Gravita - Management meet notes

Copper is the next phase of growth

We recently met the management of Gravita India and here are the key insights from that call on how the future growth would look like for the company

1. RMIL Acquisition - Operational Update (First Full Quarter of Ownership)

Background & Context

Acquired 12 March 2026. This was effectively the first full quarter under Gravita’s ownership.

The previous owner, Mr. Benani, is 74 years old and was in “exit mode” — he was not pushing the business. Capacity utilization was well under potential.

FY26 RMIL sales volume was only ~10,000–11,000 tons (against 31,200 MTPA capacity = ~32-35% utilization).

FY27 Targets

Targeting ~18,000 tons in FY27 - a ~50% ramp-up over FY26.

Gradual further ramp-up planned over the next 2-3 years.

Planning to double RMIL’s own capacity from 30,000 to 60,000 MTPA at the existing Sarigam, Gujarat facility.

Business Model - Key Distinction from Gravita’s Core

RMIL is a converter, NOT a recycler. It buys cathodes from the market (primary raw material) and converts them into value-added products.

Also uses small portions of millberry and copper closs (high-grade scrap).

Gravita’s plan: replace cathode procurement with in-house recycled copper (backward integration). Once the Mandvi recycling plant is live, cathode will be produced in-house from scrap.

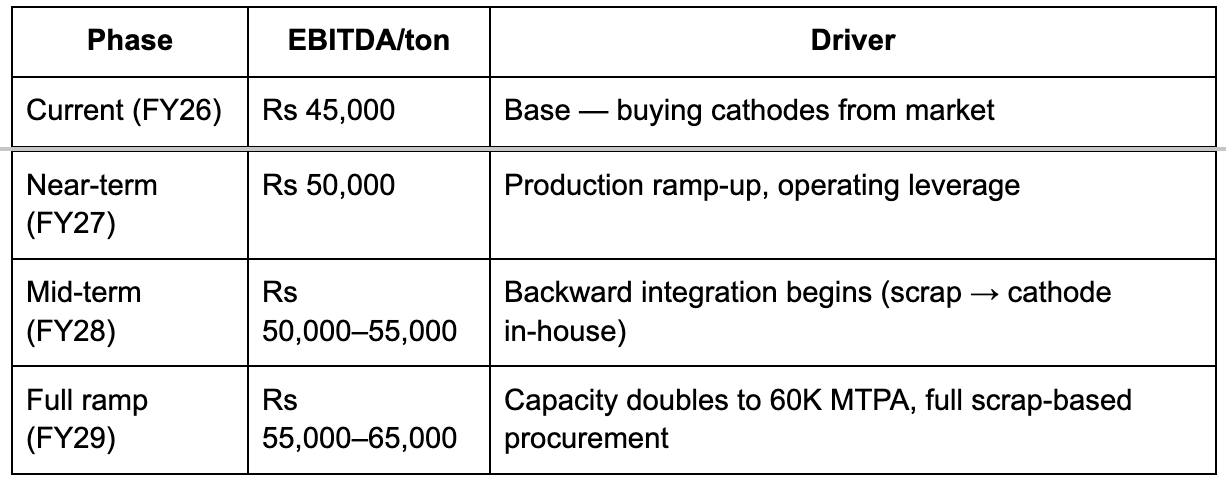

EBITDA/Ton Bridge - Detailed Walkthrough

Management provided a clear phased bridge from Rs 45,000 to Rs 65,000/ton:

Capacity doubles to 60K MTPA, full scrap-based procurement

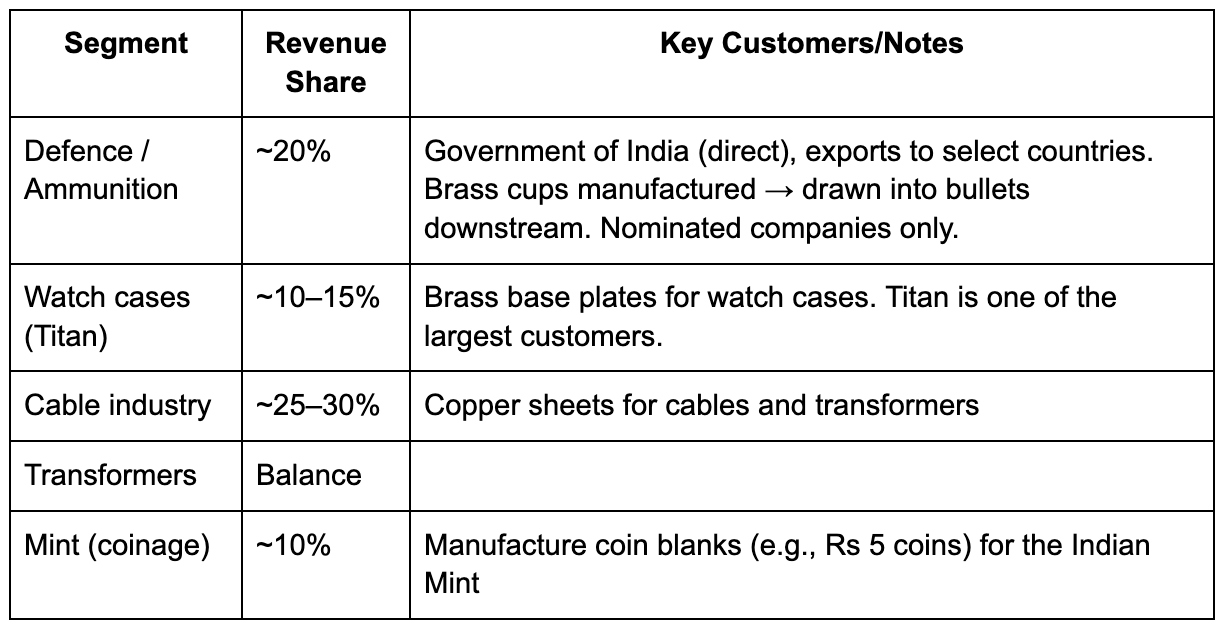

RMIL Revenue Mix by Customer Segment

Key insight: Product mix is fully flexible. Same machines can be produced for any segment with no dedicated equipment needed. Management can shift the mix based on margins/demand.

RMIL - No Commodity Sales

RMIL does NOT sell cathodes, ingots, or any commodity copper. Everything is converted into sheets, cups, foils, or other VAP.

100% value-added product output.

2. Copper Recycling Plant (Mandvi, Gujarat) - Strategy & Economics

Sourcing Strategy

Scrap types: All types of wires, motors, car parts, etc. “Scrap is scrap. The only difference is the price at which it comes.”

Simple process for wire scrap: Strip the wire → separate copper from plastic insulation → briquet → sell. Very labor-intensive, no high technology.

Why India/developing economies win: Labor is expensive in the US/Europe, making this labor-intensive stripping work uneconomical there. They export the scrap instead. India, Vietnam, China process it.

Margin logic: The simpler the scrap (e.g., plain wire), the thinner the margin — it’s a mature, transparent market. The more complex the scrap (motors, mixed electronics), the better the margin.

Scrap Sourcing - Yard Model Replication

Gravita plans to replicate its yard model (proven in Africa) in developed economies: Brazil, US, Europe.

Dual benefit: Copper scrap procurement + also source battery/aluminium scrap from the same yards.

Already dealing with many of these traders for other scrap types → existing relationships will be leveraged.

Captive vs. Third-Party Sales

Primary use: backward integration into RMIL (supply cathode to replace market purchases).

Surplus will be sold to third parties - other converters, or exported.

Arbitrage opportunity: If international cathode price > domestic price, export the recycled cathode and let RMIL buy domestically at a lower price. Capture the delta.

Logic: “Fixed costs (salaries, plant overhead) are fixed. Every extra rupee earned on surplus volume goes straight to EBITDA.”

Quality Challenge in Copper Recycling - Electrolysis Moat

This was a key insight from the call:

When you strip wire, you get multiple grades:

Grade 1 (Copper Closs): Fine quality, can be used directly.

Grade 2+ (Copper Coco and lower): Requires electrolysis to purify.

Electrolysis process: Anode → dipped in water tanks → charged → cathode extracted. Well-known process, but capex-intensive (~Rs 100 Cr to set up).

Most competitors skip the electrolysis step. They claim to produce “cathode” but without electrolysis, the product is impure → leads to rejections and quality issues at the customer end.

Gravita’s plan includes the electrolysis capex — this is a genuine differentiator and barrier to entry in copper recycling.

Competitive Landscape in Copper

The market is fairly mature. Traders are abundant and accessible - Gravita already deals with them for other scrap.

Moat is NOT in scrap procurement (anyone can buy from traders) - moat is in the yard model (last-mile collection at lower cost) + electrolysis capability + RMIL’s VAP customer base.

On competitors entering copper recycling (e.g., Pondy Oxides): “Market is fairly mature... the only difference is that today if you want to buy from traders, you can easily buy.”

Management is confident that their integrated model (scrap → recycled cathode → RMIL VAP) gives a structural margin advantage over standalone recyclers.

Plastic By-product from Copper Wire Stripping

The plastic insulation stripped from wires is sold as-is currently. No issues with finding buyers.

Long-term: exploring granulation or tile manufacturing from this plastic, but “that would come at a later stage.”

Challenge with recycled plastic: Unlike lead (infinitely recyclable with no property loss), plastic loses strength/properties with each recycling cycle. Product development for recycled plastic is time-consuming.

3. Copper Division - Financial Targets

ROCE Target

Copper division (RMIL + recycling combined) ROCE target: 25-26% by FY29 on optimum utilization basis.

Management explicitly said they view copper as ONE division - they don’t separate RMIL and the recycling plant.

ROCE expansion will be driven primarily by margin improvement (from backward integration).

Margin Trajectory

Current RMIL EBITDA margin: 7–8% (normalized, excluding unhedged copper price gains).

Target: 9–10% — comparable to lead margins.

Management claims no one in India is currently making 8–10% EBITDA margins in copper sustainably.

Took a veiled shot at competitors: “Some people say they’ll make it... their Q3 commentary had different numbers, Q4 numbers were different.” (Referring to someone who guided aggressively and then missed.)

Hedging Policy

100% hedging is non-negotiable. No intention to play on commodity swings.

Buy at LME, sell at LME. No commodity speculation.

MCX margin requirements on copper hedging will be “very small” relative to Gravita’s scale, not a concern.

EBITDA Contribution Outlook

On a 2-3 year view: Copper could be ~20% of consolidated EBITDA.

Revenue contribution will be disproportionately higher (>100% of current lead revenue eventually) because copper value per ton is ~6x lead.

Non-lead business overall could reach 40–45% of EBITDA on a 2-3 year horizon.

4. Lead Business - Capacity & Volume Update

New Capacity Ramp-Up

Recent capacity additions (Phagi + Mundra) have taken total lead capacity to ~360,000 MTPA.

FY27 lead capacity utilization expected: 40–45%.

Long-run sustainable utilization target: 60–65%.

Management is planning to take lead capacity from 360,000 to ~450,000 MTPA.

Middle East Sourcing Disruption - Resolution

Last meeting management had flagged that Middle East sourcing was disrupted and they were rerouting.

Update: Largely resolved. Shipments have started coming from a port just above Oman, past the Strait of Hormuz.

Still gradual normalization not overnight, but slowly things will start to improve

The Middle East is also a customer market (15–20% of sales), not just a sourcing market.

Volume Growth Drivers - Structural Tailwinds

Three key catalysts identified:

Reverse Charge Mechanism (RCM) on battery scrap GST:

Currently under active discussion. Will wipe out the informal market’s 18% GST arbitrage.

Management is also lobbying for a GST reduction from 18% to 5% on battery scrap; this would further destroy the informal sector’s incentive.

BWMR (Battery Waste Management Rules) - Last 3 years of compliance window:

Companies will face increasing pressure on the volume/compliance part.

This will push more domestic scrap into the organized channel.

The “loop effect” on import licenses:

Higher domestic production → higher eligibility for import licenses next year → more imports → higher production → even higher import eligibility.

5. Aluminium Business - Candid Assessment

India Operations — No Progress

India operations for aluminium are largely halted due to no clarity on hedging instruments.

MCX aluminium alloy (ADC12) hedging contract still not live. Management has been expecting it soon for over a year. The bottleneck is at the end of MCX.

Major development (off the record): Gravita has dismantled its Jaipur aluminium plant and shifted it to Mundra.

Reason: 100% imported scrap was being processed and then re-exported. Jaipur location added 15 days of extra working capital cycle + $30–35/ton additional logistics cost vs. Mundra (port-based).

This is a sensible consolidation move but confirms aluminium India operations are essentially on hold until MCX contract launches.

6. Rubber Business

Mundra rubber facility expected in H2 FY27 (not H1 as previously guided a slight delay).

Africa was the initial rubber recycling location, but that production was entirely for in-house consumption (used internally), not sold to third parties.

Romania was the first third-party sales operation for rubber.

Rubber recycling produces three outputs from tyres: steel wire, carbon, and pyrolysis oil. All three are saleable.

7. Lithium-Ion Battery Recycling

Currently at the very initial stage.

Currently doing battery → black mass conversion only.

Being treated as R&D expense - no revenue or profitability expectation.

Anything that comes from lithium would be “icing on the cake, over and above” the guidance.

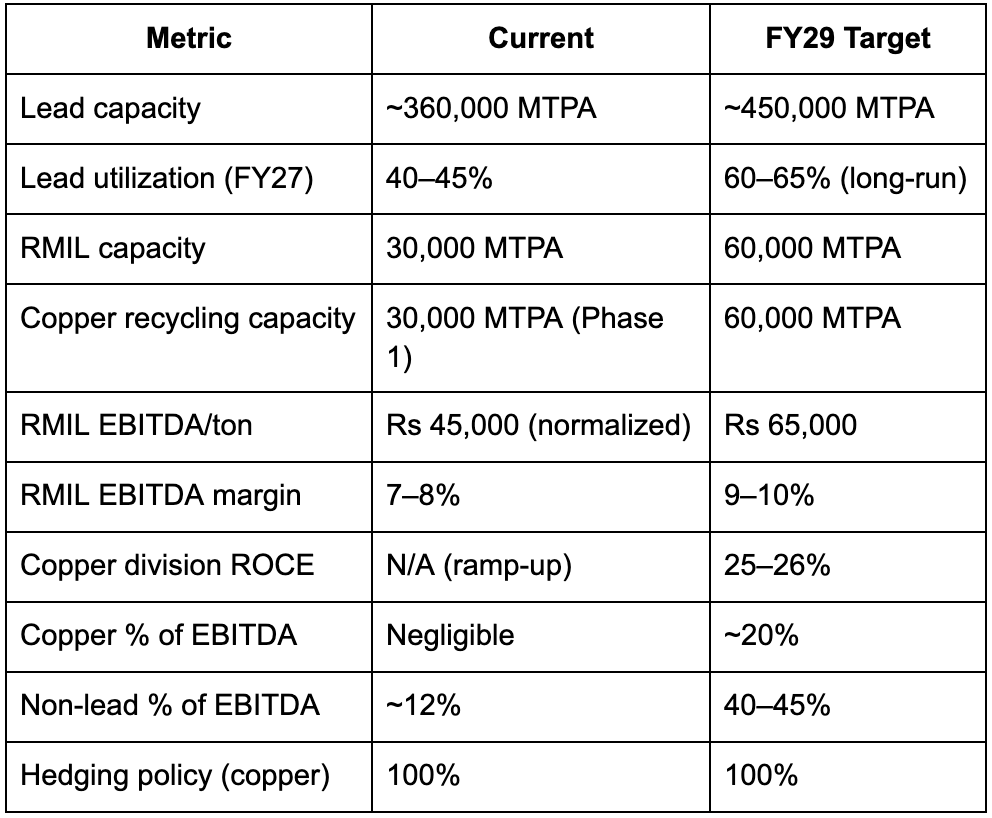

8. Key Financial Metrics & Targets Summary

9. Key Variant Perceptions & Non-Consensus Insights

Electrolysis capex (~Rs 100 Cr) is a genuine moat in copper recycling. Most competitors skip this step, producing an inferior cathode that gets rejected. Gravita is investing in this to create quality differentiation.

MCX aluminium alloy contract may be structurally blocked by a large OEM. This is not just a regulatory delay. Aluminium India scale-up could be years away, not quarters.

Competitor quality of earnings in aluminium recycling is suspect. Management explicitly called out CMR and Baheti for: (a) running unhedged commodity positions and reporting gains as operating profit, and (b) potential accounting misclassification enabled by local auditors. Worth digging into CMR’s and BTI’s auditor and hedge accounting disclosures.

Lead volume growth has a self-reinforcing loop via import license eligibility higher production → higher import quota → higher production. This is an underappreciated compounding driver.

RMIL’s FY26 volume was only 10-11K tons (vs. 31.2K capacity = ~33% utilization). The previous owner was not pushing. FY27 target of 18K tons represents genuine low-hanging fruit.

https://earningsunwrapped.substack.com/p/indias-recycling-market-is-entering?utm_source=share&utm_medium=android&r=rer2b

Wrote about Gravita and Recycling industry. The infection point is coming especially with changes in regulatory framework as well.

Bhagyanagar India and sunlite recycling are two companies worth studying in copper recycling segment.