab since ~2008–09 which is a multidisciplinary team pursuing eco-friendly, renewable-feedstock routes to aroma chemicals. This was patient, founder-backed R&D incubated largely outside the listed entity’s reported numbers for over a decade, generating a stack of process know-how and a pipeline of patents that never had to justify itself against quarterly ROCE.

The merger of Privi Fine Sciences and Privi Biotech into the listed company is the moment that optionality becomes visible. It simplifies the structure and unlocks the decade-long R&D into green/biotech-route specialty molecules, super-specialty aroma chemicals, and even tech-licensing/franchising possibilities into the platform that the market actually values. Add the de-risking the management is engineering (no single product to contribute more than ~10% of EBITDA by FY29) and you have a differentiated portfolio that was a cost centre for years before it became the core thesis.

4. HBL Power Systems (HBL Engineering) - pioneering Kavach in the 2000s, monetising it after 2020

HBL was the first company to respond to the Indian Railways’ (RDSO) expression of interest for an indigenous anti-collision device back in 2008, and it ran the early Train Collision Avoidance System (TCAS) demo trials around 2012. For well over a decade, railway electronics was a small slice of the business (~10% of revenue) and carried disproportionate development effort relative to what it earned, a classic case of R&D and capability spending years ahead of monetisation.

The inflection came when Kavach was adopted as the National ATP System in July 2020. Today HBL is the only player with RDSO approval for the latest Kavach version, sitting on a multi-thousand-crore order book, with the Railways’ multi-year network rollout still ahead. The capability was built a decade before the order book validated it.

5. Data Patterns - the highest margins in the industry, by design

Data Patterns earns the richest margins in Indian defence electronics with EBITDA margins that have ranged from the high-30s to the mid-50s percent in recent quarters, versus the assembly-heavy economics of much of the peer set. The reason is structural: it is one of the very few vertically integrated defence-electronics players, designing and building the electronic building blocks boards, sub-systems, test equipment and the underlying IP in-house, essentially chip-to-system. It doesn’t bolt together other people’s modules; it owns the design.

That in-house, IP-led integration is the entire uniqueness. Because Data Patterns owns the design of the radars, electronic warfare suites and avionics embedded in programmes like Tejas, the BrahMos ecosystem and naval/airborne platforms, it is deeply embedded and hard to substitute and it captures the design value rather than just the manufacturing value. The company has been at this for 35+ years (as the erstwhile Indus Teqsite); the margin profile and the stickiness are the compounded payoff of that long, unglamorous investment in owning the full stack.

6. Wockhardt - two decades of antibiotic R&D, finally crystallising

This is the purest sacrifice today for tomorrow’s case on the list. Wockhardt has run a ~140-scientist drug-discovery programme on novel antibiotics for over two decades, with roughly $500 million ploughed into R&D over 25 years, a spend the market repeatedly wrote off through years when the company’s headline financials gave little reason for optimism. The ValuePickr Wockhardt thread is a great chronicle of exactly this journey: a balance sheet under strain, a promoter who refused to abandon the science, and a slow accretion of a six-antibiotic pipeline, all carrying USFDA QIDP designations.

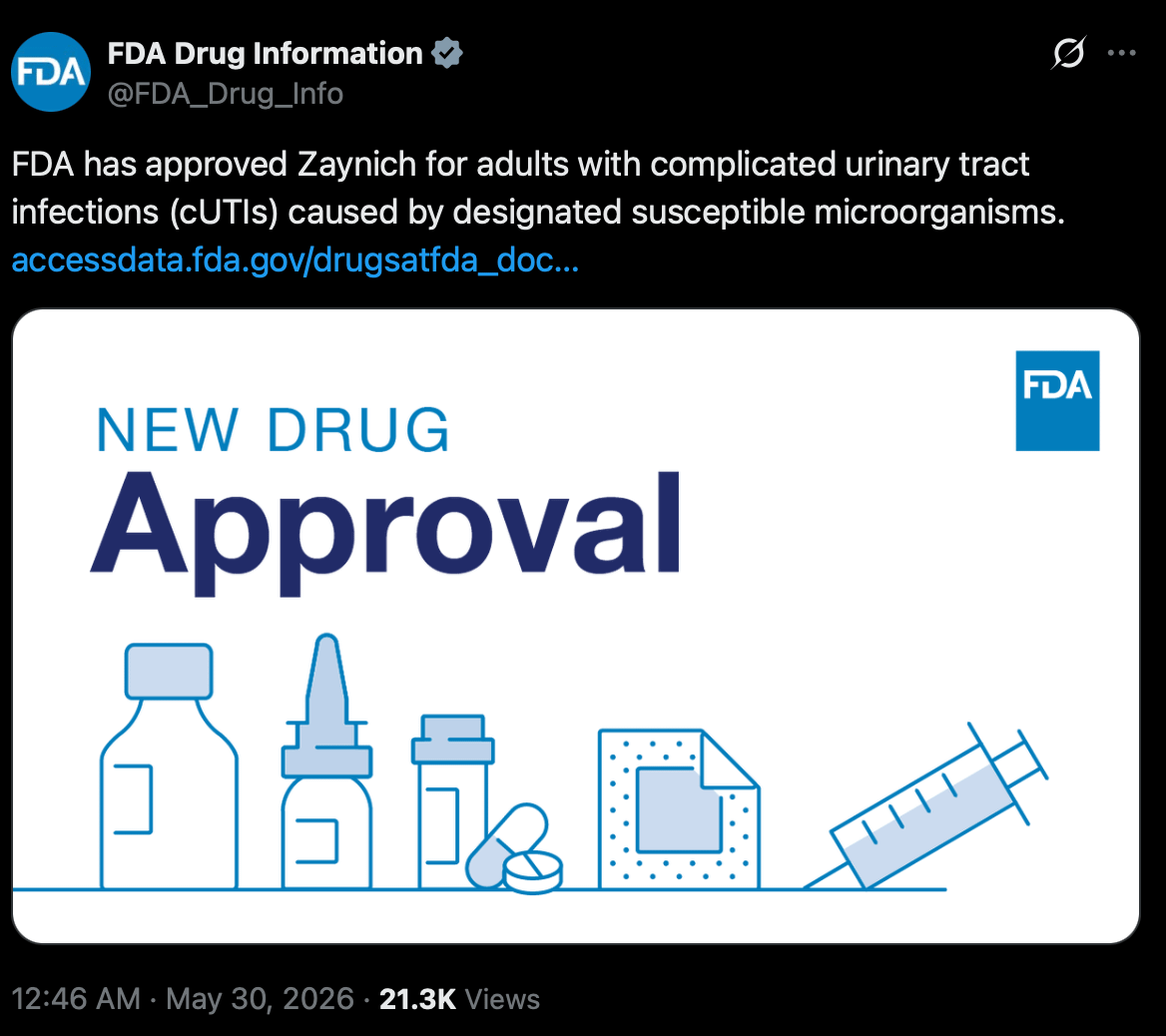

The crown jewel is WCK 5222 / Zaynich (cefepime + zidebactam) a first-in-class β-lactam enhancer mechanism and the first New Chemical Entity discovered and developed in India to reach a US NDA and an EU MAA.

The pivotal ENHANCE-1 Phase III trial showed statistical superiority over meropenem, and under compassionate use the drug has saved roughly 45–50 critically ill patients globally. Just this week (end-May 2026) Wockhardt received CDSCO (Indian) marketing authorisation for Zaynich in cUTI. Note the precise regulatory status, because it matters: the US FDA NDA was accepted in December 2025 and is under Fast Track + priority review, with a decision expected mid-to-late 2026 and a US launch targeted for FY27; the EU MAA was filed in January 2026 under accelerated assessment. And now FDA has approved Zaynich for adults with complicated urinary tract infections (cUTIs) caused by designated susceptible microorganisms. (accessdata.fda.gov/drugsatfda_doc)

7. Shilpa Medicare - big capacities and a fistful of optionalities, ahead of the revenue

Shilpa has spent years building capability and capacity ahead of the revenue that would justify it, the textbook depressed-ROCE-by-choice profile. The flagship optionality is recombinant human albumin (rHA / NavAlbumin): Shilpa is the first Indian company to take this animal-free, fermentation-derived albumin through human trials (Phase 1 completed in 2024), it has now received approval for a global Phase III study, and it has an Orion Corporation partnership already paying milestone money. This is a genuinely novel, hard-to-replicate biologics capability.

And it doesn’t stop at albumin. Shilpa has seeded a stack of optionalities on top of large, currently under-utilised capacity: an integrated ADC (antibody-drug conjugate) manufacturing platform, transdermal patches (Rotigotine targeting Europe in FY27), orally disintegrating films, biosimilars (Aflibercept, Nivolumab with approvals expected around FY27), complex injectables and 15+ new oncology APIs. Plants like Unit VI at Dabaspet (with US FDA EIR in hand) sit ready to be filled. Each one of these depresses ROCE today because the capacity and development spend are in the books while the revenue isn’t and each is an option that monetises as the products commercialise. Recent concalls make the management’s framing explicit: leverage the under-utilised assets, commercialise the differentiated pipeline, and let profitability follow.

So how do you actually find these businesses?

The uniqueness in every example above took years to show up in the numbers which is precisely why the market under-prices it while it’s being built. The edge is recognising the capability before it lands in the reported ROCE. A few things to look for:

1. Investment running ahead of revenue and the discipline to tell the two apart. Look for rising R&D-as-%-of-sales, heavy capex, and low capacity utilisation that depress today’s return ratios. The hard part is distinguishing genuine capability-building from plain value destruction. A depressed ROCE caused by a company seeding a real, differentiated capability is an opportunity; a depressed ROCE caused by serial diworsification into commodity capacity is a trap. The question to keep asking: is there a credible path to monetising this, and is the capability actually hard to copy?

2. A capability that is genuinely difficult to replicate. Proprietary IP and complex chemistry (Navin’s fluorination, Privi’s biotech routes), regulatory moats (Wockhardt’s USFDA QIDP/NCE status, HBL’s sole RDSO approval, Shilpa’s first-in-India biologics), vertical integration and design ownership (Data Patterns), or a licensed-then-localised design capability (TD Power). If a competitor could buy the same outcome with a purchase order next quarter, it isn’t optionality.

3. Optionality that exists but isn’t yet in the P&L. Pipelines, filed patents, regulatory approvals pending, acquired capabilities (Manchester Organics), new chemical entities, idle-but-ready capacity, new verticals. The value is real but invisible to a screener filtering on trailing ROCE or P/E.

4. Management that openly thinks in 5–7 year arcs. Read concalls and annual reports for why the company is spending, not just what it earned. Founders building this kind of business will tell you they’re willing to look ugly on near-term ratios; they reinvest rather than optimise for the next print. Then hold them accountable — track guidance versus delivery over time, because credibility is the difference between a visionary and a value-destroyer.

5. Comfort with the lag. In every single case here, there was a multi-year gap between the spend and the recognition — Navin’s ~13 years, HBL’s decade, Wockhardt’s two decades, TD Power’s decade. The numbers always show up late. If you need the income statement to confirm the thesis before you’ll act, you’ve already given up the edge.

Before we move to the other side of the coin, a quick note for readers who think the way this piece thinks.

Every business discussed in this blog like the ones building capabilities years ahead of the P&L and they didn’t just appear in a screener one morning. They were found through a process: studying industry structures, reading concalls for what management is spending on rather than what they earned, and tracking capability-building across quarters before the market notices.

That’s exactly what we do inside SOIC Long Term Research.

Our TVGP Watchlist is a curated universe of roughly 50 businesses that we track continuously using our internal framework: Theme, Value, Growth, and Promoters. Many of the ugly ROCE, unique capability businesses you just read about sit inside this watchlist identified early, tracked deeply, and studied over time rather than chased after the stock has already moved.

Every Sunday, we run a live session breaking down one company from this watchlist in detail industry structure, business mechanics, growth triggers, risks, and valuation context. Over time, this builds a structured repository of business analysis rather than isolated stock notes. All session recordings are accessible to subscribers in our research library.

If studying businesses this way resonates with you — finding the Navin Fluorines and TD Powers of the world before the income statement confirms the thesis — the broader watchlist and research library is here: 👉 Explore SOIC Long Term Research

One more thing before we go to next section

Learning to distinguish a depressed ROCE that’s hiding a future compounder from one that’s hiding a black hole. That skill isn’t something you pick up from a single blog post. It’s built through repetition studying business after business, framework after framework, cycle after cycle.

That’s what the SOIC Membership is designed for.

Our webinars and micro-courses walk you through exactly this: how to read a business like an analyst, how to spot capability-building before it shows up in the numbers, and how to avoid the traps where cheap is just broken. Everything from financial modelling to industry mapping to the behavioural traps that make investors sell too early or hold too long.

Exclusive SOIC Membership + StockScans Bundle 👉 Explore and join here

📌 Kindly use a browser to enrol — mobile apps apply additional (30%) charges 🎟️ Limited Period Coupon Code: SOICSCANS

Getting Back to the blog

Let me explain you the other side of the picture when picture-perfect ROCE stops working for you -

Everything above was about businesses where the ugly ROCE print was hiding a future compounder. But there is a mirror image to that story, and it’s equally important.

Some of the most celebrated businesses in Indian markets, the ones that ran a picture-perfect ROCE for a decade or longer are now teaching investors a different and arguably more painful lesson: buying perfection at the price of perfection leaves you nowhere to go.

The ROCE didn’t become perfect overnight. It was built over years, sometimes decades, by exceptional operators running tight supply chains, owning distribution, and reinvesting intelligently when competition was light. The problem is what comes after. Once a company has optimised its return ratios to near-theoretical limits, the question isn’t whether the business is great it obviously is the question is whether the incremental outcome from here justifies what you’re paying. And in case after case, the answer has been: probably not, especially when the competition finally shows up.

1. Asian Paints - when a 10,000 crore cheque cracked the moat

For two decades, Asian Paints was the single most cited example of a high-ROCE compounder in India. ROCE consistently north of 30%, market share above 55% in decorative paints, and a distribution network that no competitor could replicate. Berger, Nerolac, Akzo everyone tried, nobody could break the grip.

Then Kumar Mangalam Birla wrote a 10,000 crore cheque (which is just ~6.5% of the company’s fixed asset base but is more than the fixed asset base of Asian Paints). Grasim launched Birla Opus with three of six factories going live on day one, 2,300+ colour shades on the shelf, pricing 5–7% below Asian Paints, and smaller, next-gen tinting machines that won dealer loyalty. By March 2025, Birla Opus had entered the top three decorative paint brands by revenue. By September 2025, Asian Paints’ market share had slipped from roughly 59% to about 52%, with Birla Opus capturing approximately 6–7% of the organised market. JSW Paints, merged with AkzoNobel India, piled on with its own price cuts and dealer schemes.

The stock tells the story. From a 52-week high of 3,395 in September 2024, Asian Paints corrected to a low of 2,125 by March 2025, a 30%+ drawdown. Q3 FY26 revenue grew just 4% year-on-year with net profit actually declining 4.6%. Trade receivables (debtors) have been growing at 19% annually a sign that channel terms are loosening under competitive pressure. Despite the correction, the stock still trades at a P/E of ~64 and a P/B of ~13. Operating margins, which were the company’s hallmark, stood at 20% in Q3 FY26.

The ROCE is still respectable. The business is still the market leader. But the decade when Asian Paints could grow at 15%+ top-line with 25%+ margins, undisturbed, is over. The incremental return from here depends on how it fights a price war not on the compounding machine it once was.

2. Hindustan Unilever - the gold standard that stopped compounding

HUL is arguably the highest-quality FMCG franchise in India. Nine out of ten Indian households use at least one HUL product. 50+ brands, market leadership across fabric wash, personal wash, cosmetics, shampoos. ROCE comfortably above 100% in some years. A balance sheet with effectively zero debt.

And the stock has been dead money for nearly five years. HUL hit a record high of roughly 2,859 in September 2021. As of today, after every rally and selloff in between, the market cap is about 5.06 lakh crore and the stock is trading well below that 2021 peak. Five-year sales CAGR is just 6.5%. In FY25, revenue was 60,700 crore up 2%. Pricing was essentially flat; the company chose to cut prices in home care to defend share. EBITDA margins dipped to ~23.5%, squeezed by commodity inflation in palm oil, tea and coffee that wasn’t fully passed through.

What changed? The world HUL was built for where a handful of mass brands dominated through TV advertising and general trade is fragmenting. Digital-first D2C brands (think Mamaearth, XYXX, The Derma Co) carved out niches in skincare, innerwear, and personal care. Quick commerce reshaped purchase frequency. Regional brands undercut on price. Younger consumers stopped treating legacy brands as default choices. HUL is explicit that it’s taking the pain now by elevating ad-spends, distribution, and tech but that is exactly the point. Defending a mature franchise requires reinvestment that compresses margins, and if the growth it buys is low-single-digits, the stock simply cannot compound the way it did from 2010 to 2020. The business is still exceptional. The stock just isn’t.

3. Page Industries - a 60%+ ROCE that the stock couldn’t outrun

Page Industries, the exclusive licensee for Jockey in India, has run ROCE in the 50–85% range for the better part of a decade. ROE north of 45%. Debt-free. In-house manufacturing, an aspirational brand, distribution in 2,700+ cities. By every screener metric, this is a perfect business.

The stock peaked around 50,470 and today sits roughly 24% below that level at about 38,000. FY25 revenue of 4,935 crore grew at 8% solid, but a far cry from the 14% ten-year CAGR the company used to deliver. More telling, Q4 FY26 saw net profit decline 5.6% quarter-on-quarter even as revenue grew 14% year-on-year, because operating margins compressed from ~23% to ~21%.

The bull case for Page was always that Jockey’s brand moat in premium innerwear was impenetrable. But digital-first innerwear brands like XYXX, DaMENSCH, Bummer have nibbled at the premium end. Athleisure overlap from brands like Lululemon and Nike’s DTC push is real. And at 52x trailing P/E, the market was pricing in a growth rate the company was no longer delivering. The ROCE stayed perfect but the growth that justified the multiple didn’t, and the stock has been a frustrating hold for anyone who bought it at those multiples.

4. Pidilite Industries - Fevicol’s 70% market share, 3% stock return in three years

Pidilite is the other poster child of the “great business, buy and hold forever” thesis. Fevicol commands a 70% market share in adhesives. Dr. Fixit leads in waterproofing. Over 25 brands, 1,300+ SKUs, a distribution network that reaches carpenters and contractors in every tier of the country. The moat is deep, the brand is iconic, and the business has compounded steadily for decades.

Yet the stock has gained only about 3% over the past three years, while the BSE500 moved meaningfully higher. Over the last year, Pidilite’s stock has actually declined roughly 6-7% against the Sensex’s gain, producing a negative alpha of over 12%. The P/E sits around 69x, the P/B at 13.7x. Analysts flag that expectations for growth are already embedded in the price, leaving limited room for multiple expansion.

Q2 FY26 revenue grew ~10% year-on-year but operating margins contracted sequentially, and the quarterly net profit declined ~14% from Q1 to Q2. Competition from domestic and international specialty chemical players is intensifying, raw material costs remain volatile, and the construction cycle that drives adhesive demand is lumpy.

Nobody is saying Fevicol’s moat is broken. The point is different: when you buy a 70% market-share monopoly at 70x earnings, you need everything to go right and even then the mathematics of incremental compounding become brutal. A 10% earnings growth on a 70x P/E stock does not create wealth the way a 40% ROCE inflection on a 15x P/E stock does.

5. Relaxo Footwears - the most dramatic fall from grace

This might be the starkest example. Relaxo was a market darling through 2021: India’s largest non-leather footwear manufacturer, dominant in the mass EVA/rubber slipper segment, with ROCE that had been consistently strong, revenue growing at double digits, and a stock that peaked near 1,400 in November 2021 trading at 90x+ earnings.

Today the stock is around 350. That’s a 75% drawdown from peak. Market cap has shrunk to roughly 8,600 crore. Five-year sales CAGR is 2.75%. ROE has collapsed to ~9%. FY26 revenue actually declined 3% year-on-year to 2,702 crore.

What happened? Raw material prices spiked 2.5x in 2022, and Relaxo’s long supply chain with pre-contracted international inputs meant its costs stayed high even after spot prices in India declined. Local, unorganised manufacturers buying from the domestic spot market became sharply cheaper. Relaxo’s core consumer, extremely price-sensitive, mass-segment buyers simply switched to cheaper alternatives. Volumes crashed 15% in Q2 FY23. The company took aggressive price cuts to claw back share, which gutted margins: EBITDA fell from 16% to under 9%. The CFO resigned. The earnings power the market had priced in at 90x PE never materialised.

Relaxo’s ROCE looked excellent in 2019–2021 not because the business had a hard-to-replicate capability, but because the cycle was favourable and unorganised competitors hadn’t yet closed the price gap. The moment the macro turned, it became clear that cheap footwear at scale, without genuine IP or brand premiumisation, wasn’t a moat, it was a cost advantage that evaporated as the second input economics shifted.

The pattern across all five -

In each of these cases, the ROCE was genuinely world-class, not manufactured, not leveraged, earned through years of operational excellence and market dominance. The businesses were real. The problem was never the business quality; the problem was what the market was paying for that quality and what happened to the incremental growth once the franchise matured or competition caught up.

When a company already earns a 30–80% ROCE, operates at dominant market share, and trades at 50–90x earnings, the maths of future compounding works against you. The ROCE can stay high and the stock can still go nowhere for years, because the market has already priced in the entire runway.

And when competition finally shows up whether it’s a 10,000 crore Birla Opus, a wave of D2C insurgents, or the unorganised sector arbitraging a raw material cycle it doesn’t need to destroy the business. It just needs to slow the growth rate by a few percentage points. On a 70x P/E stock, even a 2–3% growth deceleration can trigger years of multiple de-rating.

Contrast this with the businesses in the first half of this piece. When a company like HBL or TD Power or Navin Fluorine is seeding a capability building Kavach a decade before the orders, licensing Siemens generators while thermal capex is dead, acquiring Manchester Organics for £4.3 million the ROCE looks ugly, the capacity sits idle, and the stock trades at undemanding multiples. But the capability is real, the optionality is accumulating, and when the cycle or the regulatory or the end-market tailwind finally arrives, the earnings inflect violently upward and the multiple re-rates at the same time. That double-barrelled impact earnings inflection plus multiple expansion is where the asymmetric returns live.

The picture-perfect ROCE stocks give you one engine: the compounding of an already-optimised business, priced at perfection. The ugly-ROCE-hiding-uniqueness stocks give you two: the inflection in the numerator and the re-rating in the denominator. One is arithmetic; the other is geometric. And the gap in terminal wealth is where the entire investing edge sits.

In short: the great businesses optimise for the capability, not the quarter. The reported ROCE of a company in the middle of seeding optionality is one of the most misleading numbers in investing. Sometimes it’s hiding a future compounder, sometimes it’s hiding a black hole. Doing the work to tell which is which is, in the end, the whole job.

Superb!

Awesome Read