From Struggling Small Cap to Dominant Industry Player

From Struggling Small Cap to Dominant Industry Player: The Remarkable Turnaround of Apcotex Industries

Business Background

Apcotex was established in 1980 as a division of Asian Paints (India) Limited. In 1991, the division was spun off as a separate company, headed by Mr. Atul Choksey, the former Managing Director of Asian Paints Limited. Mr. Choksey has more than four decades’ of experience in the paints and chemicals industry.

The current Managing Director of the company, Mr. Abhiraj Choksey, and other management personnel who are experts in the field of chemicals, bring valuable experience to the company. The company enjoys a strong market presence in the Indian synthetic rubber and synthetic latex markets and has a significant market share in India.

The overall clientele has remained diversified, with the top 10 customers contributing ~30-35% of the revenues in the last two years. The products find application in various industries such as paper and paperboards, gloves, textiles, carpets, construction, tyre cord, footwear, and automobiles. Additionally, the business has established trusting connections with respected players in these sectors.

Company Profile

Apcotex Industries Limited is one of the leading producers of Synthetic Rubber (NBR & HSR) and Synthetic Latex (Nitrile, VP latex, XSB & Acrylic latex) in India. The company is one of the leading producers of emulsion polymer products in India, Synthetic Latexes (various grades of Carboxylated Styrene Butadiene Latex, Styrene Acrylic Latex, Vinyl Pyridine Latex and Nitrile Latex) and Synthetic Rubber (Nitrile Butadiene Rubber, Nitrile Polyblends, NBR Powder and High Styrene Rubber). Company has one of the broadest ranges of emulsion polymer products in India and caters to a wide range of industries.

The company has a diversified clientele and is present across various industries, which protects it from any slowdown in a single industry. The major raw materials are petrochemical products, and its business is vulnerable to high volatility in the prices of crude oil as well as its downstream products. Apcotex has a strong global presence in Southeast Asia, the Middle East, & Africa and intends to tap other Markets.

A game-changing OMNOVA acquisition...

Apcotex acquired 100% stake of Omnova Solutions Pvt Ltd (OSIPL) for ~Rs 360 mn on 5th Feb. 2016. The acquisition was funded entirely through internal accruals. By purchasing OMNOVA Solutions, a company gained control of the synthetic rubber market and gained access to advanced manufacturing techniques for nitrile latex. Because of Apcotex's expertise with butadiene and styrene as well as its method of emulsifying oil with water, competitors face a high barrier to entry.

Apcotex was able to enter four new industries thanks to the acquisition: - Automotive, LPG Tubing, and Wire & Cables. This acquisition closely reflects Apcotex's long-term plan to fully exploit the emulsion polymer market. The only manufacturer of NRB in India is OMNOVA, which is also the nation's second-largest manufacturer of High Styrene Rubber (HSR) after Apcotex.

A service-driven approach and a leading market share across end-user industrial segments are the reasons for the significant client stickiness. Emulsion polymer has a wide variety of uses, and its dominance in the Nitrile Rubber market suggests that it will be widely used in the medium to long term.

Apcotex has managed to turn its fortunes around and become a dominant player in the Industry!

Let’s see how they did –

Focusing on innovation and product development: Apcotex realized early on that innovation was key to staying competitive in the market. The company invested heavily in research and development and developed new products that met the changing needs of the market.

Improving operational efficiency: Apcotex also focused on improving its operational efficiency to reduce costs and improve profitability. The company implemented lean manufacturing processes and invested in automation technologies to streamline its operations.

Expanding into new markets: Apcotex recognized that there was significant growth potential in new markets, both domestic and international. The company expanded its sales and distribution network and started exporting its products to new countries.

Acquiring complementary businesses: Apcotex also made strategic acquisitions of companies that complemented its existing product portfolio. These acquisitions allowed the company to expand its product offerings and enter new markets.

Building a solid brand: Apcotex put a lot of effort into creating a solid brand that stood for dependability and quality. In order to increase awareness of its goods and services, the company made investments in marketing and branding campaigns.

Business Picture

Strong management teams, a wealth of industry knowledge, long-standing client relationships, and investments in R&D are just a few of the key advantages that Apcotex has over its rivals and new competitors.

The company anticipates keeping its key operational metric of EBITDA/ton steady, with toplines beginning to increase gradually in Q3/Q4 of the current fiscal year as new capacities are put into service. Additionally, the company's growth is anticipated to be fueled by ongoing and upcoming new capacity additions, rising export demand for NBR-related products (such as nitrile and xnbr latex), and improving domestic demand in supporting industries like paper, carpets, and construction.

Debottlenecking, new products, significant capacity additions, rapid growth in the ApcoBuild business, and increased export revenue will all benefit Apcotex. In the following two to three years, the management expects exports to contribute 30 to 35% of the topline (up from 21 percent in FY22).

The company is supported by the new business sector ApcoBuild and products introduced in the previous two years, which are anticipated to fuel growth in the following two years. Over the next two years, the company expects significant double-digit revenue growth. Factoring in the strong performance despite demand destruction caused by COVID- 19, expect healthy volume and price growth in the upcoming quarters.

The evolution of the financial situation

Revenue: Over the past few years, Apcotex's revenue has consistently increased. The company reported revenue of INR 1,080 crore as of March 2023, a significant increase from the INR 388 crore reported as of March 2017.

Net Profit: Over the past few years, Apcotex's net profit has also significantly increased. The company reported a net profit of INR 108 crore as of March 2023, up from INR 35 as of March 2017.

Earnings per share (EPS): Over the past few years, Apcotex has consistently improved its EPS. A significant increase from the company's reported EPS of INR 6.74 as of March 2017 to INR 20.82 as of March 2023.

Return on equity (ROE): Over the past few years, Apcotex's ROE has also significantly improved. In comparison to the ROE of 9.3% reported for the fiscal year 2017–18, the company reported a ROE of 24.8% as of March 2023.

Overall, Apcotex Industries' financial performance has shown significant improvement over the past few years, as the company has successfully executed its growth strategy and expanded its business.

CAPEX to take advantage of the opportunity

With a brownfield expansion plant for nitrile latex at its Taloja facility, which is anticipated to be fully operational by H1FY24, Apcotex is aiming to double Synthetic Latex capacity from 65,000 MT to 1,30,000 MT by FY24. With capacities of 35,000 metric tonnes per year for the Multipurpose Latex Plant in Taloja and 50,000 metric tonnes per year for the Nitrile Latex Plant in Valia, both projects in Taloja and Valia were put into operation during the third quarter.

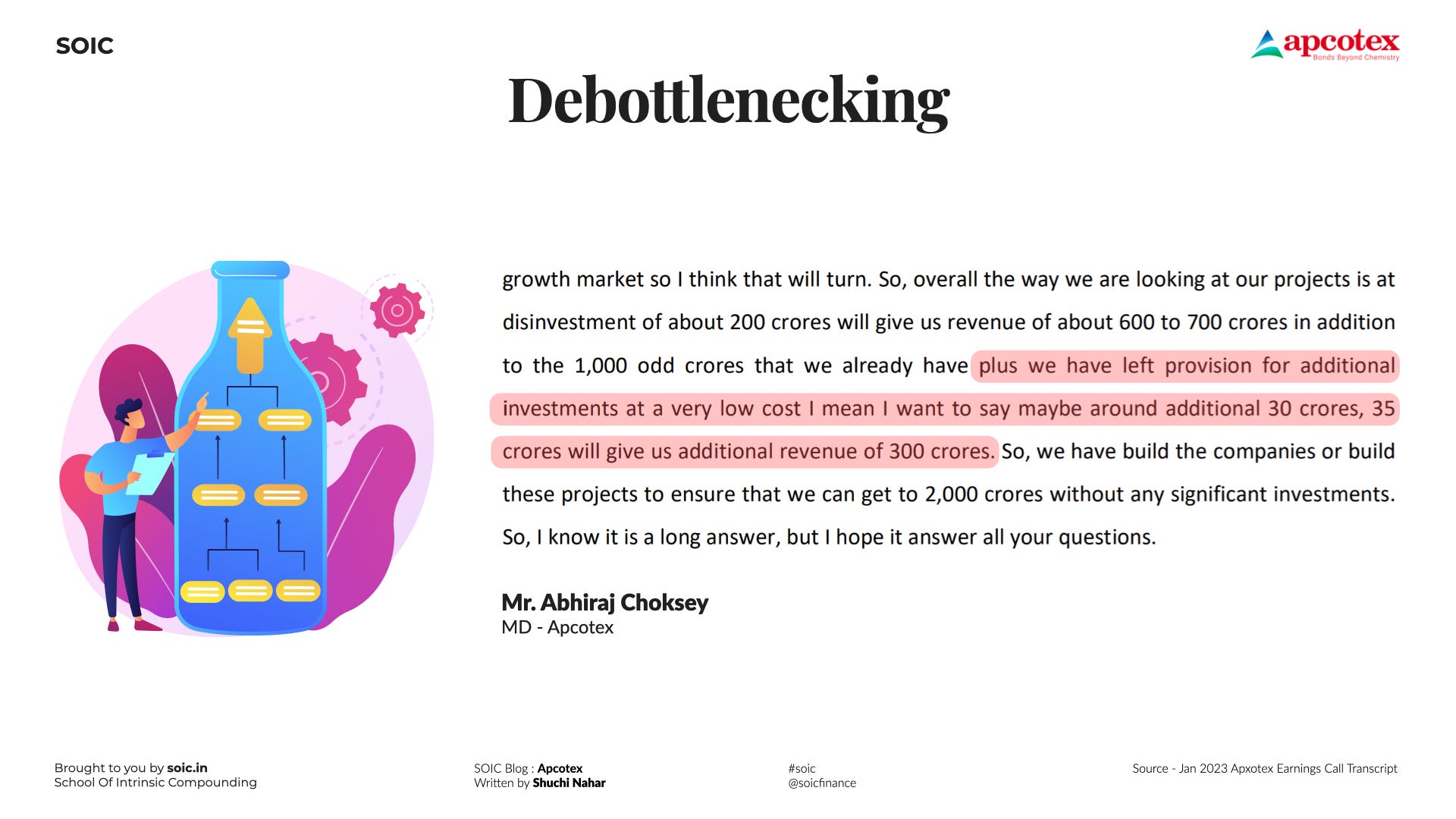

The company also intends to expand Nitrile Rubber production to serve both the domestic and international markets. When both plants are operating at full capacity, which is anticipated to be by Q3 FY23, all the expansion plans, including that one, are expected to generate an additional Rs. 600–700 crore in revenue.

The management is confident that by H2FY24 or H1FY25, its new capacities will be fully ramped up. Additionally, Apcotex is preparing for NDR Capex, for which it has received environmental approval. In the following two quarters, a decision will be made regarding this project.

Industry Overview

Asia Pacific leads the production of the global synthetic rubber industry, with the automobile sector-leading growth. With the rise in population, the large manufacturing base of the automobile industry, and the availability of competitive labour, India offers great opportunities for synthetic rubber product manufacturers. With increasing R&D investments backed by strong infrastructure, the country is poised to become a leader in rubber products manufacturing in the years ahead.

About 70% of Nitrile Butadiene Rubber (NBR) is imported in India, which creates good potential for Indian manufacturers of Nitrile Rubber. The long-term growth of this segment can be attributed to the growing demand for NBR across automotive, industrial, and agricultural applications.

Today, the company has developed a strong Research & Development base, which has enabled them to develop, manufacture, and export products and compete effectively against global players. Apcotex Industries has a workforce strength of over 550 full-time employees.

On the Nitrile Latex & Glove Industry front

The glove industry is facing the twin problems of low demand and high inventory levels, which have led to very low demand for synthetic latex, This situation is expected to continue over the next 6-9 months, which will keep the Nitrile latex margins below historical levels in the near term, bringing a drag on overall margins.

Nitrile Latex Prices -

In 2020, the global demand for nitrile gloves surged due to the COVID-19 pandemic, causing a significant increase in the price of nitrile latex.

The price of nitrile latex rose from USD 900/MT in January 2020 to USD 4,500/MT in August 2020.

This increase in price was due to supply chain disruptions, raw material shortages, and increased demand from the healthcare and industrial sectors. Due to that, nitrile latex margins have reduced to 4-5% but over the longer period, as nitrile latex margins recover, they see their EBITDA margins improving to around 18%.

Nitrile latex is a key raw material for Apcotex Industries Limited, and the cost of nitrile latex has been volatile in recent years due to more capacities in existence due to COVID from China and Malaysia. As of now, the demand for medicinal gloves has reduced, and they have a shelf-life of 2-3 years. So lower-end manufacturers will go out of business as there is a huge supply and demand have substantially come down.

Nitrile latex margins continue to be extremely weak, mainly in the glove market. There were a lot of extra gloves produced during COVID times, and then post COVID over the last year, glove demand has been extremely muted down by 20%, 30% compared to the previous 2 years, and 3 years, and so margins for the nitrile latex for gloves are even lower than pre COVID levels, so that has been a challenge for the company.

The management notes that the price of nitrile latex has started to stabilize after the sharp increases seen in 2020, but it remains a key factor that can impact the company's margins.

The management also notes that other raw materials, such as butadiene and styrene, have also experienced price volatility in recent years, which can impact the cost of producing nitrile latex.

The global Giant Latex Player – Synthomer

Synthomer’s comments on the global outlook – “Our year-to-date trading performance reflects the continuation of the challenging macroeconomic conditions in the final quarter of 2022, with subdued levels of demand across most of our end markets and geographies. We expect to make progress in the second half of 2023 reflecting the benefits of our operational and cost actions, supplemented by the anticipated start of an improvement in market conditions, although visibility of this is currently limited. As previously indicated, while underlying end-market demand for medical gloves remains robust, we do not expect the unprecedented period of destocking, and hence low NBR production levels, to abate before the end of 2023. We have taken decisive actions to strengthen our business in the current difficult environment and position ourselves for profitable growth as demand recovers.

We remain confident in our ability to execute Synthomer's refreshed strategy and deliver the medium-term targets we set out in October 2022, which were mid-single-digit growth in constant currency over the cycle, EBITDA margins above 15%, and mid-teens return on invested capital.”

Additionally, their CEO Commented - “Following an exceptional prior year and a robust first half, our overall performance in 2022 was significantly affected by deteriorating macroeconomic conditions during the second half and the prolonged destocking in nitrile latex. The group has been swift to respond.

We are on track to save £150-200m of cash by the end of this year, have rapidly executed the first successful divestment from our non-core business portfolio, and have completed a refinancing with our banks, strengthening the Group’s financial platform. We are implementing operational changes to strengthen delivery in our adhesives business while executing our new strategy, which will increase our focus on the more specialty, higher growth end markets in our portfolio.”

Glove Industry Cycle -

The glove industry is cyclical in nature and is driven by supply and demand factors.

In the past, the glove industry has experienced periods of oversupply, leading to lower prices and profitability, followed by periods of undersupply, leading to higher prices and profitability.

The COVID-19 pandemic has caused a significant increase in demand for gloves, which has led to more supply from China and Malaysia, particularly nitrile gloves, which has led to shortages and price increases.

However, the industry is expected to eventually return to a period of oversupply once the demand for gloves decreases and new capacity comes online.

It is important for glove manufacturers to manage their production capacity and costs effectively to remain profitable throughout the industry cycle.

However, the management of Apcotex Industries Limited expects that the demand for gloves may start to taper off soon as more people get vaccinated, and the pandemic is brought under control.

The management also notes that the supply of gloves has increased in recent months as new capacity has come online.

Despite this, the management believes that the glove industry remains attractive due to the ongoing demand and potential for long-term growth, particularly in developing markets.

Unit-level economics of the Capex

The level of automation that the company has been able to pull through and so just to give an example –

In Taloja plant 35,000 tons, which will give them at least 200 crores to 250 crores of revenue. For that, they need an additional 6 to 8 people per shift. Here, the OPEX is very low in comparison to other chemical players.

So, it is highly automated; everything is run from an automated DCF system, and of course, some amounts require physical manpower for packing and such, but a lot of it is automated much more than our current plant.

Although the chemical industry is regarded as a single sector, there are numerous subsectors within the chemical sector, making it impossible to compare one to the other.

Commoditized chemicals may have poor margins and high CAPEX, but they still provide the required return on capital due to their stable businesses. On the other end, however, there are particularly specialized chemicals, which may have high margins but limited volumes and business opportunities. The company’s line of work falls into that category—at least not yet—where you might look at other businesses worldwide that are similar to Apcotex and find companies with EBITDA margins of 30 to 35%.

Typically, chemical companies are considered to be very heavy asset industries with lower asset turnover; here, it is the complete opposite. The company is quoting that with the current 200 crore investment, they would generate about 600 to 700 crores of revenue, which is 3.5x.

The company expects higher depreciation and interest expenses in the coming quarters, although operational expenses will not increase much because of the nature of the design of new plants and less need for manpower.

Conference Call – Q3FY23

Through debottlenecking also company additional 30 crores - 35 crores will give company additional revenue of 300 crores.

Management also commented, - The only latex was nitrile latex for gloves, which is a new product in which we have invested 50,000 tons. So, as a result of that, we have obviously pivoted and converted our Taloja plant into a multipurpose latex plant that includes styrene-butadiene latex, styrene acrylic, and so on. So, we did that, and it should take maybe a couple of years for us to fill that capacity of 35,000 tons, which is in addition to our current 65,000 tons which is almost more than a 50% capacity increase. The other is in Valia, which is a $ 50,000-ton nitrile latex plant that is definitely a challenging market in the current context, but in the long term we are quite bullish on it and we think that the margins will turn.

So overall, we can say that the company has a strong unit level of business, which is very good. Though the company must face challenges in the short run due to Nitrile Latex prices, even the company is confident for the bigger play.

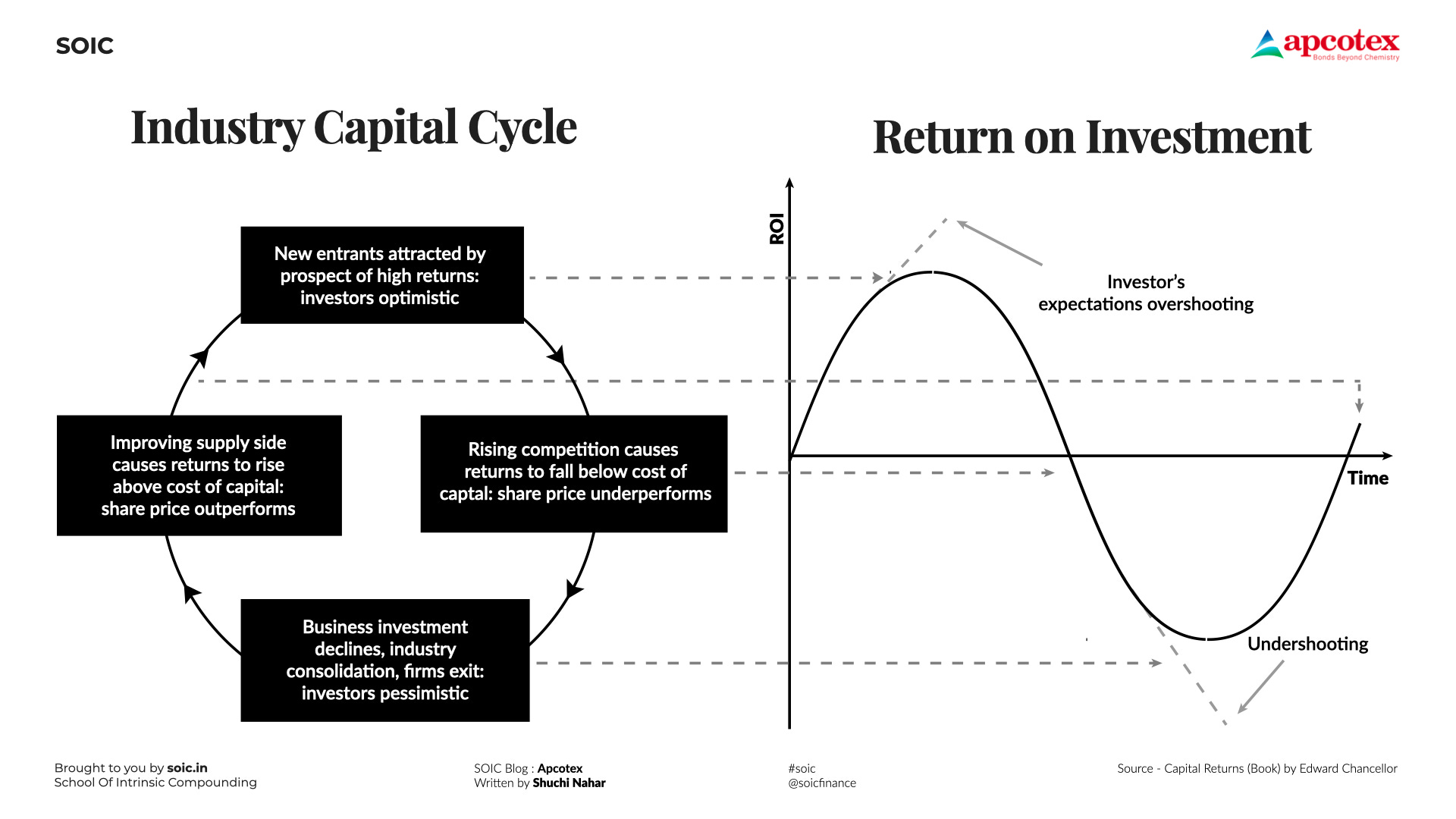

Here’s a mental model that suits this industry at this point in time that is – Mean Reversion

Capital cycle analysis, however, focuses on supply rather than demand. Supply prospects are far less uncertain than demand, and thus easier to forecast. In fact, increases in an industry’s aggregate supply are often well-flagged and come with varying lags – depending on the industry in question – after changes in the industry’s aggregate capital spending.

The “asset-growth anomaly” can be viewed from the perspective of mean reversion. Mean reversion is not driven by the ebb and flow of animal spirits alone. Rather, it works through differential rates of investment. Companies that earn above their cost of capital tend to invest more, thereby driving down their future returns, while companies that fail to earn above their cost of capital behave in the opposite way. This point is recognized by Benjamin Graham and David Dodd in Security Analysis (1934), the bible of value investing.

When it comes to the glove industry, increases in aggregate supply are often well-flagged and come with varying lags after changes in aggregate capital spending. For example, as we observed in the industry, when there was an increase in demand for gloves due to a covid, companies in the industry responded by increasing their capital spending to expand production capacity. This increase in capital spending eventually led to an increase in the aggregate supply of gloves in the market.

The capital cycle turns down as excess capacity becomes apparent and past demand forecasts are shown to have been overly optimistic. As profits collapse, management teams are changed, capital expenditure is slashed, and the industry starts to consolidate. The reduction in investment and contraction in industry supply paves the way for a recovery of profits.

For an investor who understands the capital cycle, this is the moment when a beaten-down stock becomes potentially interesting. However, brokerage analysts and many investors operating with short time horizons generally fail to spot the turn in the cycle but obsess instead about near-term uncertainty.

We can see the exact cycle happening in the latex industry - Due to which there was a rise in competition as many players from China and Malaysia, there was an oversupply of gloves eventually, which led to the removal of underperformers in the industry, which improved the supply, and the same cycle continues.

The rubber glove industry is currently in a phase of excess capacity, which has led to declining profits for companies in the industry. However, the industry is reaching a bottoming point in the capital cycle, and companies will begin to see increased profitability as excess capacity is absorbed and demand for rubber gloves continues to grow.

Disclaimer: The information provided in this reference is for educational purposes only and should not be considered as investment advice or recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are not registered with SEBI (Securities and Exchange Board of India) and do not provide any buy/sell/hold investment advice, suggestions, or recommendations, nor do we provide any Portfolio Management Services.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not be borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.