Decoding Amkor Technology (AMKR)

The Silent Giant Powering the AI and Semiconductor Revolution

When we think of the semiconductor boom, the spotlight usually shines on the designers like NVIDIA or Apple, or the giant foundries like TSMC. However, there is a critical, often-overlooked industry making the AI and high-performance computing (HPC) revolution physically possible. We are talking about the OSAT (Outsourced Semiconductor Assembly and Test) industry.

In this blog we will dive deep into one of the players - Amkor Technology (Nasdaq: AMKR).

As the world’s largest U.S.-headquartered OSAT (Outsourced Semiconductor Assembly and Test) provider, Amkor is undergoing a massive transformation. It’s no longer just a backend packaging service; it’s a strategic co-development partner bridging the gap between cutting-edge silicon and next-generation electronics.

1. Understanding the Business: What Does Amkor Do?

At its core, Amkor provides semiconductor packaging and test services. Once a semiconductor wafer is fabricated (e.g., printed with microscopic circuits), it cannot be plugged directly into a phone or server. It needs to be cut, protected, connected electrically to a circuit board, and rigorously tested. This is Amkor’s domain.

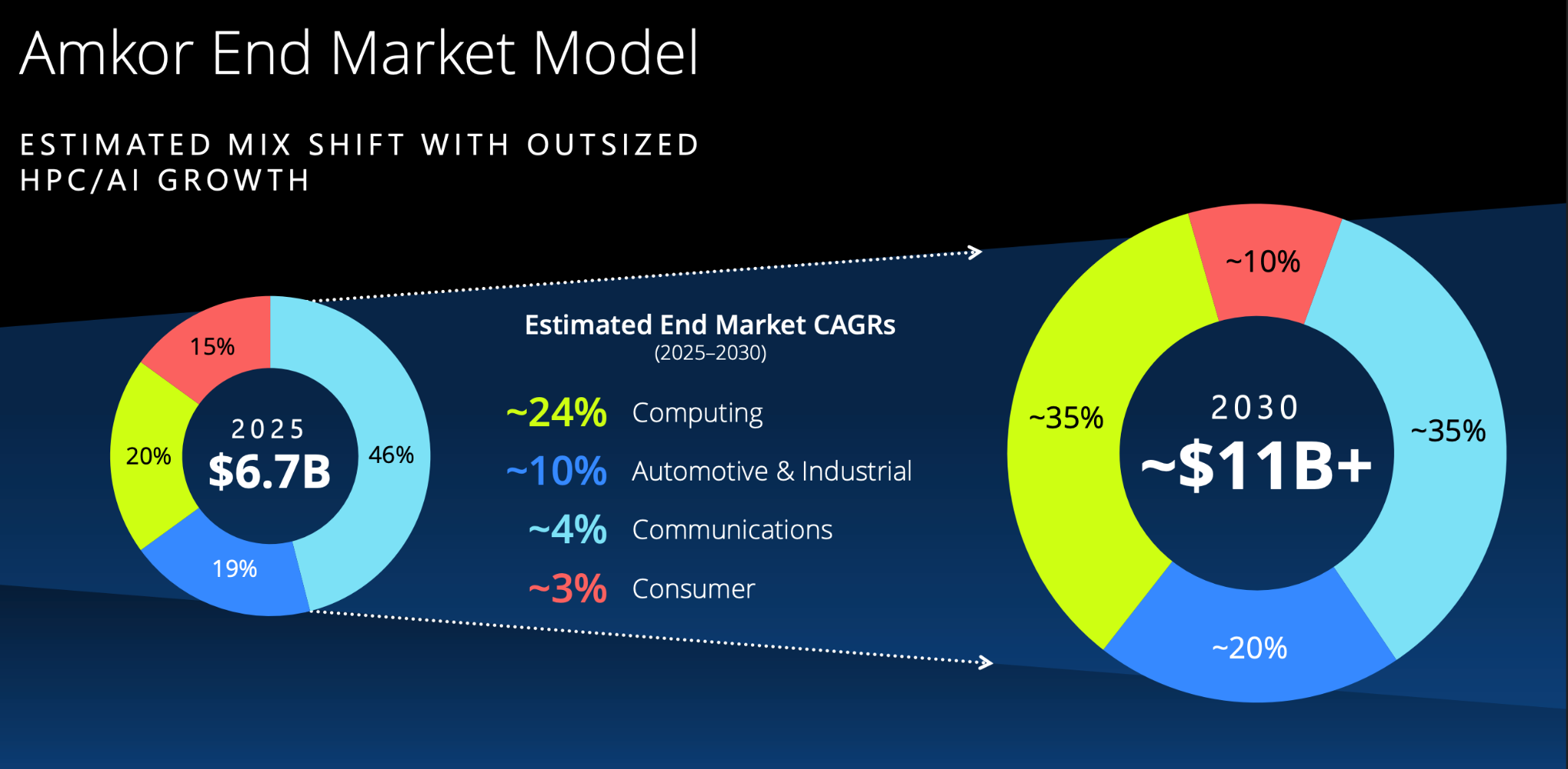

Amkor operates a massive global footprint of 13 million square feet spanning 9 countries (including South Korea, Taiwan, Vietnam, Portugal, and soon the U.S.). They cater to diverse end markets:

Communications (44% of Q1 2026 Sales): Smartphones and tablets (iOS and Android premium tiers).

Computing (21%): Data centers, AI accelerators, infrastructure, and storage.

Automotive & Industrial (21%): ADAS (Advanced Driver Assistance Systems), electrification, and infotainment.

Consumer (14%): Wearables, IoT devices, and AR/VR.

The Paradigm Shift: Historically, packaging was considered a low-margin, commoditized backend process. But as “Moore’s Law” slows down (making it harder to shrink transistors on a single monolithic chip), the industry is shifting to Advanced Packaging. Instead of making one giant, expensive chip, designers are breaking them into smaller “chiplets” and stitching them together in a high-density package (2.5D, High-Density Fan-Out). Advanced packaging is now Amkor’s primary growth engine.

2. The Value Chain: Where Amkor Fits In

The semiconductor value chain looks broadly like this:

Fabless Designers (NVIDIA, AMD, Apple): Design the chips.

Foundries (TSMC, Samsung): Manufacture the silicon wafers.

OSATs (Amkor, ASE): Package, assemble, and test the chips.

System Integrators/OEMs: Build the final product (servers, cars, phones).

Amkor is the critical bridge between the foundry and the final customer.

Because advanced packaging (like integrating High Bandwidth Memory or HBM with GPUs) directly dictates the power, thermal control, and speed of AI chips, Amkor’s position in the value chain has elevated dramatically. They are no longer brought in at the end of the line. Instead, Amkor is engaged years in advance to co-develop the package architecture with fabless designers and foundries, reducing system-level risk and ensuring supply security.

3. The Competitive Landscape

The OSAT market is highly consolidated at the top, but fiercely competitive. Amkor’s primary rivals include:

ASE Technology Holding (ASE): The undisputed global leader in OSAT by market share. ASE has massive scale and advanced packaging capabilities, often competing head-to-head with Amkor for premium contracts (like Apple).

Internal Foundry Packaging (TSMC, Intel, Samsung): The most significant emerging threat in advanced packaging comes from the foundries themselves. TSMC’s CoWoS (Chip-on-Wafer-on-Substrate) and InFO (Integrated Fan-Out) technologies are the gold standard for high-end AI chips (like NVIDIA GPUs). Foundries are increasingly capturing the highest-margin advanced packaging work, pushing OSATs to either partner closely with them (as Amkor is doing with TSMC in Arizona) or compete on price and scale for slightly less bleeding-edge designs.

JCET Group: A major Chinese OSAT player. They benefit from strong domestic support and are expanding their footprint, though geopolitical tensions limit their reach into Western supply chains for critical AI/HPC infrastructure.

Amkor’s moat against these competitors is its strong U.S. presence, its willingness to co-invest aggressively in local supply chains (Arizona), and its long-standing, 30+ year partnerships with top-tier fabless designers.

4. The Investment Thesis: Why Amkor?

Amkor is currently riding three structural tailwinds that make it a compelling story of multi-year value creation:

A. The AI & HPC Megatrend:

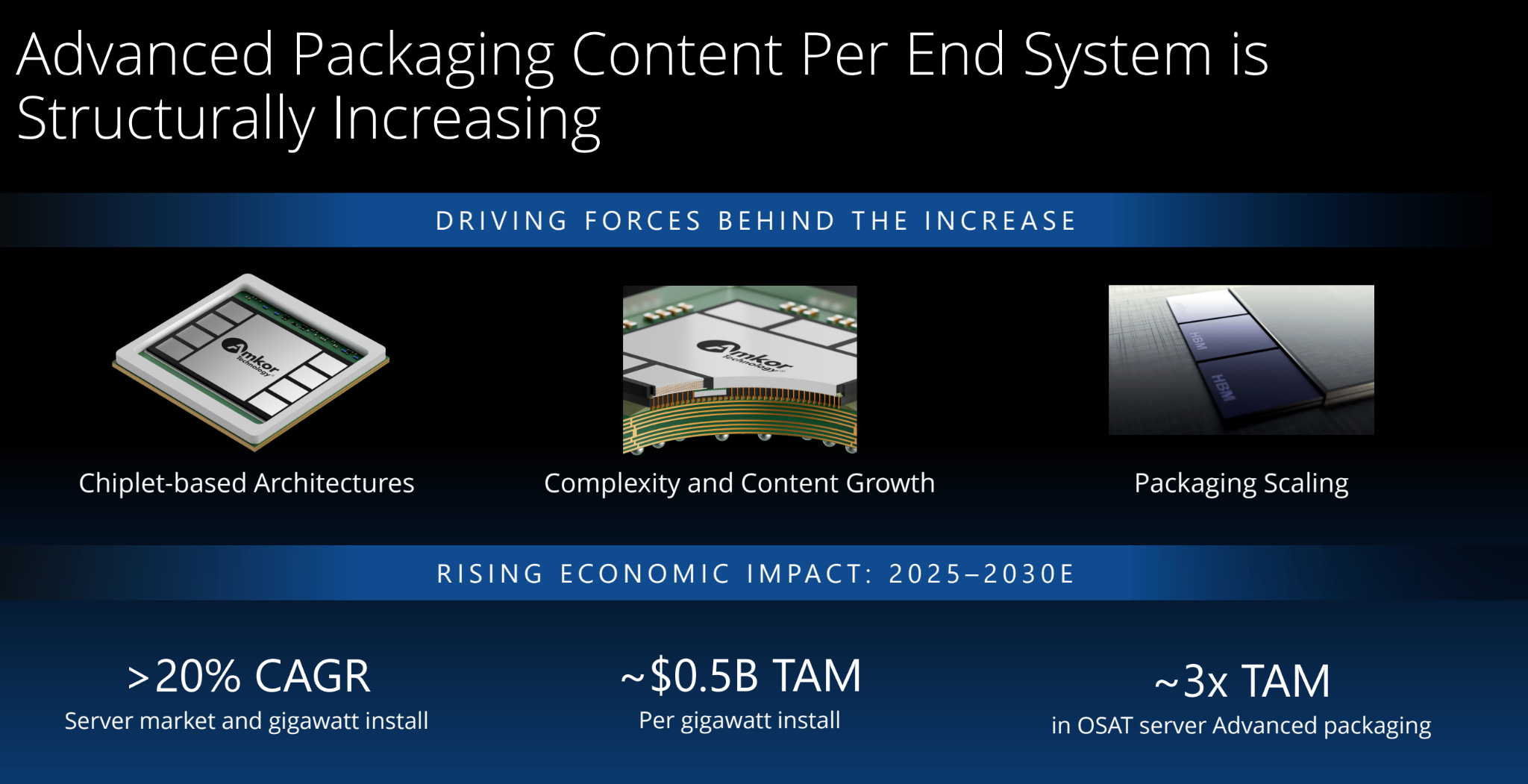

The proliferation of AI requires massive compute power. The server TAM is expanding rapidly, and advanced packaging content per server is expected to roughly triple. Amkor is uniquely positioned to capture this growth with its highly scalable 2.5D and HDFO platforms.

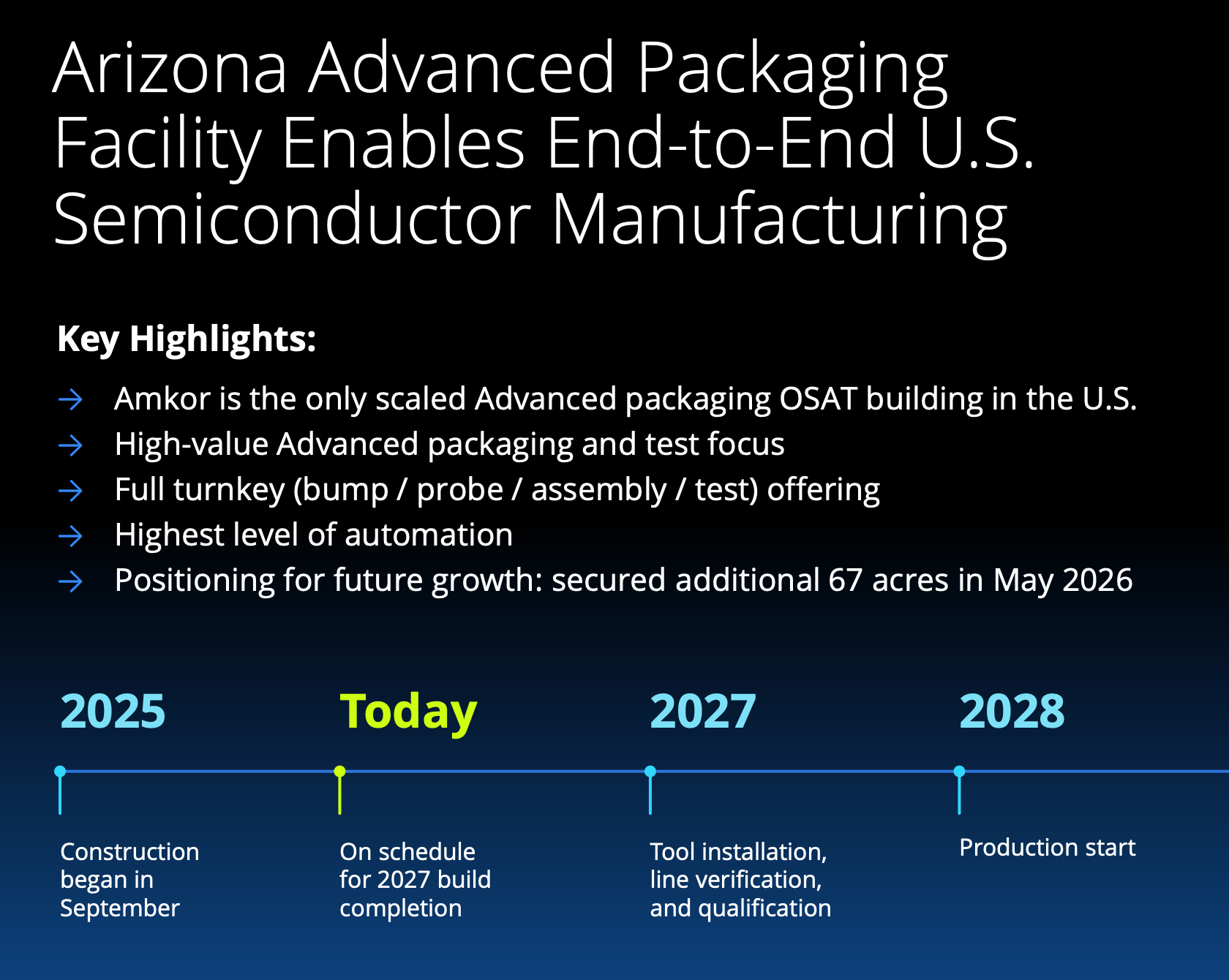

B. Reshoring and the U.S. Supply Chain:

Driven by geopolitics and national security, supply chains are shifting from global to regional. Amkor is building a massive, highly automated Advanced Packaging facility in Arizona. This $7B (across two phases) mega-project is a game-changer. Co-located near TSMC and partnered with Apple, Amkor will be the only scaled advanced packaging OSAT building in the U.S., providing the missing link for a true end-to-end American semiconductor supply chain.

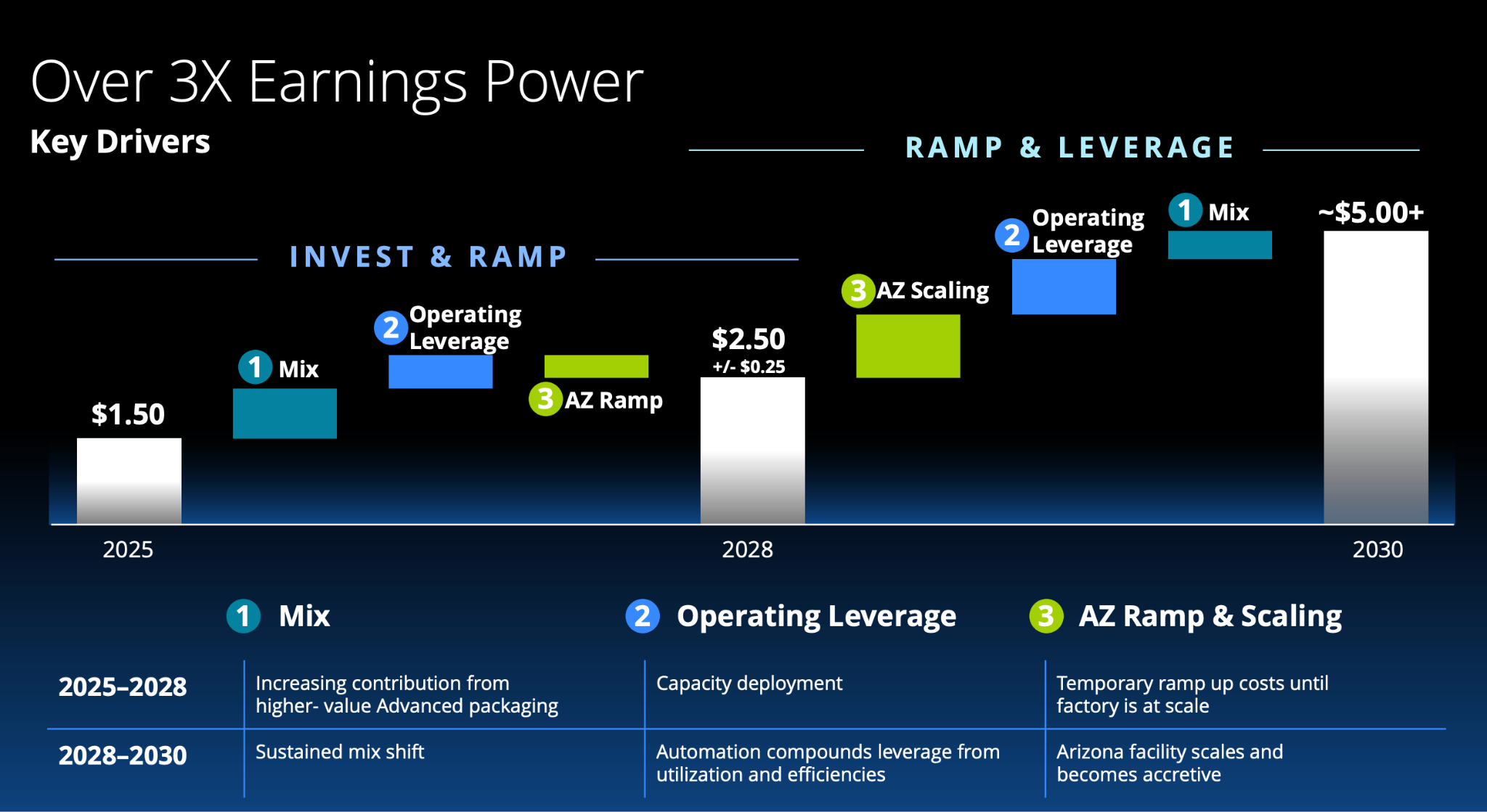

C. Path to Tripling Earnings Power by 2030:

Because Amkor is engaging earlier in design cycles with multi-year commitments, they have unprecedented visibility. This allows for disciplined capacity planning, higher utilization, and a shift toward a higher-margin product mix. Management expects these dynamics to translate into more than 3x earnings power by 2030.

5. Key Risks to the Thesis

While the tailwinds are strong, Amkor operates in a notoriously difficult industry:

Extreme Cyclicality & High Fixed Costs: The semiconductor industry is deeply cyclical. If end-market demand slumps, their fixed costs remain high, which can violently crush gross margins and profitability.

Execution of the Arizona Facility: The Arizona build-out is Amkor’s most ambitious project to date. Phase 1 requires enormous upfront capital. While supported by government incentives (CHIPS act, tax credits), any construction delays, cost overruns, or slower-than-expected utilization ramps in 2027/2028 will drag down margins.

Customer Concentration: Amkor’s top 10 customers accounted for a staggering 68% of net sales in Q1 2026. The loss of a key customer (like Apple) or a severe downturn in the premium smartphone or automotive markets would severely impact revenue.

Geopolitical Vulnerability: Despite the Arizona expansion, the vast majority of Amkor’s operations remain in Asia. They are highly exposed to regional conflicts, trade barriers, export controls, and tariffs.

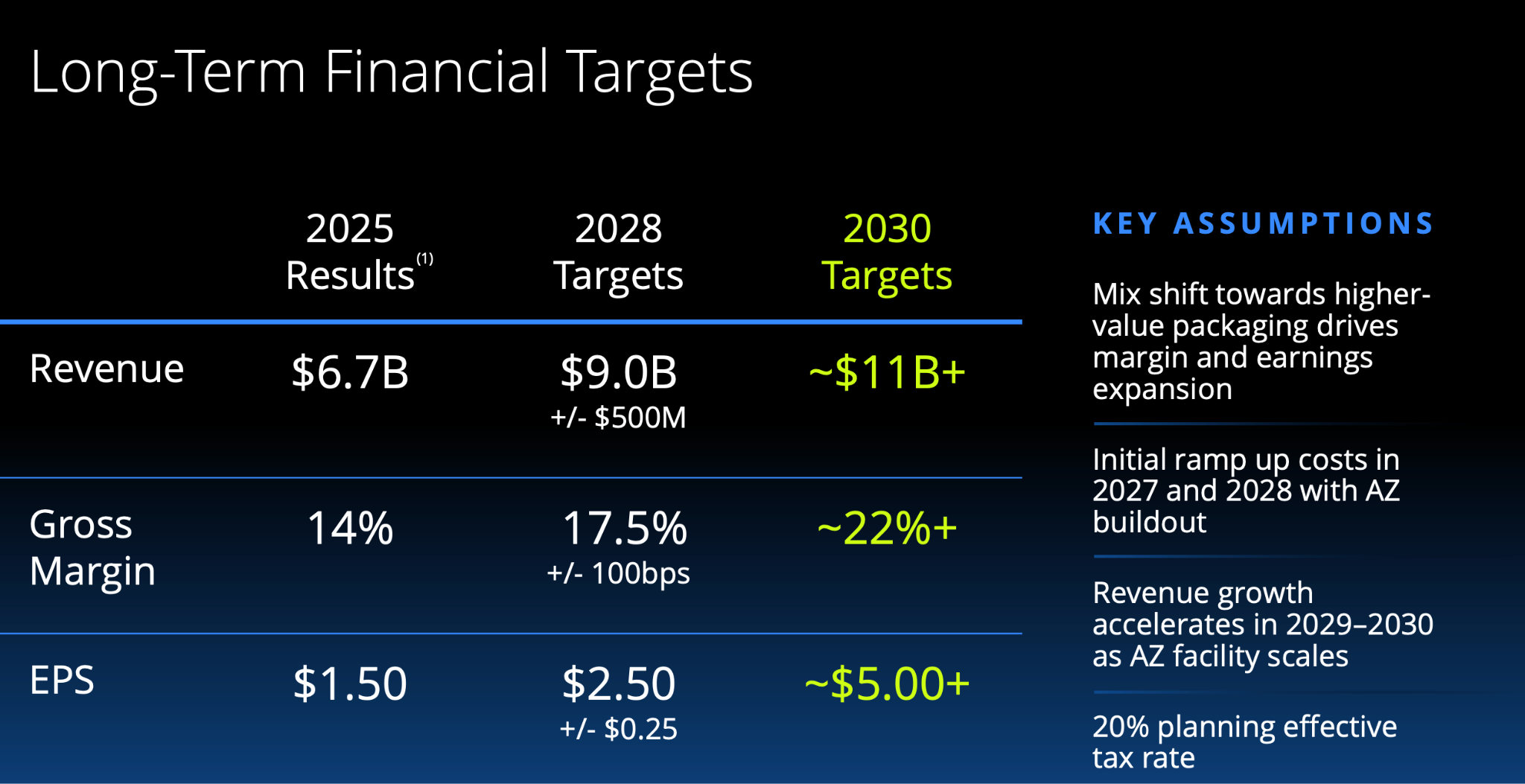

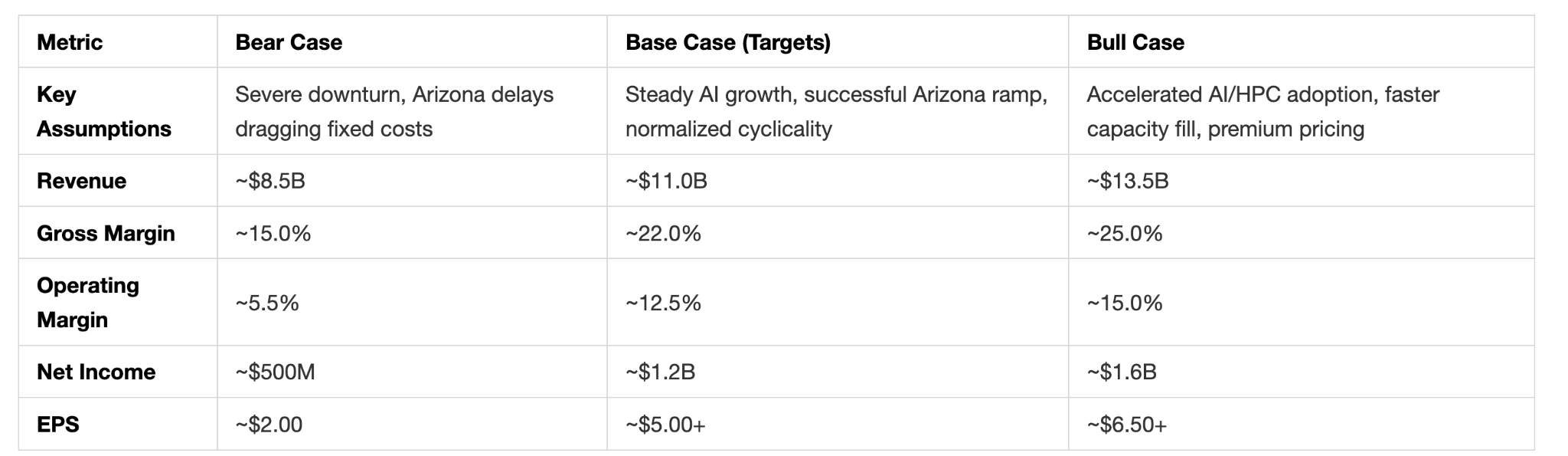

5. Valuations

Amkor had an investor day and they have guided for $11B+ in revenue and $5+ EPS by FY30.

Based on this, it is possible that today we are buying Amkor at 12-15x FY30 P/E. This multiple continues to assume that OSAT companies are low margin businesses. For decades, computing performance came directly from transistor scaling (classic Moore’s Law). However, as transistor miniaturization is now hitting both physical and economic limits, the biggest performance gains for AI and High-Performance Computing (HPC) are coming from package system architecture. Because of the slowdown in Moore’s Law, the industry is moving toward heterogeneous integration, taking multiple smaller pieces of silicon (”chiplets”) and integrating them into one single, high-density package.

We at SOIC actively manage a watchlist of ideas for not only Indian businesses but also 15-20 Global businesses.

Our TVGP Watchlist is a curated universe of roughly 50 businesses that we track continuously using our internal framework: Theme, Value, Growth, and Promoters. Many of the ugly ROCE, unique capability businesses you just read about sit inside this watchlist identified early, tracked deeply, and studied over time rather than chased after the stock has already moved.

Here we have a combination of both Global and Indian Watchlist of stocks which one can do deep dive with us on each of the names present there.

If studying businesses this way resonates with you then the broader watchlist and research library is here: 👉 Explore SOIC Long Term Research

Can you guys tell if this tech infrastructure can be brought in India ,is it feasible to open a startup around this, I am a 23 year old looking for business ideas. I thought if India can even provide for some part of the value chain for the chips,it can be a game changer. But I wanna know is it feasible?