Craftsman Automation: Crafted for Auto Revival

In today’s term when you listen to interviews of any legendary investor, portfolio manager or PMS Fund or their views on social media via tweets, blogs or podcasts one thing is very common, most of them are bullish on two sectors one is capex cycle and the other is automobiles and when dig further they are more bullish on commercial & passenger vehicles which is also reflecting in last few quarters numbers as well and main buzz word here is Electric Vehicles (EV).

So as investors we also like to play this theme and studied various companies in both the sectors, but one problem we find in the automobile industry is they are highly cyclical and second is stock prices of these companies had shown a good run up in last few months which leads to very less margin of safety for new entrants. When we look at infrastructure companies for capex, the problem here arises is dependence on government spending and poor balance sheets and long working capital cycle of these companies.

To play these themes, at SOIC we look for proxy companies which could benefit from these trends with a medium to long term time horizon. As these companies are not well covered on the streets, available at much better valuations and provide margin of safety. When we go for proxy beneficiaries, without taking balance sheet risk, one can invest in the best of the franchises and keep compounding wealth.

We have also covered the proxy investing themes in the past as well like refractories for steel cycle, cable & wire , steel tubes for real estate sector and rings & cages for the bearing sector which itself is proxy to capex revival.

One such proxy company we will be discussing today is Craftsman Automation Ltd which is a proxy for both sectors Automobile as well as Industrials.

Craftsman Automation Ltd, established in 1986, is a diversified engineering company with vertically integrated manufacturing capabilities. The company has 12 strategically located manufacturing facilities across 7 cities in India which includes 1 flagship facility, 8 satellite facilities (these facilities are located strategically near the major automotive manufacturing hub to provide Just in Time supply to the customers facilities within hours) and 3 integrated facilities with a total built-up area of 1.6 million sq. ft. close to some of the key customers to enable meeting customers’ just-in-time delivery schedules, allow economies of scale and logistical advantages for the customers, and to insulate them from local supply or other disruptions.

The company has also proposed 4 new plants across the country to cater their customers. The company has one wholly owned subsidiary company in the Netherlands Craftsman Europe B.V and one Joint Venture in India with 30% stake in Carl Stahl Craftsman Enterprises Pvt. Ltd.

Company is engaged in three business segments:

1) Automotive – Powertrain and Others: This is the flagship division of the Company, catering to diverse categories within the automotive segment and serving the needs of marquee clients in both domestic and export markets. This segment contributes ~52% of the revenue and 79% of the EBITDA of the company.

2) Automotive – Aluminium Products: Craftsman’s key products in this products segment include highly engineered products that consist of Crank Case and Cylinder Blocks for two wheelers, engine and structural parts for passenger vehicles and gear box housing for heavy commercial vehicles. It also supplies high pressure, low pressure, gravity and sand aluminium die castings, precision machined in ready-for-assembly condition to major OEMs.

This segment contributes to around 20% of the revenue & just 2.5% of the EBITDA. In Q1 FY2023 the company integrated the industrial aluminium business with the auto aluminium and now call this segment as Aluminium Product Segment.

3) Industrial and Engineering: This segment is divided into two sub-segments, Contract Manufacturing and Storage Solution & Material Handling. Craftsman forayed into the high margin storage solution with a slew of products that cater to the warehousing sector, in keeping with the huge demand for sophisticated warehousing solutions to cater growth in e-commerce in India. This segment contributes to around 28% of revenue and 18% of the EBITDA of the company.

Let’s dig deeper into each of its business segments with their growth plans and details of their key products:

Automotive – Powertrain and Others:

In automobiles, a powertrain generates power and transmits it to the wheels. It can be broadly classified into four components – (i) engine and engine parts, (ii) transmission, (iii) driveshaft, and (iv) rear axle. The engine burns the fuel to produce mechanical power. It comprises several critical components, including cylinder block, cylinder head, and crankshaft, pistons, camshaft, and engine valves.

Products in the Automotive – Powertrain and Others segment are highly engineered and require advanced manufacturing processes to maximize end user performance, with end users including OEMs producing commercial vehicles, special utility vehicles, tractors and off-highway vehicles.

Key products in this segment include engine parts such as cylinder blocks and cylinder heads, camshafts, transmission parts, gearbox housings, turbo chargers and bearing caps, catering to CV, SUV, tractor and off highway OEMs.

The company is the largest player involved in the machining of cylinder blocks and cylinder heads in the intermediate, medium and heavy commercial vehicles segment as well as in the construction equipment industry in India and is also among the top 3-4 players in the machining of cylinder blocks for the tractor segment in India.

Powertrain business is a high margin business (~36%) as mainly involved in machining and value addition, this division procures RM (casted products) either from suppliers or from OEMs.

Cylinder block is the supporting structure of the engine on which all engine parts are mounted. It houses the cylinder, which gives the engine its power. The cylinder block for commercial vehicles (CVs), off-road vehicles, sports/multi-utility vehicles (SUVs / MPVs), and tractors uses cast iron.

The next key product is Cylinder head, it covers the cylinder and helps the head gasket seal the cylinders in order to build enough compression for the engine operation. Similar to a cylinder block, cylinder heads are also manufactured by the process of casting using ferro alloys.

Now comes Transmission, commonly known as the gearbox, which transmits power to the wheels through the drive shaft and rear axle. Auto-component companies are engaged in casting, forging and machining of engine parts, transmission parts housing, drive shaft, rear axle housing, etc.

Transmission is a set of gears within a casing that allows controlled application of the power using different gear ratios. The switching of gears can be done manually by the driver of the vehicle or automatically, depending on the type of transmission used in the vehicle. In India, manual transmission is used for CVs and tractors, while automatic transmission is used for SUVs.

Key Growth driver for this segment are:

Wide product range and market leadership in cylinder blocks and cylinder heads gives a competitive moat

They are present across the entire value chain in the Automotive- Aluminium Products segment, providing diverse products and solutions.

They offer comprehensive one-stop solutions to their customers including design, process engineering and manufacturing including foundry, heat treatment, fabrication, machining and assembly facilities. They are diversified across end-user industries and cater to commercial vehicles, two-wheeler, tractor and other segments.

They actively pursue cross-selling opportunities across segments to derive value for their existing and prospective customers. This not only helps them in solving complex customer problems that require multi-domain expertise but also helps them in penetrating customers’ different business segments and enhancing their capabilities to collaborate with OEMs right from the designing of their new products. Their diversified presence across various segments and design capability provides them with the flexibility to operate successfully across business cycles and mitigate any fluctuations in the industry.

Craftsman caters to all automotive segments:

2) Long term and well established relationships with marquee domestic and global OEM:

The company has strong long-term relationships with a number of marquee OEMs (domestic and global) as well as component manufacturers across its three business segments.

It is considered as a strategic and preferred supplier by many of its OEM customers and is also the single source supplier in certain product categories for some key customers. Most of its business involves direct supplies to OEMs under long-term agreements, which are renewed from time to time.

These can also be verified from their numbers, more than 70% of its revenue comes from its customers who have more than 10 years relationship with the company.

Their key customers include Daimler India, Tata Motors, Tata Cummins, Mahindra & Mahindra, Royal Enfield, Mitsubishi Heavy Industries, Siemens India, Escorts, Ashok Leyland, Simpson & Company, TAFE Motors and Tractors, Perkins India, John Deere and JCB India.

3) Proxy to the domestic CV growth story:

The powertrain division has substantial dependence on the Medium & Heavy Commercial Vehicle industry. Craftsman is an ideal play on the ongoing revival in the M&HCV demand.

Company expects a strong cyclical recovery in the domestic CV industry during FY22E-24E, which would likely be driven by a fast normalizing economic activity, revival in government spending (road building, construction & infra) and an improving retail financing environment.

Pick-up in replacement demand, triggered by multi-decade high average fleet age provides an additional tailwind.

Craftsman is fast gaining traction with its key customers like Tata Motors and Daimler India have been gaining retail market share in heavy goods i.e, trucks category over the past several years. Craftsman has 100% share of the business of Daimler India (sole supplier to Daimler).

4) Implementation of BS VI emission norms:

The effect of BS-6, with respect to value addition, has yet to reflect fully in revenues. Company is expecting this to be seen in FY 22-23. This will lead to an increase in realizations due to additional content in between 25- 40%.

Along with that, Pick-up in replacement demand, triggered by multi-decade high average fleet age provides an additional tailwind.

The next business segment is Automotive – Aluminium Products

The Automotive - Aluminium Products segment is a recent addition to Craftsman’s portfolio. The company established this segment in 2014, despite being a relatively new entrant in the highly competitive aluminium die-casting space, Craftsman has established a strong reputation as a dependable partner for leading automotive OEMs operating in India and other customers from diverse sectors.

The Company is involved in the end-to-end manufacturing (casting + machining) of products such as crank case and cylinder blocks for 2Ws, engine and structural parts for passenger vehicles and gear box housings for MHCVs.

Among a limited set of Indian manufacturers to have capabilities in all of high-pressure die casting, low-pressure die casting and gravity die casting. Under this segment, the company undertakes product sales & machining services and caters directly to domestic and export markets.

Given its technical capabilities and strong execution track record, Craftsman continues to grow its business with key customers in the face of growing competition.

Company has incurred significant capital expenditure in the past few years, including setting up an entire range of facilities such as no-bake sand foundry, high pressure, low pressure and gravity die casting capabilities for production of various types of aluminium castings for different applications for its customers, allowing them to offer a diverse product suite, reduce operating costs and drive its productivity. These capacities are not yet fully utilized and provide ample room for growth.

Post implementation of BS-VI, most OEMs explored various possibilities to light-weight their vehicles by using non-ferrous metals like aluminium to reduce carbon emission. With OEMs seeking to further reduce the weight of their vehicles, increased use of aluminium offers attractive growth prospects for companies like Craftsman.

Currently 80% of revenues come from the 2 wheeler segment with major contributors being TVS motors and Royal Enfield. The company is looking to expand its business in the PVs segment through winning new business from PSA and other OEMs.

Key Growth driver for this segment are:

Global trend shifting towards aluminium castings to meet tight emission norms/EV needs

Globally, OEMs are shifting from steel to aluminium castings to lower a vehicle’s overall weight, in order to increase fuel efficiency and meet new tighter emission norms like World Harmonized Light-duty Vehicles Test Procedure (WLTP) and Real Driving Emissions (RDE).

Aluminium content per average PV in Europe at ~180 kgs is 3x+ the average Aluminium content in Indian PVs; expect the structural trend of light weighting to bridge this gap over the medium term; Aluminium content in EV PVs to also increase, factoring in redundancies of certain aluminium ICE parts used in engines and transmissions

A key growth driver for the segment is the increasing use of non-ferrous metals like aluminium for vehicle light-weighting.

2) EV opportunities in aluminium for Craftsman

Company’s existing facilities in this segment - in Bangalore and Coimbatore - are in close proximity to major EV 2 Wheeler OEMs including Ola Electric and Ather, heightening possibilities of supplies to these OEMs with growing underlying volumes.

From the 2 wheeler segment the company currently caters to TVS motors and Royal Enfield.

3) New client wins to accelerate momentum

Initially, this segment primarily catered to 2W (TVS Motor, Royal Enfield). In recent years, Craftsman has been able to expand its customer set to CV (Daimler) and PV (M&M), thereby substantially expanding the addressable market.

Incremental order wins for the segment should continue from CVs/PVs, enabling Craftsman to quickly de-risk from 2Ws. The company is also witnessing traction in requirement of aluminium parts for exports (Stellantis order; queries from North America for aluminium casting parts and EV buses).

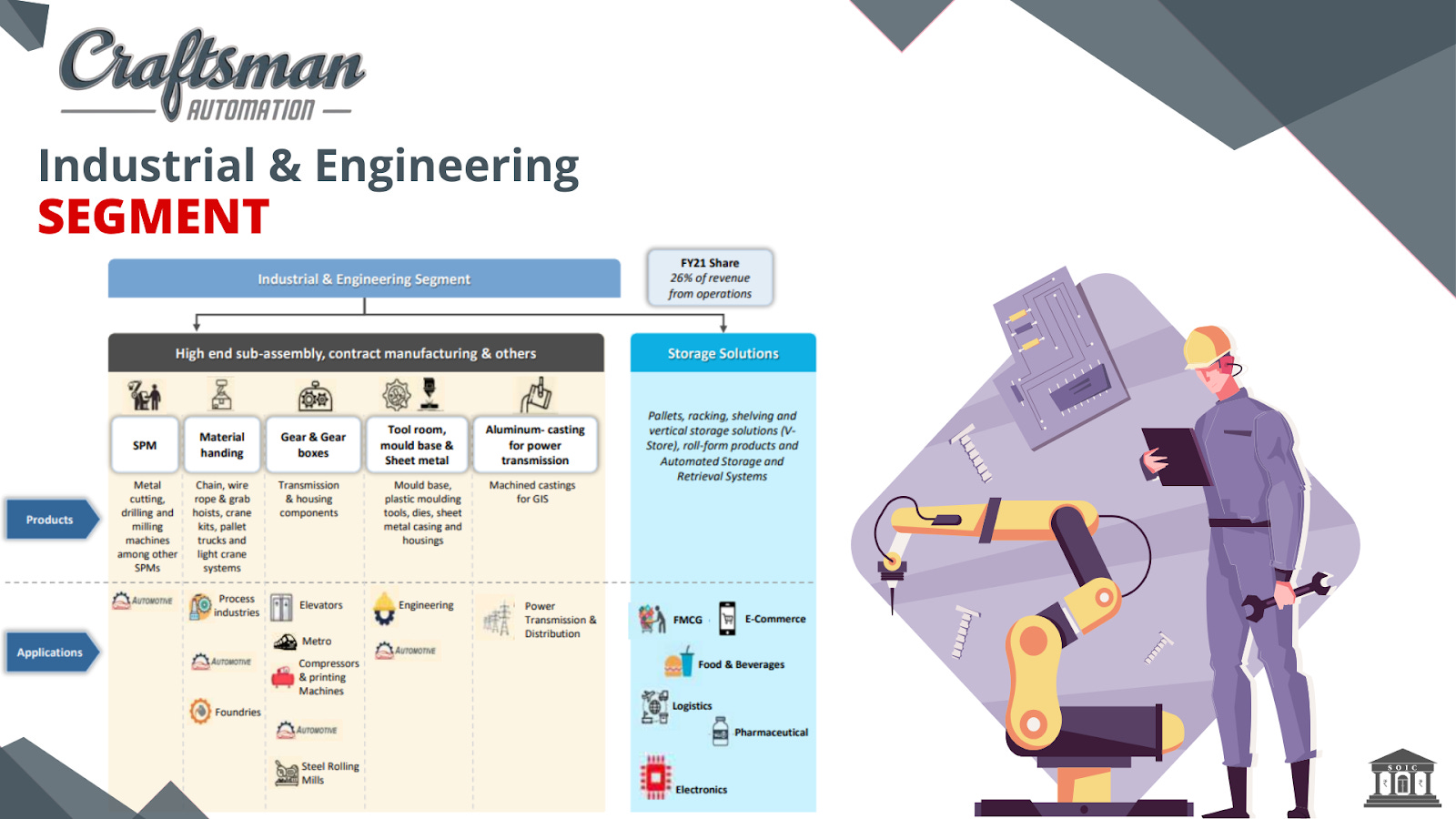

The next business segment is Industrial and Engineering

The Industrial and Engineering vertical is essentially a nonautomotive business vertical which caters to diverse user sectors – it prudently reduces the Company’s dependence on the automotive sector. The Company has divided it into two sub-segments, namely, 1) High-End Sub-Assembly, Contract Manufacturing & 2) Storage Solution.

High-end sub-assemblies and contract manufacturing products sub-segment includes multiples categories such as (1) aluminium products for power transmission, (2) gears and gear boxes, (3) material handling equipment, (4) tool room, mould base and sheet metal and (5) special purpose machines.

Here company manufacture aluminium products for power transmission, high-end precision products and undertake sub-assembly, material handling equipment such as hoists, crane kits and industrial gears, manufacture gear and gear boxes, marine engines and accessories, special purpose machines (“SPM”), which includes metal cutting and non-metal applications such as washing and leak testing solutions and tool room, mould base and sheet metal.

This segment involves a high level of design engineering and a complex production system which involves design and development, foundry and casting, sheet metal fabrication, precision machining and assembly, finishing, testing and others.

From this sub-segment company exports to various customers, including Mitsubishi Heavy Industries, Rhein Getriebe and other global customers.

Aluminium Products for Power Transmission

Growth drivers in the aluminium products for power transmission sub-segment include the use of Gas Insulated Switchgear (GIS) instead of air insulated switchgears (AIS), particularly in urban areas, as GIS is compact, occupies less space and has lower maintenance as compared to AIS. Demand for industrial castings from the power transmission sector is driven by investments of the central and state government transmission companies and, to a smaller extent, from the private sector for the medium-voltage segment.

Currently around 20-25% of the transmission substation switchgears are gas-insulated. The share of GIS switchgears is expected to rise further to ~30% by fiscal 2024.

Gear and gear boxes

Key products in the Gear and gear boxes sub-segment, include transmission and housing components. Their products in this segment cater to elevators, metro transportation, compressor manufacturers, printing machines, automobiles and steel rolling mills.

Growth drivers in the gear and gear boxes sub-segment include growth in steel products, material handling equipment, elevators and wind power capacity additions.

In this sub-segment, they undertake domestic sales as well as exports to various customers. Key customers include Ashok Leyland, Elgi Equipments, Voith Turbo, Pricol, Siemens and others.

Material handling

Company’s key products in the material handling sub-segment include chain hoists, wire rope hoists, grab hoists, crane kits, light crane systems and pallet trucks. These products are used by process industries, automotive sector and foundries.

Company have capabilities like design and development, foundry and casting, manufacture of gears, sheet metal fabrication and assembly, testing and others. They have also entered into a joint venture with Carl Stahl Hebetechnik GmbH for engaging in marketing, installation, commissioning and rendering after-sales services for its products in this sub-segment, manufactured by them. These products are sold through Carl Stahl Craftsman Enterprises Private Limited under the brand “Carl Stahl Craftsman”.

Tool room, mould base and sheet metal

The products in this sub-segment cater to diversified industries including engineering and automotive sector. Key products and services in the tool room, mould base and sheet metal sub-segment include mould base, plastic moulding tools, dies, sheet metal casing and housings.

The capabilities include design and development, heavy duty precision machining and assembly (including CNC machining, laser heat treatment, assembly, testing, etc.), sheet metal fabrication, welding, painting, finishing and others.

Special Purpose Machines (SPM)

Key products in the SPM sub-segment include metal cutting machines, drilling machines, milling machines and other SPMs like leak testing machines, nut runners, industrial washing machines and supply conveyors.

Machines in this sub-segment are primarily used by automobile companies. Growth drivers in the SPM sub-segment include the implementation of BS VI emission norms by the GoI, entry of new players in the utility vehicles, rise in sale of medium and heavy commercial vehicles due to improvement in industrial activity and the government’s focus on infrastructure.

The capabilities used in SPM sub-segment, include design and development of machines, vendor development of casting, bought-out components and electronic sub-assemblies, sheet metal fabrication, heavy duty and precision machining and assembly, testing and on-site installation.

The company undertakes direct domestic sales, and its key customers include Daimler India, Mahindra & Mahindra, Tata Motors, TAFE Motors and Tractors, Simpson & Co, JCB and others.

Storage Solutions

Storage solutions is a more recent sub-segment, which has ramped up rapidly over the last 2-3 years. The Company provides complete solutions for conventional/automated storage and manufactures products like pallets, racking, shelving, vertical storage solutions, automated storage solutions etc. for several sectors such as FMCG, e-commerce, logistics, auto, pharmaceutical and electronics.

The key storage products are stationary racks for warehouses, V-store, toll-form products and automated storage and retrieval systems.

In recent years, Craftsman forayed into the high margin storage solution with a slew of products that cater to the warehousing sector, in keeping with the huge demand for sophisticated warehousing solutions to cater growth in e-commerce in India. These products have been accepted and are gaining traction among the user sectors.

Storage solutions to drive segment growth:

Craftsman caters to warehousing and industrial sectors. Its products include, stationary racking for warehouses, V-store, roll-form products and automated storage and retrieval systems (ASRS).

Setting up of large regional warehouses by e-commerce, organised retailing, consumer durables, auto components and pharmaceuticals as well as cold storage industries, are key growth drivers for storage solutions going forward.

Key customers are Mitsubishi Heavy Industries, Rhein Getreibe and regional warehouses by e-commerce, organized retailers, FMCG companies, consumer durables, auto-component makers and cold storage.

The company expects the storage business to continue its growth trajectory and become an independent business segment over the next few years. Using their design and engineering capabilities, they have developed a vertical storage system with tray extractor arrangements operated by a console, marketed under the brand name “V-Store”. With increasing space constraints in urban areas, V-Store, which improves the storage ratio and has substantial applications across various industries, holds potential in the near future.

Key risks in the company:

High exposure to ICE engine components: The powertrain division accounts for 52% of revenues and includes exposure to several engine components like cylinder blocks, cylinder heads, etc. While the risk of imminent EV transition in the CV space (50% of segment revenues) is low, any eventual move away from ICE could impact revenue and profitability in future. There is also a terminal value risk in such a case since the future of the automobile industry is EV, if EV adoption in HCV picks up faster and company not able to develop suitable products for them then it could loose its market dominance.

Delay in underlying industry recovery: Majority of its business is directly related to vehicle sales and production by its customers, who consist primarily of large automotive OEMs, and demand for the products is largely dependent on the industrial output of the automotive industry. Slower-than expected revival in the industry could pose a downside risk for Craftsman. Whole thesis is built on the revival of the CV cycle, if it doesn’t plays out well then this can become a value trap.

Evolving technologies in the aluminium space: While the importance of aluminium in vehicular lightweighting is well established, evolution of means to achieve the same could undergo some changes in future (e.g., casting vs forging). In the event of other technologies gaining precedence over die casting, there could be a downside risk to the revenue and profitability estimates for the auto aluminium division.

Customer concentration: Company derives >58% revenue from top 10 customers. The loss of any of its major customer groups due to any adverse development or significant reduction in business from its major customer groups may adversely affect its business.

Delay in passing on the inflated raw material cost: The key raw material for the company are Steel & Aluminium whose price has been very volatile in the past. The company has been able to pass on the inflated costs to its customer on a timely basis but any delay in future could squeeze its margins.

Now coming to the financial performance of the company

Deleveraging plan to improve profitability:

As on 31st March 2022, company’s total debt stood at Rs 715 Cr against Rs 1040 Cr in FY 20. The company has done the IPO to repay its debt in FY2021. IPO proceeds of Rs 150 Cr were utilized for repayment of debt. Company is guiding to reduce its debt by 100 Cr in current FY. The reduction in interest outgo in the coming quarter can boost profitability and return ratios.

Growth kicking in all segments:

In the coming years growth will be driven by all the three segments of Craftsman. Strong CV cycle will drive the PowerTrain business. Even the Farm sector shall help the cause to some extent. In the Aluminum Products segment, new orders mainly from the PVs and in the storage sub-segment within the industrial segment shall lead to a very healthy topline growth. Also the rising contribution from the high margin storage business in the industrial segment shall ensure the rise in margins.

The company has given the guidance to grow at 20% in topline as well as absolute EBITDA in FY23.

Healthy operating margin profile:

Despite challenging business times due to overall economic slowdown, adoption of BS-VI, and macro economic factors, the company has maintained an EBITDA margin of 24% in FY22.

The company has given the guidance to sustain the EBITDA margins of 24% in the coming future. This is mainly due to its favourable product mix (high proportion of powertrain business) and strong in-house engineering & design capabilities.

Free Cash Flow to improve:

With a strong earnings profile, stable working capital, reducing debt, and minimum CAPEX for upcoming quarters, one can expect Operating Cash Flows and Free Cash Flow to improve in the coming quarters.

What do valuations look like?

At the time of writing the company is valued at 29 times Price to Earnings ratio and EV to EBITDA of 11 times. Management expects to grow top line at 20% in FY23 as well as for next few years and operating margins to sustain at 24% for the year. With the reduction in debt by 100 crore in current FY & net debt free in next few years could increase its PBT at much faster pace. Low capex number will leads to stagnant depreciation.

In base case scenario the valuations of the company looks like this:

The company is currently trading at 8x EV/EBITDA one year forward.

Do let us know in the comment section below, how you see the risk-reward playing out over here at current valuations and what you think about the revival in CV & Capex theme.

Disclosure: Nothing on this website should be construed as investment advice. Please consult your financial advisor. We are not SEBI registered Analysts/Advisors. We are not accountable for any loss or gains that might occur to you from this or any analysis on the website. The author and SOIC do not hold the stocks in their portfolio at the date this post was published.