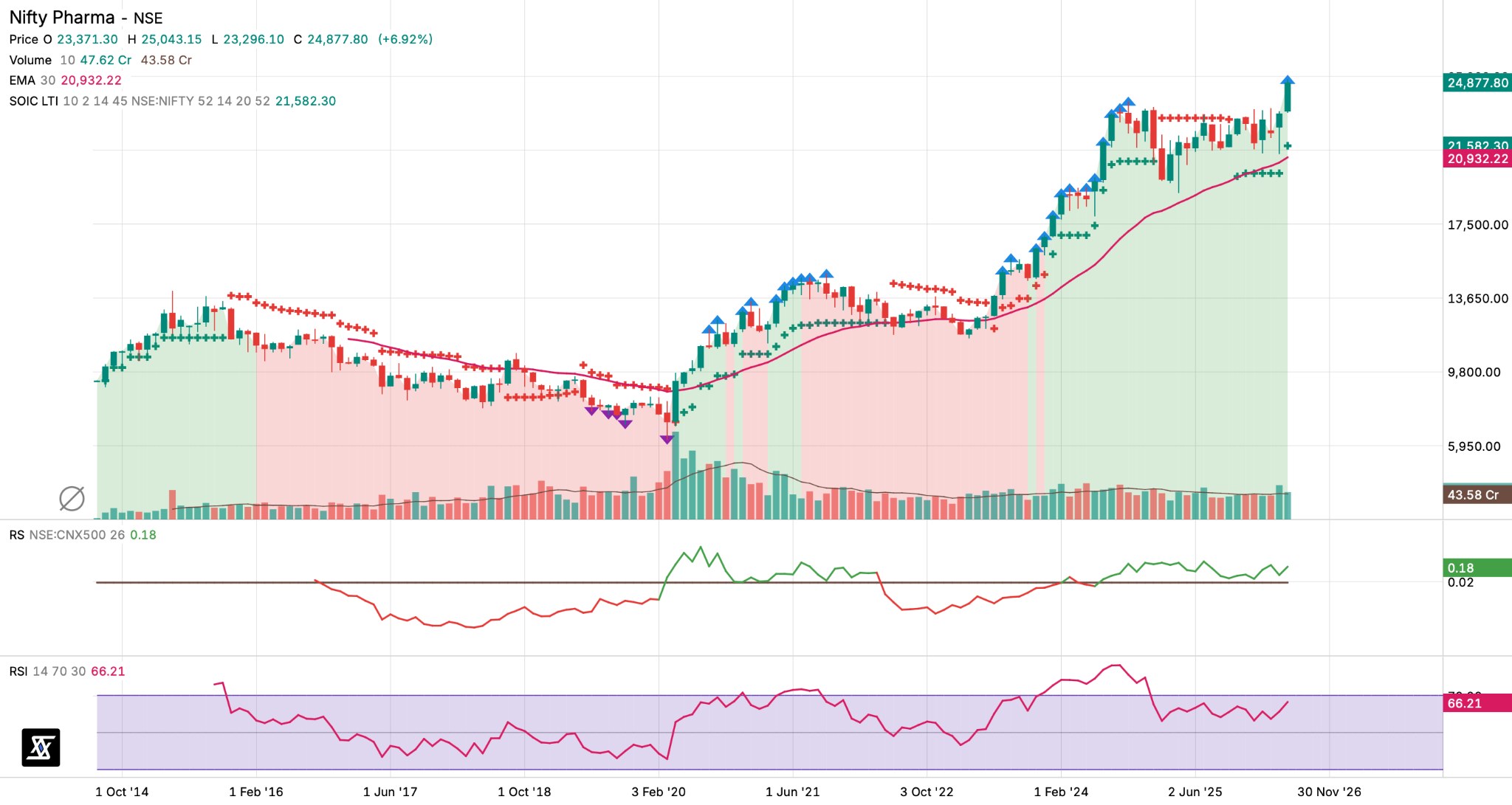

Is This The Pharma Supercycle?

But what’s shifting here? Let’s break this down with Q4FY26 results

The Nifty Pharma index is at all-time highs. Not on the back of a single blockbuster launch or one company’s breakout quarter but because the entire value chain, from intermediates makers to CDMO players to branded formulations are firing on all cylinders simultaneously. That almost never happens in a sector this broad.

Source - stockscans.in

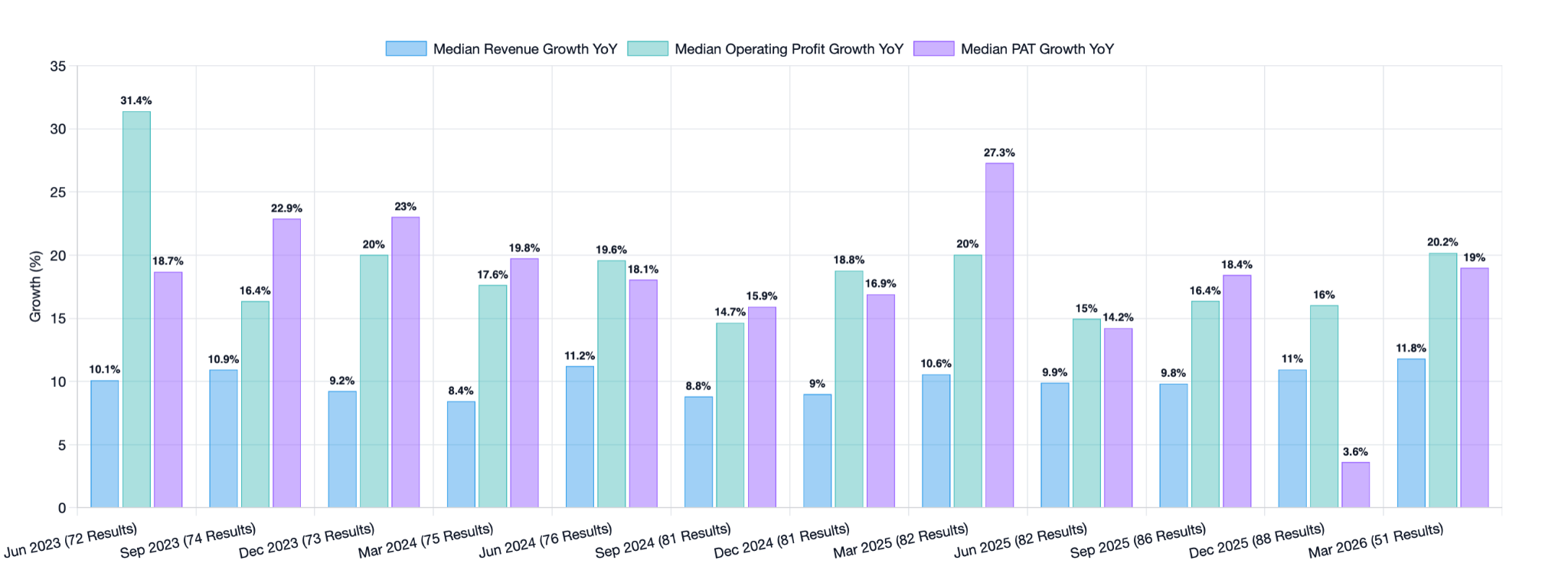

Look at the numbers that rolled in across Q4 FY26 earnings season: median revenue growth for the listed pharma universe is comfortably in double digits consecutively for 2 qtrs in a row now which has happened almost after 10 qtrs now . But what makes this cycle different from previous ones and what’s really driving the re-rating is that the quality of growth has fundamentally changed. This isn’t just topline growth anymore. Its topline growth is accompanied by a sustained EBITDA margin expansion cycle, something the sector hasn’t seen since the pre-2018 golden era.

Source - stockscans.in

Just before diving into the detailed breakdown here is the standard disclaimer that we are SEBI Registered Research Analyst and nothing that will be discussed here is a buy/sell recommendation. Please do your own research before making any financial decision.

Getting back to the discussion,

So Consider a few data points from the companies that reported this quarter to comprehend what I am trying to explain above:

Zydus Lifesciences delivered consolidated revenues of 27,150 Cr for FY26, up 17% YoY, with an EBITDA margin of 31.2% which is the highest-ever operating margin in the company’s history. G

anesh Nayak, Director at Zydus, opened the earnings call saying: “I’m happy to inform you that we have ended the fiscal 2026 on a strong note. Overall, we delivered healthy double-digit growth during the year ahead of our expectations. Even after adjusting for acquisitions, the base business grew in double digits.”

Lupin reported its 15th consecutive quarter of YoY growth with the highest-ever sales and profitability. The US business alone hit $1.3 billion for FY26, growing an extraordinary ~40% YoY.

Vinita Gupta, CEO, captured the mood: “FY26 has been a stellar year for the organization, with revenues and profitability at record levels.”

Neuland Labs, a specialty API and CDMO player, posted Q4 FY26 revenue of 789 Cr up 135% YoY with an EBITDA margin of 40.5%. Seems phenomenal right. A 2,300 basis point margin expansion in a single year.

Granules India crossed the 5000 cr revenue milestone in FY26 for the first time, growing 20% YoY, with gross margins expanding 355 bps to 65% which is the highest gross margin the company has ever achieved.

Mankind Pharma reported FY26 revenue of 14,278 Cr (+17% YoY) with adjusted EBITDA margins of 25.4%.

Rajeev Juneja, Vice Chairman & MD, went beyond the numbers to signal the strategic pivot underway: “As the industry landscape transforms, our strategic focus is now increasing towards specialty chronic therapies and R&D-led innovation products. We continue to invest in and adopt best-in-class technologies enabling us to build a more resilient, differentiated, and future-ready organization.”

And interestingly these are not isolated stories but there are many names in this year end result season that has seen earnings upgrade which is driven by multiple structural tailwinds:-

1. US Generics Pricing Has Stabilized. After years of brutal price erosion that decimated returns for Indian exporters, the US generics market has found a floor. Companies are now reporting low-single-digit price erosion (or even flat pricing) versus the high-single-digit or double-digit declines of 2017-2022

More importantly, the product mix has shifted decisively toward complex generics, biosimilars, controlled drug substances, and specialty products where margins are structurally higher.

Lupin’s Vinita Gupta noted that the company plans to “double the share of complex products in our US business led by respiratory and complex injectables augmented by our biosimilars in the next couple of years.”

2. The China+1 Shift Is Real and Accelerating. For CDMO and API players, the geopolitical realignment away from Chinese supply chains has moved from thesis to revenue line item. Akums Drugs secured a €200 million multi-year European CDMO contract that’s progressing towards FY28 commercialization.

Sai Life Sciences’ CEO Krishna Kanumuri affirmed: “We believe the long-term fundamentals of innovation-led outsourcing and supply chain diversification continue to remain strong, and we are well positioned to participate meaningfully in this opportunity.”

Also this statement gets confirmed if one understands the real growth of Wuxi (China’s largest innovator CDMO company). WuXi Chemistry’s FY2025 revenue reached RMB 36.47B, up 25.5% YoY, with TIDES revenue up 96.0% YoY. That 25.5% headline looks incredible, but the TIDES segment (primarily GLP-1 peptide manufacturing) is doing the heavy lifting.

Doing some back of the envelope calculations using the quarterly disclosures for Q1-Q3 2025 TIDES revenue grew 121.1% YoY to RMB 7.84B and FY2025 TIDES growing 96%, TIDES was likely ~RMB 10B for FY2025 off a ~5B FY2024 base. That means ex-TIDES Chemistry revenue grew roughly 10-11%, not 25%. The TIDES segment alone contributed nearly half the incremental revenue growth of the entire Chemistry division. Which shows that ex of GLP-1 tailwinds the base growth of the business very slow compared to what we see in some of the Indian innovator CDMO companies.

3. The Indian Pharma Market (IPM) Is Growing ~10% and Getting More Profitable. India’s domestic branded pharma market continues to compound at ~10% led by chronic therapies. The more significant trend is the chronic shift where companies are deliberately increasing their share of chronic prescriptions (cardiac, diabetes, respiratory) which offer more predictable, annuity-like revenue versus seasonal acute therapies.

Mankind’s chronic share has increased from 38% to approximately 40%, Zydus is at 46.3%, and Lupin is at 66%, all heading higher.

4. GLP-1/Semaglutide has Created a Massive New Therapeutic Category. The launch of branded generic semaglutide in India by Zydus, Lupin, Torrent, and now Mankind has opened a multi-thousand crore addressable market almost overnight.

Dr. Sharvil Patel of Zydus described the strategy: “We have launched a novel formulation on sema... together we control a very meaningful part of the market share on semaglutide... we are now number two in terms of share, and closely followed by Lupin, and Torrent also has gained strong share.”

In this tweet one can check what is happening in this space and where is the opportunity….

5. Geopolitical Disruptions Are Creating Pricing Power. The ongoing Middle East conflict has disrupted shipping routes and inflated logistics costs, but for Indian manufacturers with domestic supply chains and inventory buffers, it has also created short-term pricing power.

Caplin Point’s Chairman, C.C. Paarthipan, noted their anti-fragile model: “Our model of keeping the goods next to the customer in the last 20 years has produced this compounding effect. Hence, we always keep the goods in our subsidiary warehouses for a minimum of 6 months’ stock.”

6. The Biosimilar Wave Is Hitting the US Market. Indian companies such as Biocon, Zydus, Lupin are at the forefront of the biosimilar revolution in the US. Biocon’s biosimilar segment alone reported FY26 revenue of 10,431 Cr, up 16% YoY. Zydus filed an NDA for semaglutide and launched the world’s first nivolumab biosimilar (Tishtha). Lupin has 4 biosimilars in its US pipeline. This is an entirely new profit pool being unlocked.

7. Margin Expansion Is Structural, Not Cyclical. The margin expansion across the sector isn’t just operating leverage on a good quarter. It’s driven by product mix improvement (higher share of complex/chronic/specialty products), better pricing discipline, lower R&D intensity for some players, and in many cases, genuine operational efficiencies.

Strides Pharma’s MD Badree Komandur captured this well: “Profitability has been the cornerstone of our transformation journey... EBITDA has compounded at approximately 26% over the last 3 years, driven by EBITDA margin expansion of 400 basis points to close FY26 at 19%.”

Just before going ahead one should understand that Pharma is not one piece where broader tailwinds can find niche winners but it has multiple smaller themes running inside it.

A specialty API maker like Neuland Labs operates in a completely different business environment than a domestic branded player like Mankind, which in turn has almost nothing in common with a patented CDMO like Syngene/Sai. They have different customers, different competitive dynamics, different margin profiles, and different growth drivers.

Here’s how the value chain of Pharmaceutical players look like -

Intermediates → API (Generic/Specialty) → Formulations (Domestic/ROW/USA) → Patient

Then there are these CDMO players who serves innovator pharma companies NCE/Innovation drug discovery, biosimilars, novel biologics and then Domestic Branded India prescription-driven, doctor-detailing led businesses

So with this background let’s get on and dive deeper on the themes in this space that have performed strongly and the tailwinds that are there in each of the themes …

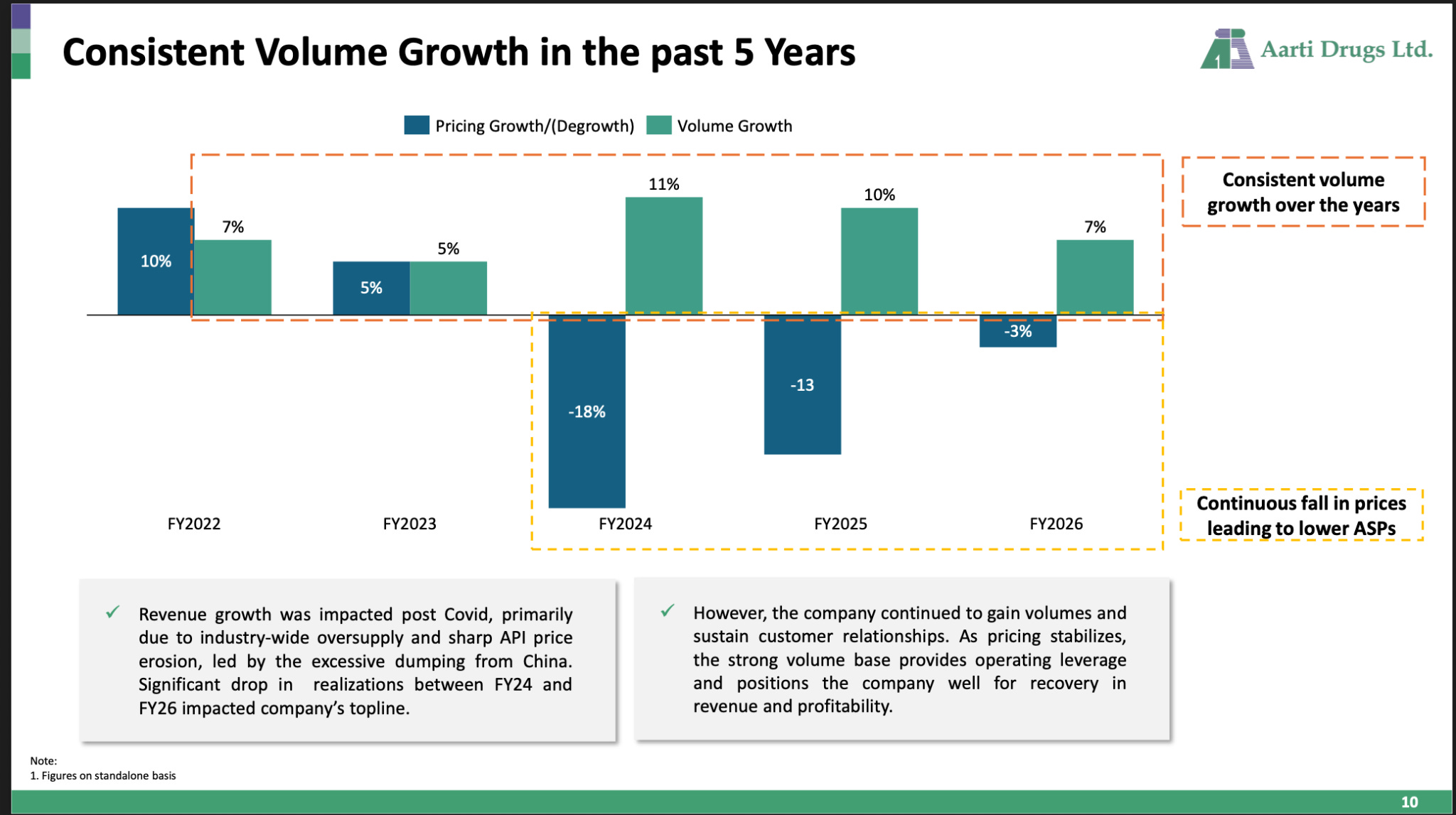

1) Aarti Drugs - The Aarti Drugs story over the last three years can be summed up in this single chart

The company has delivered consistent positive volume growth every single year for the last 5 years: 5%, 11%, 10%, 7% respectively from FY22 to FY26. But the pricing variance has been savagely negative: -13%, -18%, -3% across FY22 to FY25. Volume kept growing. Revenue didn’t because the price kept falling.

This is the defining characteristic of the API pricing down-cycle. Companies that maintained customer relationships, invested in capacity, and kept shipping volumes were running on a treadmill growing units sold but seeing realizations collapse due to Chinese dumping and global oversupply.

But is the inflection here?

CFO Adish Patil opened the earnings call with a notable change in tone: “Towards the end of FY26, we were impacted by elevated input costs and supply chain constraints for crude and gas-based raw materials due to the West Asia war... Encouragingly, pricing trends started stabilizing from September 2025 onwards, and this recovery strengthened further during Q4 FY26, supported by increasing crude prices.”

FY27 Outlook and What to Watch

Management guided for 10-15% volume growth as the internal target, with pricing variance now expected to be positive as long as the West Asia situation persists and crude remains elevated. The cautionary note was interesting if API prices go too high, it can actually hurt domestic demand for older-generation antibiotics because Indian formulation companies face NLEM price caps and can’t pass through elevated API costs to patients.

“Our internal target will always be in the range of 10-15% growth... if crude prices remain very high, then the older generation antibiotics see a drop in demand when the API becomes very expensive.”

On margins: management doesn’t expect dramatic gross margin expansion but flagged that the flow-through to EBITDA will be better if absolute gross profit per kg improves. The methylamines (backward integration where utilisation can improve in next 1 yr) ramp-up should add ~100 bps to EBITDA margin structurally. The target over the next 2-3 years is to get EBITDA margins back to the mid-teens range from the current 12-13%.

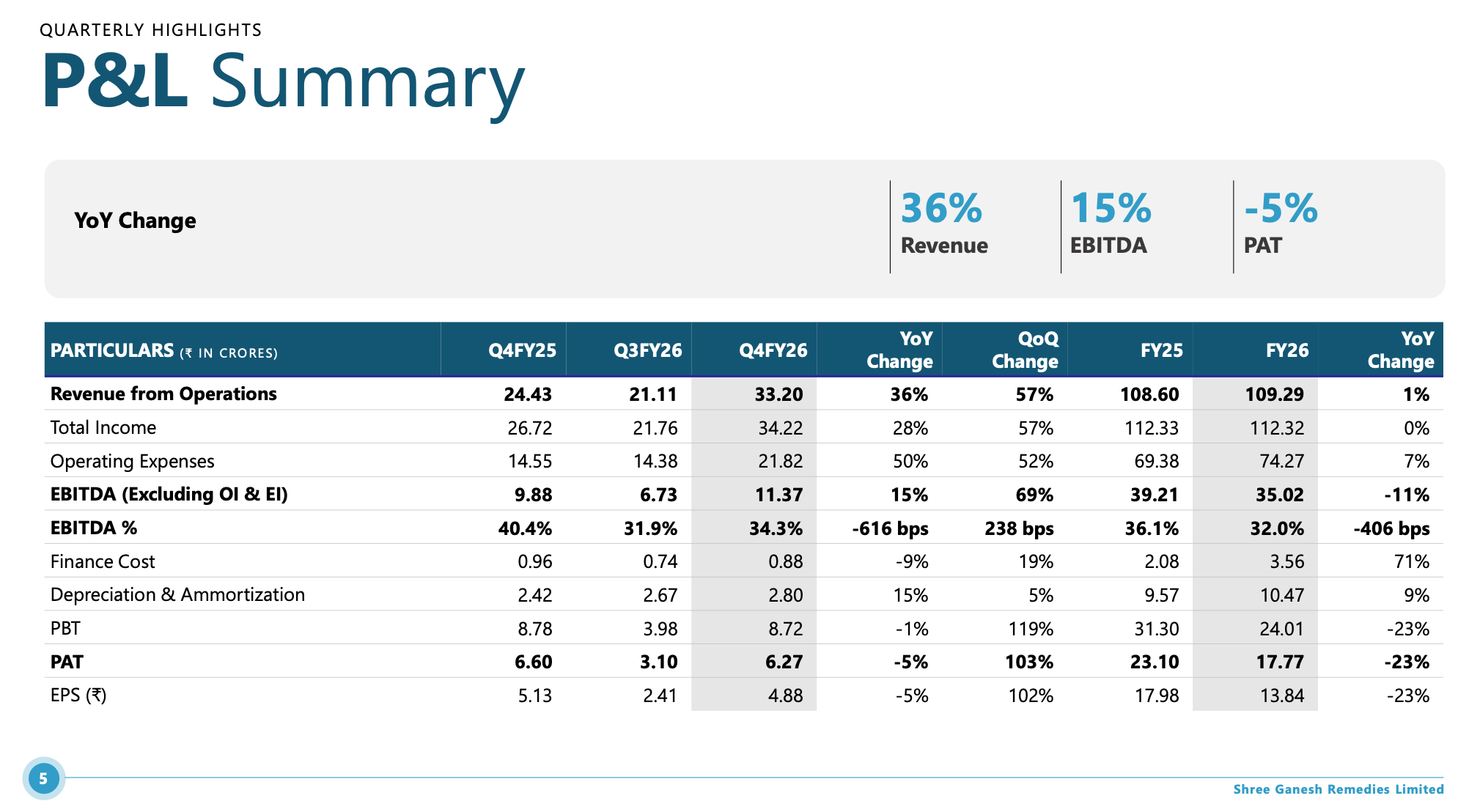

2) SGRL (Shree Ganesh Remedies) - Small, Niche, and Playing a Completely Different Game

Parth Kotia, Whole-time Director and CFO, was refreshingly candid about FY26: “As we had communicated at the beginning of the financial year, FY26 was always envisioned as a year of consolidation for the company. The financial performance does not point to material growth on a full-year basis, and I want to be candid with you. However, FY26 was never designed as a year of aggressive top-line expansion; it was a year of deliberate groundwork.”

The most significant development at SGRL is the progress on CRAMS (Contract Research and Manufacturing Services) engagements. This is SGRL’s play to transition from being a standalone intermediates maker to being a custom synthesis partner for European and Japanese innovators.

The milestone achieved in Q4 is important: “I am very pleased to share that we have made strong progress on our CRAMS engagement across the agrochemical, pharmaceutical, and electronic applications... During Q4 FY26, we successfully completed the pilot trials for these projects. This is an important milestone... We will now move to the commercial trial stage.”

Pilot trials completed. Commercial trials next. Then commercial production. This is the classic CRAMS progression ladder, and SGRL appears to have cleared the hardest rung proving to demanding European and Japanese customers that they can execute at pilot scale.

FY27 Outlook - From Consolidation to Contribution

Management was careful not to over-promise but the directional signals are clear: “FY27 should be the year in which the groundwork laid during FY26 begins to translate into more visible business outcomes. With our pilot facility now fully active, Block 7 expected to commence commercial production in Q2 FY27, our CRAMS projects transitioning from pilot trials to commercial trials... we believe the company is structurally more ready than at any point in its recent history.” (Source: SGRL Q4 FY26 Concall Transcript, fetched URL, Management Opening Remarks)

At 109 Cr revenue and a 730 Cr market cap, SGRL is a micro-cap. The CRAMS commercialization and Block 7 ramp-up could be genuinely transformative for a company this size; even a single successful CRAMS molecule could add 20-30% to the topline. But the risks are proportionate: customer deferrals, European slowdown, and the inherent uncertainty of moving from pilot to commercial scale. The journey can be lumpy but one can definitely watch over if the company is able to execute over the years.

These first 2 were specially the names where headline numbers were not that great but there might be stage set for Fy27. One has to watch for the triggers and how those triggers plays out.

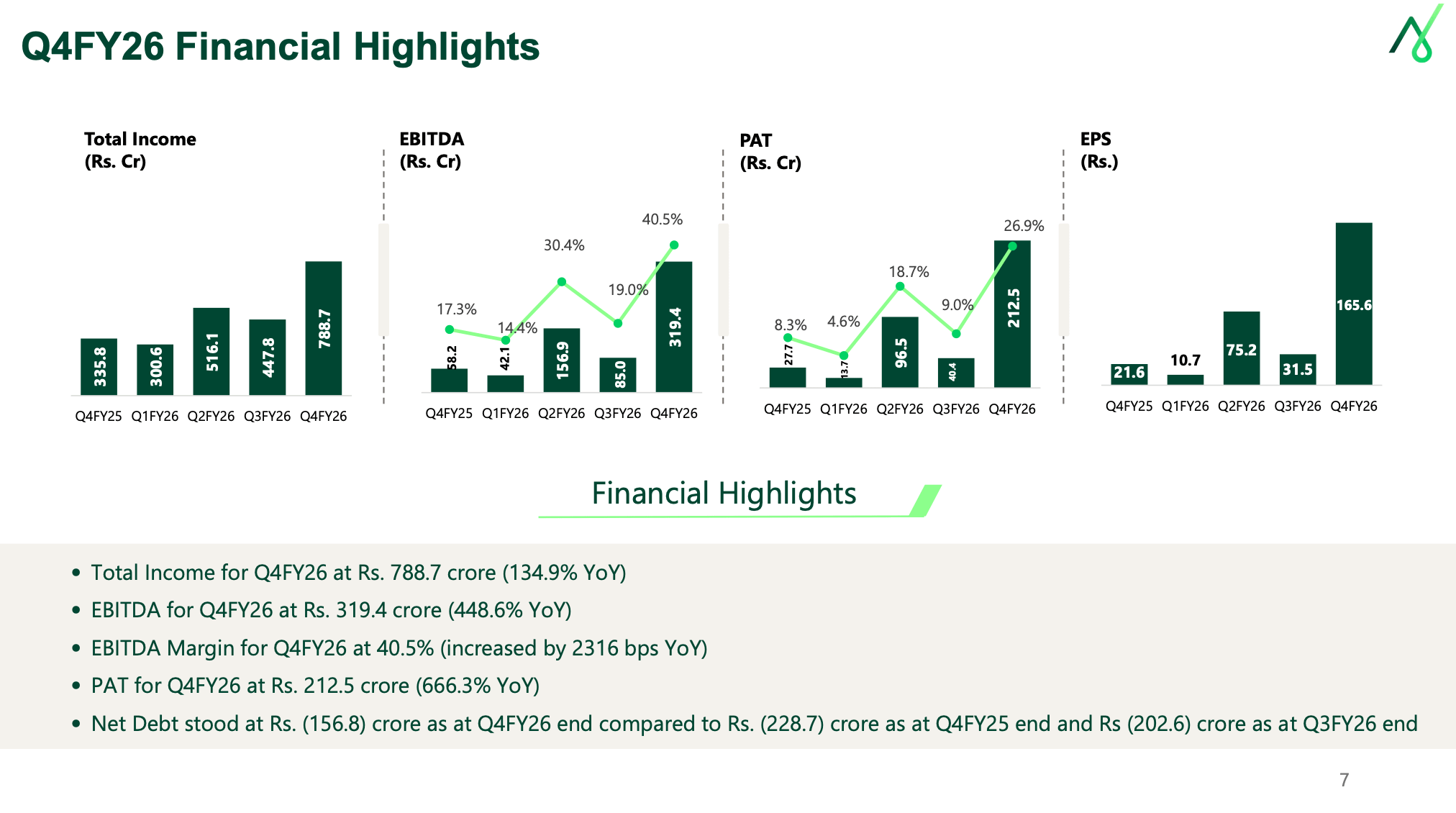

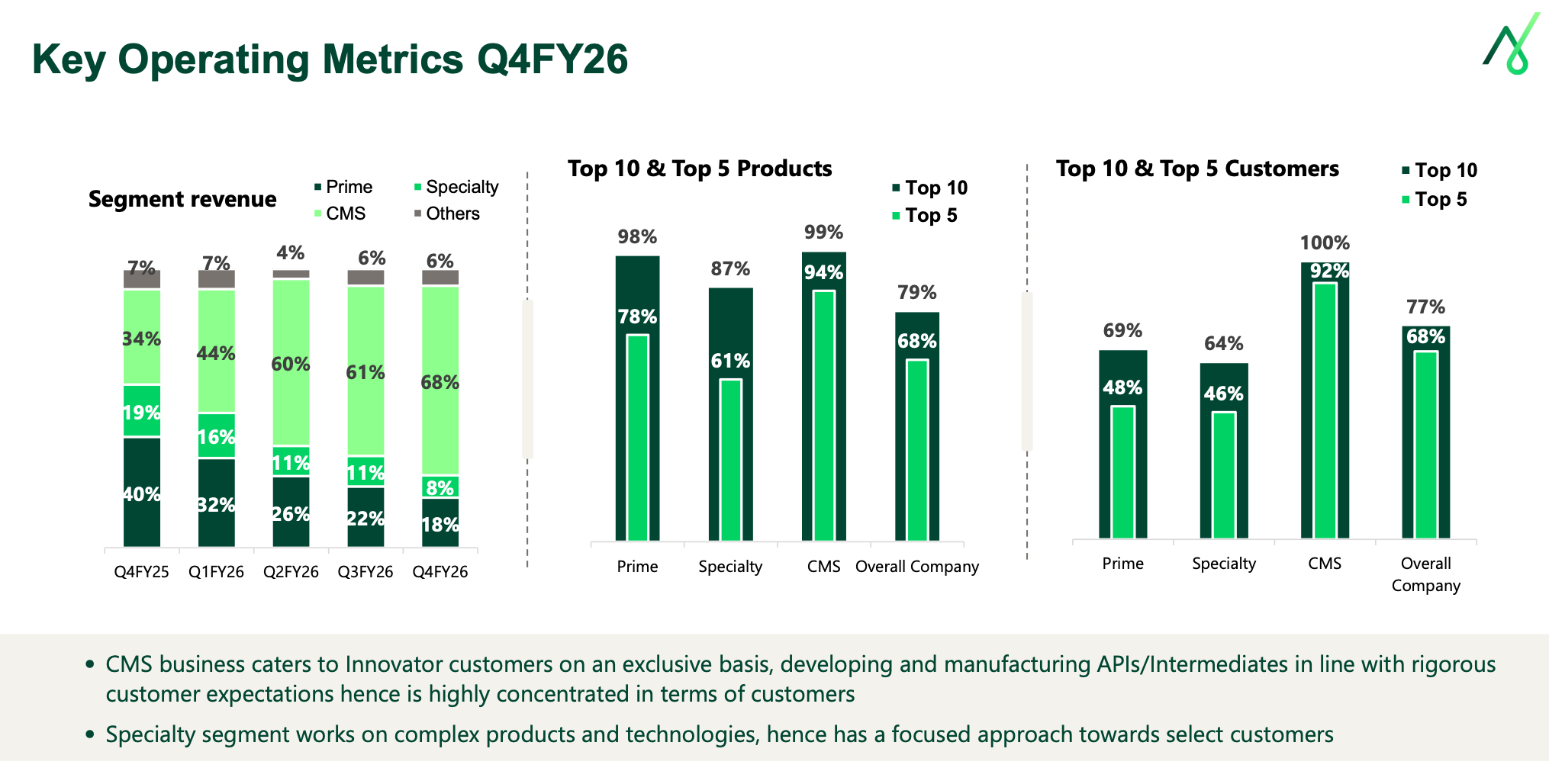

3) Neuland Labs - The Standout Quarter in All of Indian Pharma

There is no other way to say this Neuland Labs delivered what is arguably the most remarkable single quarter in the entire Indian pharma earnings season. Q4 revenue of 789 Cr represents a 135% YoY increase. EBITDA margin of 40.5% is extraordinary for any company in the pharma value chain, let alone an API/CMS player. To put it in perspective, Neuland’s single quarter EBITDA of 319 Cr is nearly as large as what the company earned in the entire previous year

And the key driver again this time was the CDMO segment for the company and mind you this can be lumpy…

Saharsh Davuluri was careful to frame the context correctly and this framing is critical for understanding the business: “The same lumpiness that resulted in a record-breaking Q4, if you recall, also made the previous quarter, which is Q3 FY26, a relatively muted quarter. And it’s worth stating the obvious: the lumpiness does not recognize financial year boundaries. It doesn’t care about March 31.”

What’s Actually Driving This Performance?

The Neuland story isn’t just about one good quarter. Its about a multi-year strategic transformation from a generic drug substances (GDS) company to a custom manufacturing services (CMS) platform.

Beyond the current commercial CMS engine, Neuland is making a significant capital allocation decision that could define the company’s next growth phase: large-scale peptide commercial manufacturing.

The context here is the GLP-1 revolution. Semaglutide, tirzepatide, and the broader GLP-1 RA class are peptide-based drugs generating tens of billions in global sales. The manufacturing of peptide APIs is complex, capacity-constrained globally, and dominated by a handful of players. If Neuland can establish credible large-scale peptide manufacturing capability, it unlocks access to what is arguably the single largest growth opportunity in pharmaceutical manufacturing over the next decade.

Growth trajectory for the next 3-4 years should be good for a company where on a 3-4 yr basis the company is looking to grow at a 20% CAGR with margins improving as the CMS mix stabilises for the company + scaling up of Peptide business where management is looking to scale it in the similar manner as CMS.

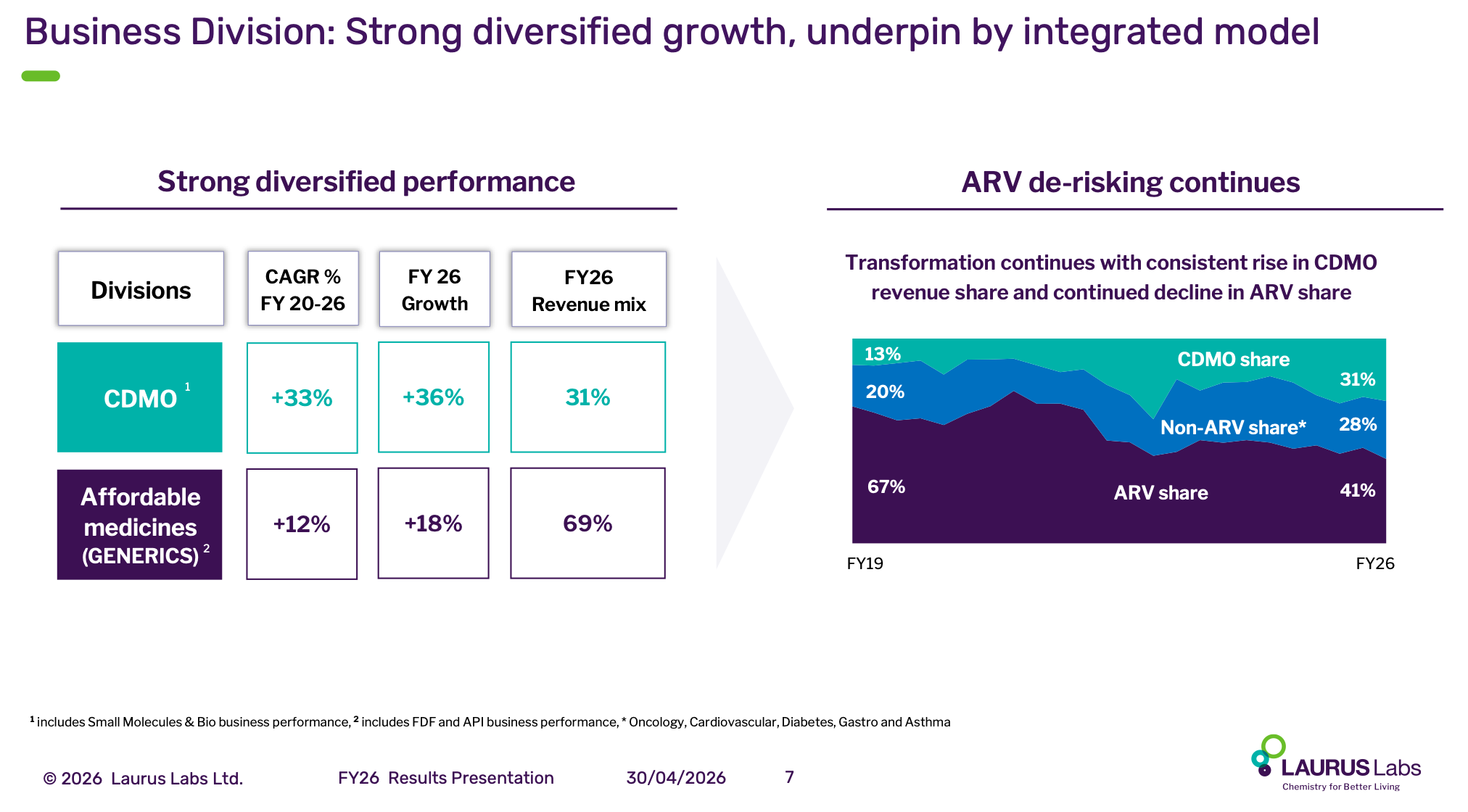

4) Laurus Labs - The Recovery Year, and What Comes Next

Laurus Labs FY26 was a definitive recovery year after the FY25 slowdown. Revenue grew 23%, EBITDA margins expanded 670 bps to 26.8%, and the strategic transformation of the business portfolio continued to accelerate.

Dr. Satyanarayana Chava set the tone: “In 2026, we significantly accelerated our performance, reflecting sustained demand in technology-driven commercial offerings. The transformation of our portfolio is well underway. The momentum is building as we continue to execute on our strategy with clear focus.”

The most important long-term trend at Laurus isn’t any single quarter’s numbers its the portfolio mix shift that has occurred over the last 6 years

Laurus has several large capital projects in various stages of execution, all designed to support the next phase of growth:

Unit 7 (Greenfield, Vizag): First production ready for commercial validation by March 2027, with four additional manufacturing blocks during FY28, adding 2,000+ cubic meters of reactor volume.

Peptide Manufacturing: Commercial scale block ready for validation during Q2 FY27.

Laurus Bio (Fermentation): Greenfield site Phase 1 starting by the end of 2026.

KRKA JV (Formulations): Phase 1 completion by mid-2027.

Total reactor volume has exceeded 8,200 cubic meters, Dr. Chava noted that “90% of project spend is towards mid- and large-scale manufacturing.” The message is clear: Laurus is betting heavily on its ability to attract large-scale manufacturing programs from global innovators, and it’s building the infrastructure to back that bet.

5) Solara Active Pharma - The Turnaround in Progress, Dragged by Ibuprofen

Solara’s story in Q4 FY26 is a tale of two businesses running in opposite directions. And until the company resolves this split, the market will struggle to price it correctly.

The “good” is the base API business of approximately 70 commercialized products across multiple therapeutic areas, operating at 54% gross margins and 26% EBITDA margins. This business is genuinely healthy, growing, and has a diversified customer base (top 15-20 products drive ~75-80% of revenue, no single molecule dominance). Capacity utilization sits at approximately 70%, leaving significant headroom for incremental revenue on a largely fixed cost base.

The “bad” is Ibuprofen which is Solara’s legacy large-volume API product that is running at negative EBITDA. The company is not backward integrated in Ibuprofen (it sources IBB, the key starting material, externally), which means it’s exposed to raw material price volatility without the ability to manage costs upstream.

The board has appointed bankers to evaluate strategic options for the Ibuprofen business. When asked for specifics, management indicated: “The Ibuprofen business has been a drag for us, and continues to be a drag. I believe we’ll be in a better position to put out the conclusion on this strategic piece in H1 of this financial year.”

Solara is a microcosm of the broader generic API industry’s challenge. The base business diversified, multi-product, regulated-market-focused can generate 25%+ EBITDA margins. But commodity, non-integrated products like Ibuprofen (where Chinese competition is fierce and cost structures are unfavorable) destroy value. The resolution of Ibuprofen will determine whether Solara is a 16% EBITDA margin company (dragged down by losses) or a 25%+ margin company that can re-rate meaningfully.

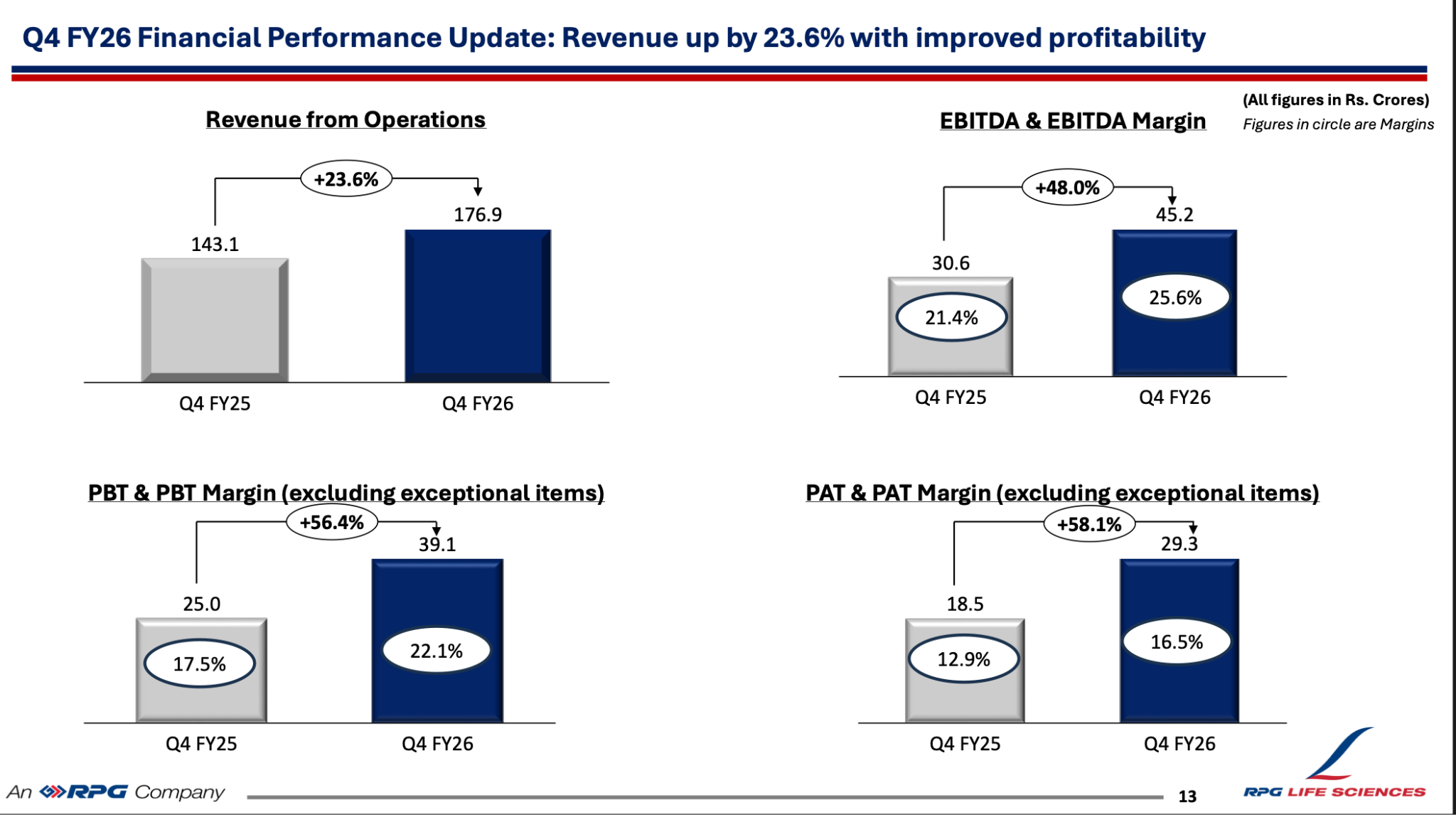

6) RPG Life Sciences - Not Quite a Pure API Play, But the API Recovery is Worth Noting

RPG Life Sciences is primarily a domestic branded formulations company (69% of revenue), not a pure API player. It belongs more naturally in the Domestic Branded section. However, its API segment (13% of revenue) has a noteworthy Q4 recovery story that illustrates broader trends in the generic API space, which is why we’re touching on it here.

RPG’s API business had a difficult year where it suffered a fire incident at its manufacturing facility earlier in FY26 that disrupted production for the majority of the year. The plant was restored by September 2025, validation completed thereafter, and Q4 saw a meaningful bounce-back with API revenues hitting 33.3 Cr. MD Ashok Nayak highlighted: “Despite our plant remaining affected due to the fire impact for the larger part of the year, we are happy to share that we have grown 5% year-over-year, thanks to the team’s resilience and strong fundamentals of our API business.”

The company’s API portfolio centers on immunosuppressants (Azathioprine) and niche generics (Haloperidol, Risperidone, Nicorandil) more specialty in character than commodity. The real story at RPG Life Sciences, however, is the domestic formulations outperformance: the company grew 1.8x the IPM rate in Q4 (18.2% vs. IPM’s 10.1%), improved its IPM ranking from 58 to 52, and is building its nephrology (+55%), rheumatology (+40%), and oncology (+23%) portfolios aggressively.

In general seeing the trends here in these Intermediary players and API Players one can figure this much out that -

Generic API is at a cycle inflection, but the recovery will be gradual. Pricing is stabilizing (Aarti Drugs flagged September 2025 as the turning point), volumes are compounding, and backward integration projects are beginning to bear fruit. But generic API margins at 12-13% are still well below the mid-teen peaks of the previous cycle. The recovery requires sustained positive pricing variance, which in turn depends on either continued geopolitical disruptions (the West Asia war inflating crude and input costs) or a genuine structural reduction in Chinese competition (more lasting but slower).

Specialty API/CMS players command premium valuations because they’ve escaped the commodity trap, they compete on capability, not price. Generic API players trade at lower multiples because the market views them as price-takers in a commoditized business. The Q4 data suggests that generic API is at the best starting point in 3 years for a potential re-rating but only if the pricing cycle cooperates. Specialty API/CMS, meanwhile, has already re-rated but has the growth visibility and structural moats to justify it.

The single most important trend cutting across both sub-segments: peptide manufacturing capability is the new frontier. Neuland is investing in large-scale peptide commercial facilities. Laurus has a commercial-scale peptide block ready for validation in Q2 FY27. The GLP-1 wave (semaglutide, tirzepatide) has created unprecedented demand for peptide API manufacturing, and the companies that build credible, scaled peptide capabilities over the next 2-3 years will unlock the largest single growth opportunity in pharmaceutical manufacturing.

Now let’s see some strong results in the formulators space -

This section splits the formulation universe into three sub-categories, each with distinct economics, competitive dynamics, and growth drivers: Domestic Branded, International/ROW, and US Formulations.

DOMESTIC BRANDED FORMULATIONS

The Indian Pharmaceutical Market (IPM) grew approximately 9.9-10.1% in Q4 FY26 and ~8.6-9.9% for the full year. But beneath the headline, three transformative shifts are underway that are reshaping competitive dynamics and profitability:

1) The Chronic Shift. - Chronic therapies (cardiac, diabetes, respiratory, CNS) are growing faster than acute therapies (antibiotics, anti-infectives, pain) and now dominate the portfolios of leading companies.

2) The GLP-1/Semaglutide Disruption - The launch of branded generic semaglutide in India by Zydus, Lupin (co-marketed with Zydus), Torrent, and now others has created a multi-thousand crore addressable market almost overnight

3) The Modern Trade and Digital Channel - OTC and consumer health segments are seeing 30-60% growth through e-commerce and modern retail channels, creating a parallel growth engine beyond traditional doctor-detailing.

Let’s go company by company.

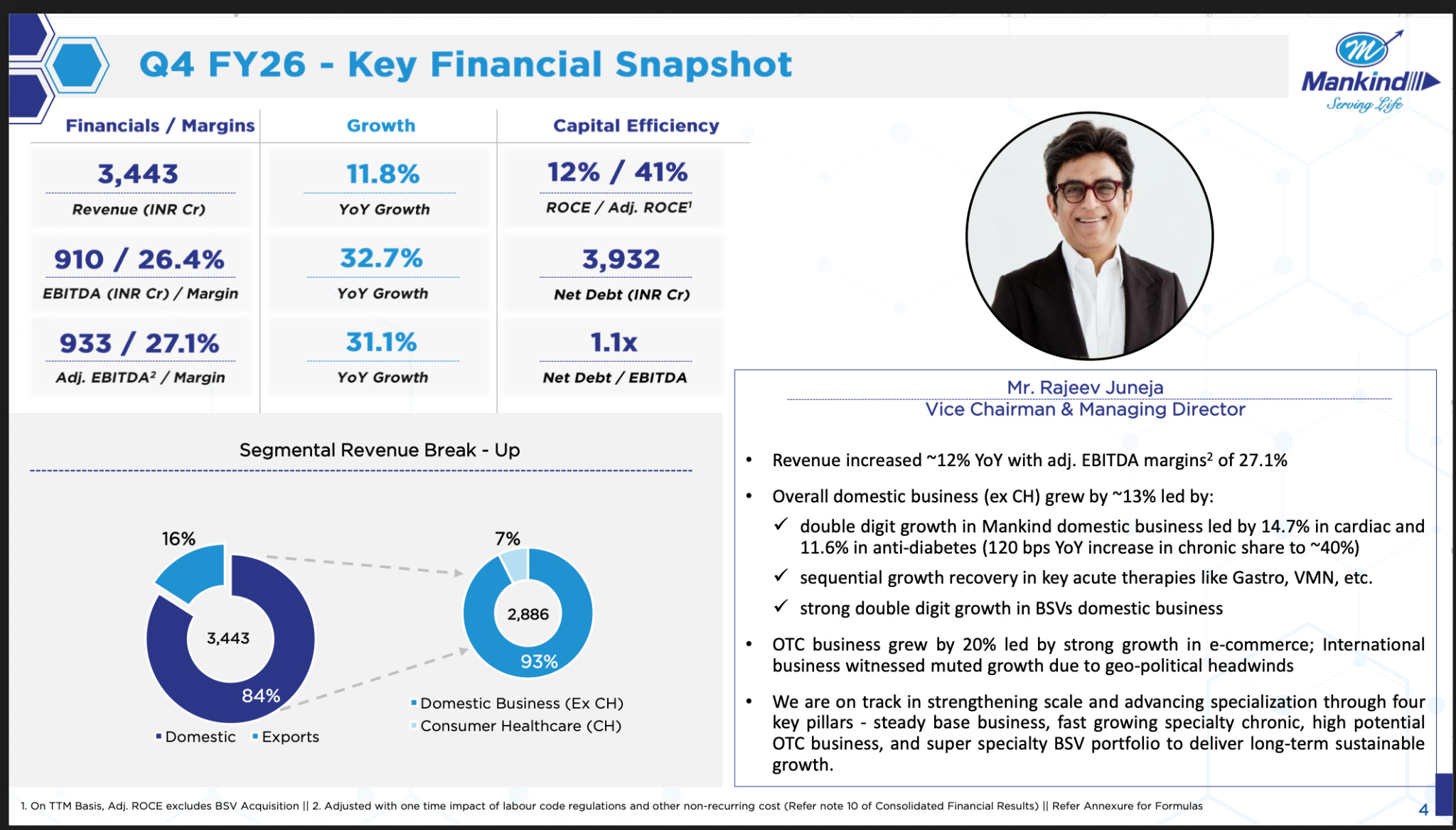

7) Mankind Pharma — India’s #1 Prescription Company

Mankind holds the #1 rank in Indian pharmaceutical prescriptions, a position it has maintained for 9 consecutive years. The FY26 story is dominated by two narratives: the ongoing integration of BSV (Bharat Serums & Vaccines, acquired in FY25 for ~13,600 Cr) and the strategic pivot toward chronic and specialty therapies.

Vice Chairman Rajeev Juneja articulated the shift: “As the industry landscape transforms, our strategic focus is now increasing towards specialty chronic therapies and R&D-led innovation products. We continue to invest in and adopt best-in-class technologies enabling us to build a more resilient, differentiated, and future-ready organization.”

BSV Integration: The fertility and women’s health portfolio from BSV contributed meaningfully, though the integration is still in early stages. Mankind’s consumer healthcare brands (Manforce, Gas-O-Fast, Prega News) continue to scale through modern trade channels.

Management guided FY27 EBITDA margins of 25.5-26.5%, up from 25.4% in FY26, suggesting incremental margin expansion through operating leverage and BSV synergies. However, there’s a critical tax headwind: the effective tax rate is expected to jump from ~17% in FY26 to 25-26% in FY27 as tax holidays expire

Semaglutide strategy is clear to let the storm pass. Unlike Zydus and Lupin which launched aggressively, Mankind has been more measured on semaglutide prioritizing margin discipline over first-mover advantage. This is consistent with Mankind’s historically conservative approach to new therapy areas.

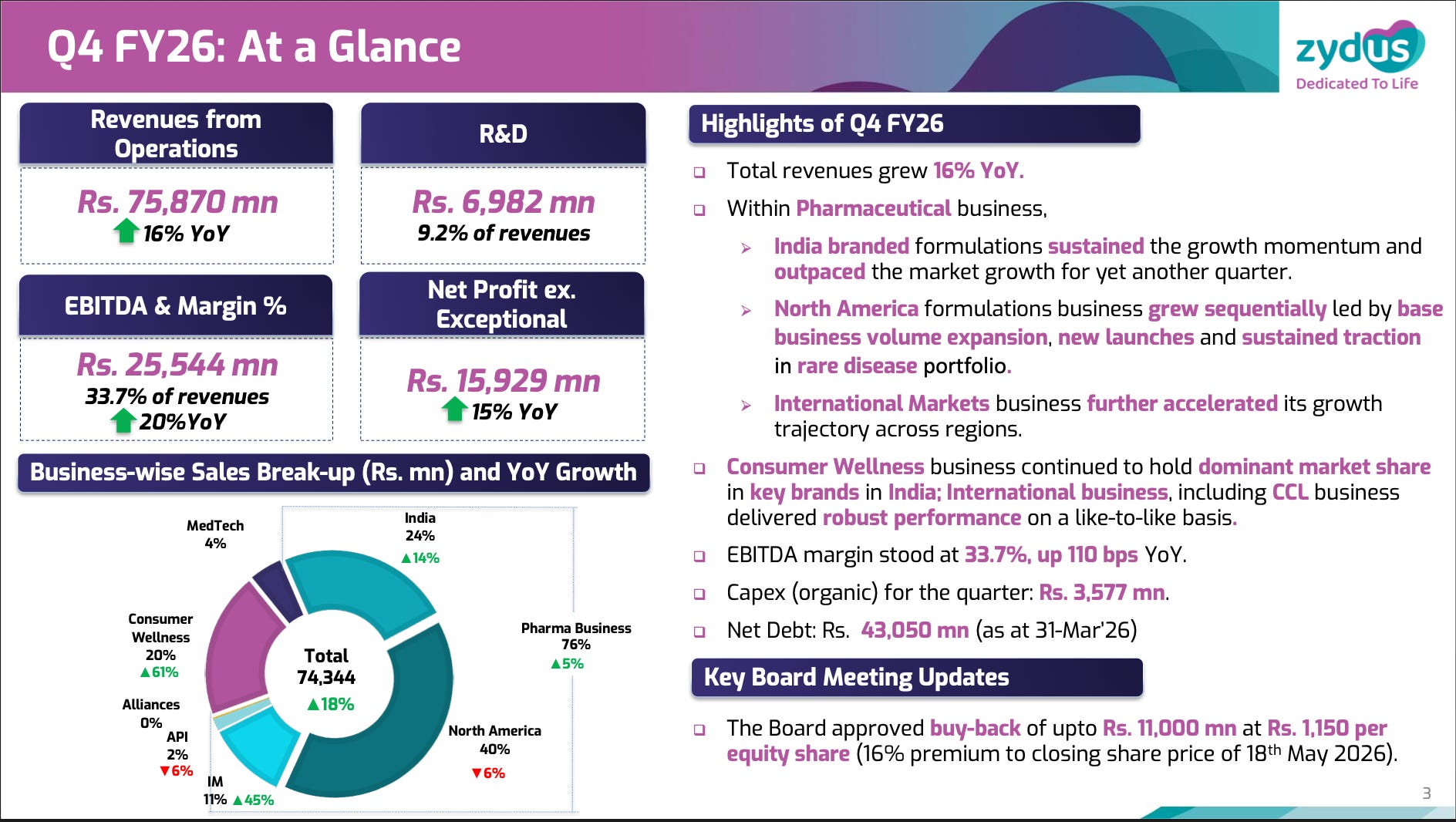

8) Zydus Lifesciences - Record Margins, Semaglutide Leadership, and a Buyback

Zydus is having arguably its best year ever. The headline is 31.2% EBITDA margin is the highest operating margin the company has recorded.

Zydus is the most aggressive player on semaglutide in India. Dr. Sharvil Patel described the co-marketing strategy: “We have launched a novel formulation on sema... together we control a very meaningful part of the market share on semaglutide... we are now number two in terms of share, and closely followed by Lupin, and Torrent also has gained strong share.”

They have co-marketing agreements with both Lupin and Torrent for semaglutide, creating a multi-pronged market coverage strategy. The company also filed an NDA for semaglutide in the US, a potentially massive long-term opportunity.

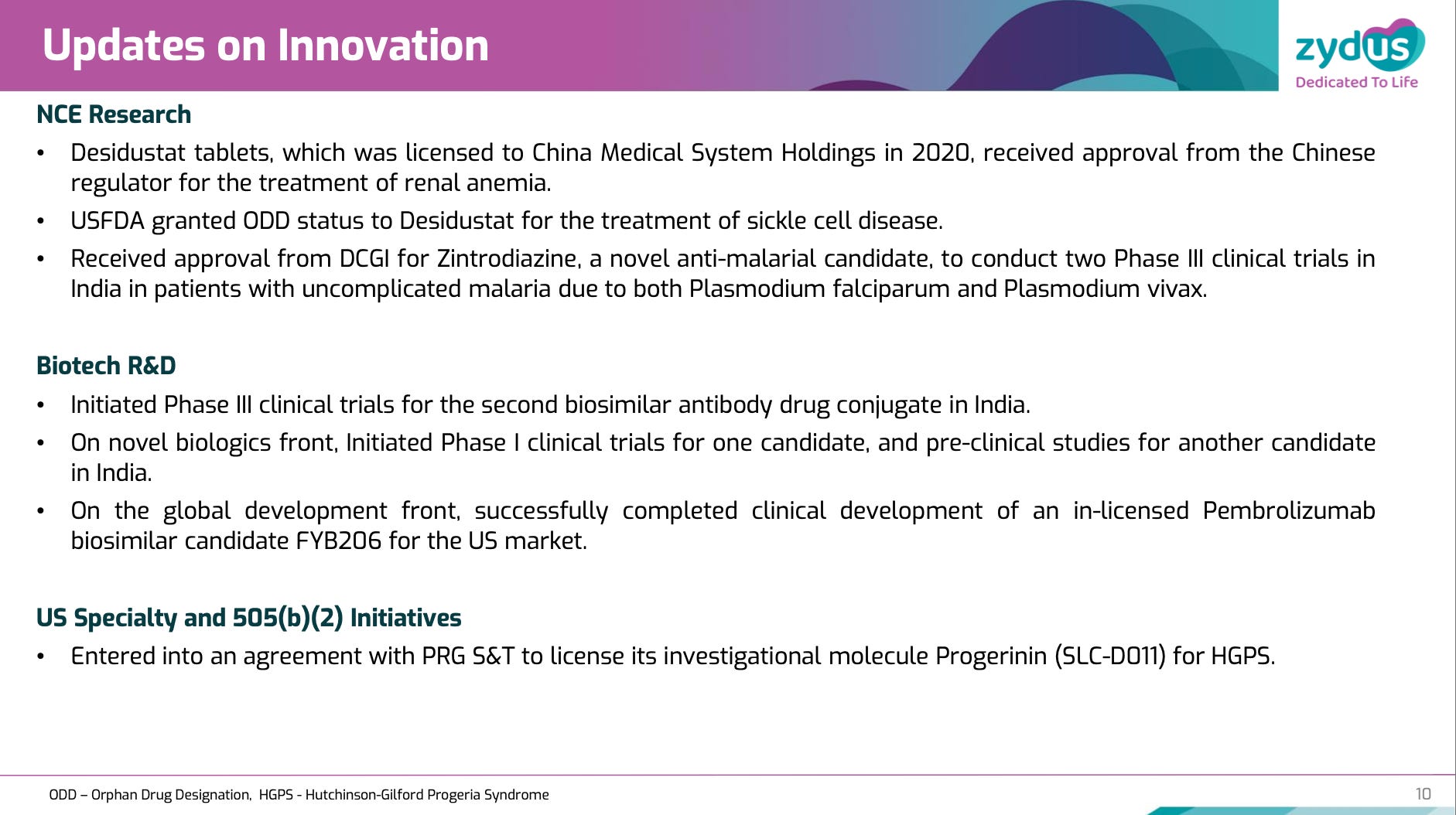

Innovation Pipeline - Beyond Generics: Zydus’s innovation engine continues to deliver milestones:

Desidustat: Approved in China for renal anemia

Nivolumab biosimilar (Tishtha): World’s first nivolumab biosimilar, launched in India

Pembrolizumab biosimilar: Clinical development completed

Saroglitazar: Pre-launch activities for US entry in PBC indication

Assertio acquisition: US acquisition for oncology supportive care portfolio

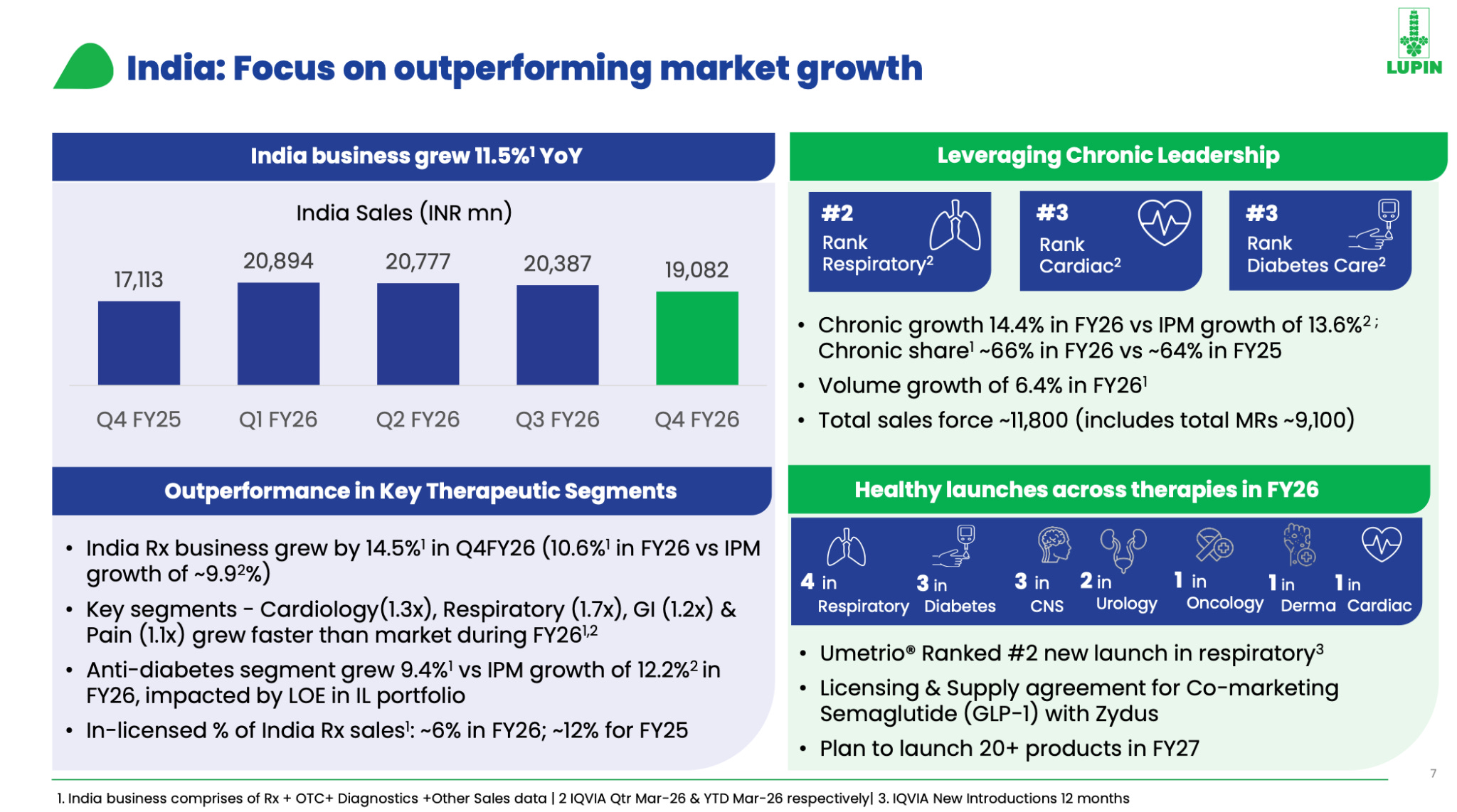

9) Lupin - 15 Consecutive Quarters of Growth

Lupin’s domestic performance is a masterclass in portfolio engineering. The company has deliberately built depth in chronic therapies → cardiac (#3 rank), respiratory (#2), diabetes care (#3) while maintaining volume growth at 6.4% in FY26.

The India strategy is evolving on multiple fronts simultaneously:

Semaglutide: Licensed and co-marketed with Zydus, with a dedicated division spanning diabetology/endocrinology and gastroenterology/gynecology

Chronic target: ~70% chronic share by FY31, up from 66% today

Nebulization Task Force: New initiative to strengthen the respiratory portfolio

Extra-Urban (Uday): Division expansion for deeper penetration in semi-urban and rural markets

20+ product launches planned for FY27

What makes Lupin’s India story particularly interesting is the combination of scale and growth rate at 1900+ cr quarterly revenue, still growing 12-14.5%, with 1.2-1.3x IPM outperformance guided for FY27.

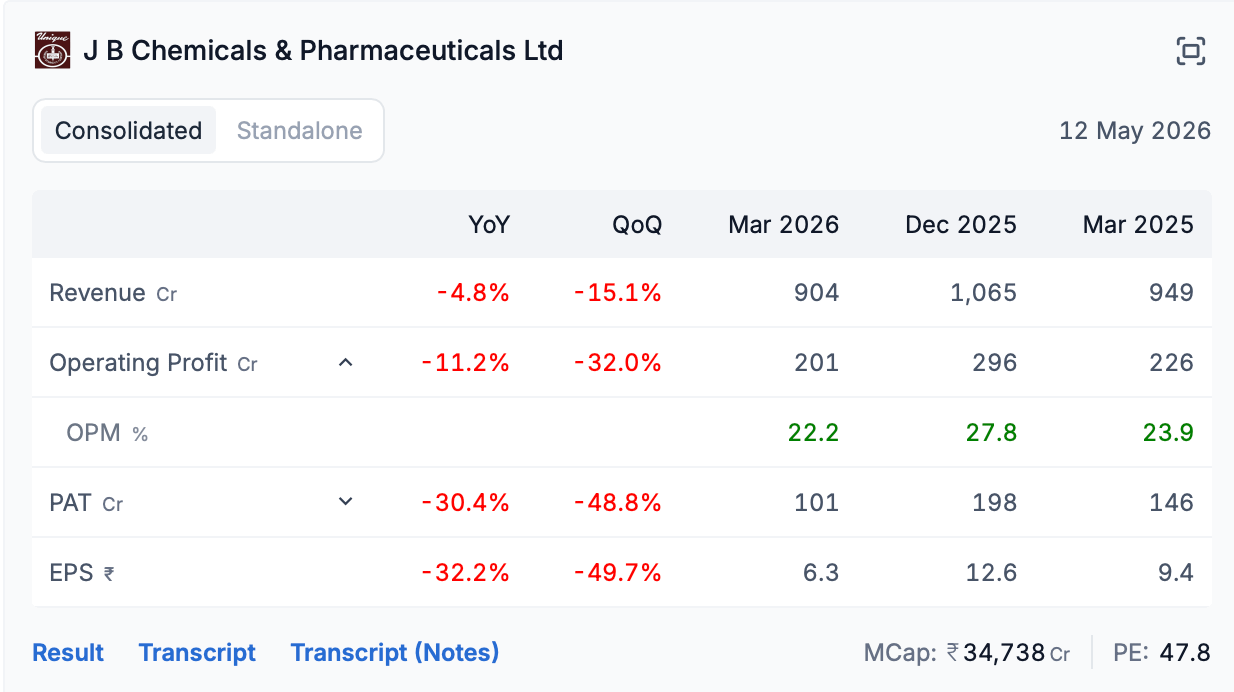

10) JB Chemicals - A Transition Quarter, Torrent Integration Reset

JB Chemicals’ Q4 was a transition quarter following the Torrent Pharma integration reset. The company’s core branded business grew 8%, but the deliberate discontinuation of the trade generics business created a headline drag. The full-year picture reflects a company in the midst of recalibrating its portfolio toward higher-margin branded segments while absorbing the operational complexity of integration.

This is a name to revisit in FY27 when the base effects normalize and the combined entity’s true growth trajectory becomes visible.

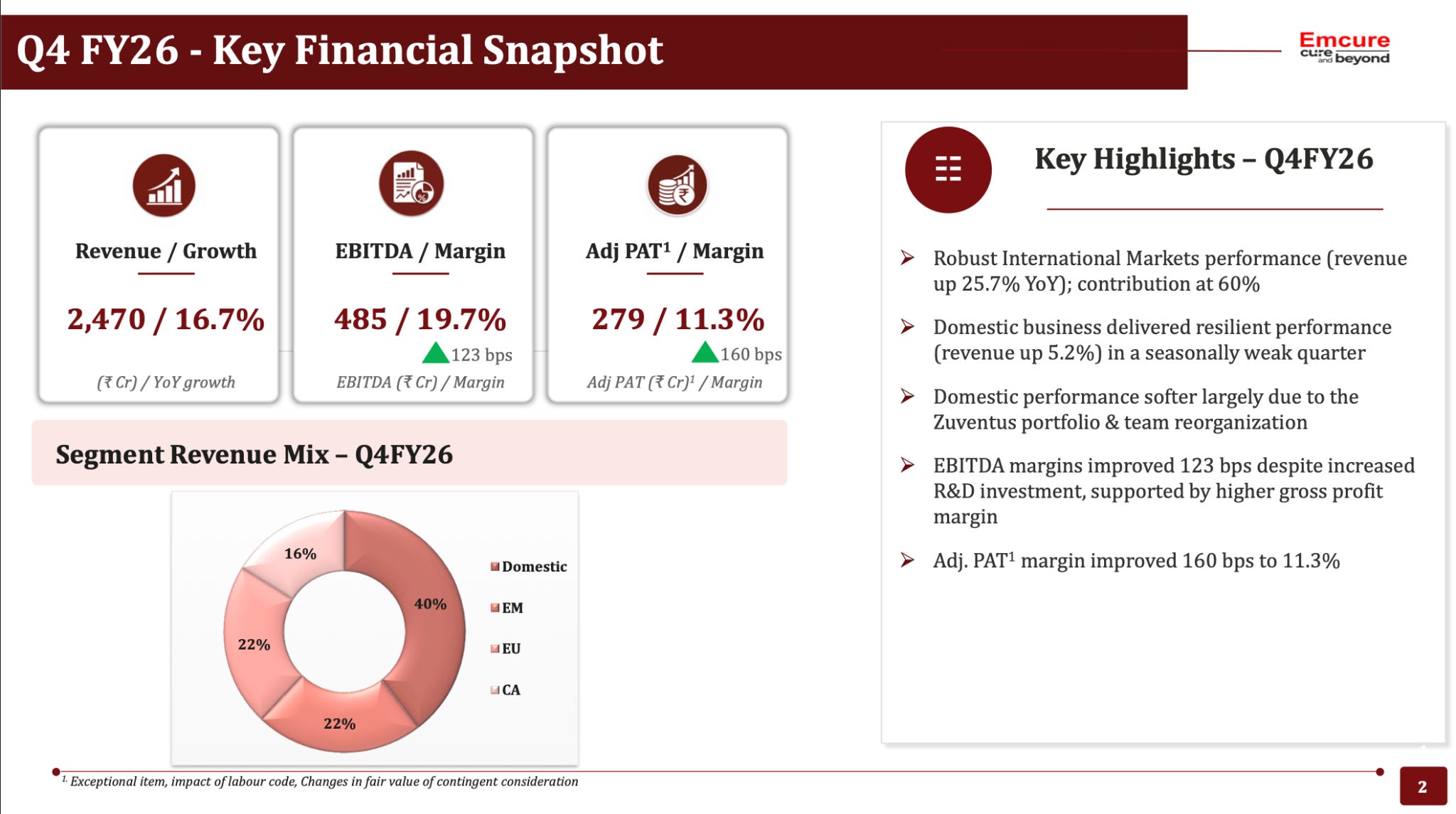

11) Emcure Pharmaceuticals - Quietly Crossing the $1 Billion Mark

Emcure crossed $1 billion in revenue for the first time in FY26, a significant milestone for a company that has been building a diversified formulations business across India and international markets. Domestic grew ~10%, while international was the standout at +22%.

The more interesting aspect is Emcure’s partnership strategy. The company has supply agreements with Novo Nordisk, Sanofi, and Roche for marketing their patented products in India, a model that provides premium product access without the R&D risk. This positions Emcure as a distributor of global innovation in the Indian market, a differentiated approach versus the typical generic-first model.

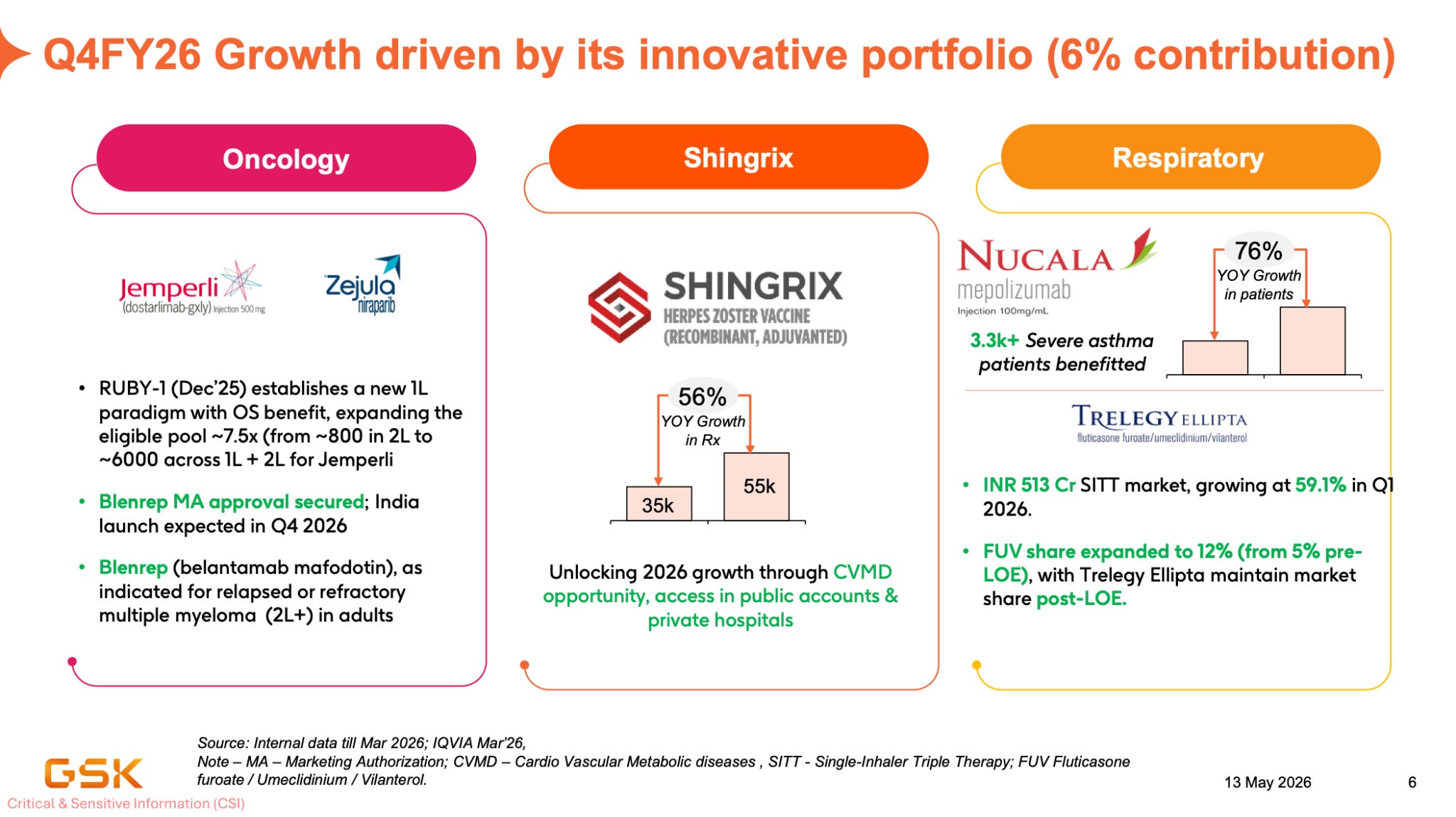

12) GSK Pharma India - Innovation-Led, But Growth Remains Patchy

Mixed performance - promoted brands (Augmentin, Calpol) grew 3-4 pp above market; distributed portfolio underperformed Key Highlights: Shingrix (adult shingles vaccine) continued double-digit growth; oncology launches (Zejula, Jemperli) building base; ~6% of topline from innovation portfolio

GSK India’s story is fundamentally different from domestic Indian pharma companies. It’s a subsidiary of a global innovator, and its growth depends on the pace at which GSK’s innovation portfolio is launched in India. MD Bhushan Akshikar articulated the priority: “Unlocking value of our innovation portfolio, especially in key markets like India, to accelerate the launch of innovative medicines and vaccines with accelerated timelines as well as reducing the launch lag.”

The innovation freshness index is at 6% of topline, targeting 10%. The specialty builds in respiratory (Trelegy Ellipta, Nucala) and oncology (Zejula, Jemperli with Ruby-1 approval) are encouraging but still small in absolute terms.

With this lets see how ROW Formulators have performed?

International formulations outside the US selling to markets across Latin America, Africa, Southeast Asia, the Middle East, and Eastern Europe have quietly emerged as one of the most attractive sub-segments in Indian pharma.

The reasons are simple -

1) Less price erosion than US generics many ROW markets operate on tender-based or branded-generic models with less competitive intensity

2) Higher entry barriers than domestic Indiarequires regulatory filings (EU GMP, WHO PQ, ANVISA), distribution infrastructure, and local market knowledge

3) Branded potential - unlike the US where generics are interchangeable, many ROW markets allow branded generics that can command premium pricing

4) Large unmet need - healthcare access in Africa, LatAm, and Southeast Asia is expanding, creating genuine volume growth (not just market share battles)

Lets see who is doing well here -

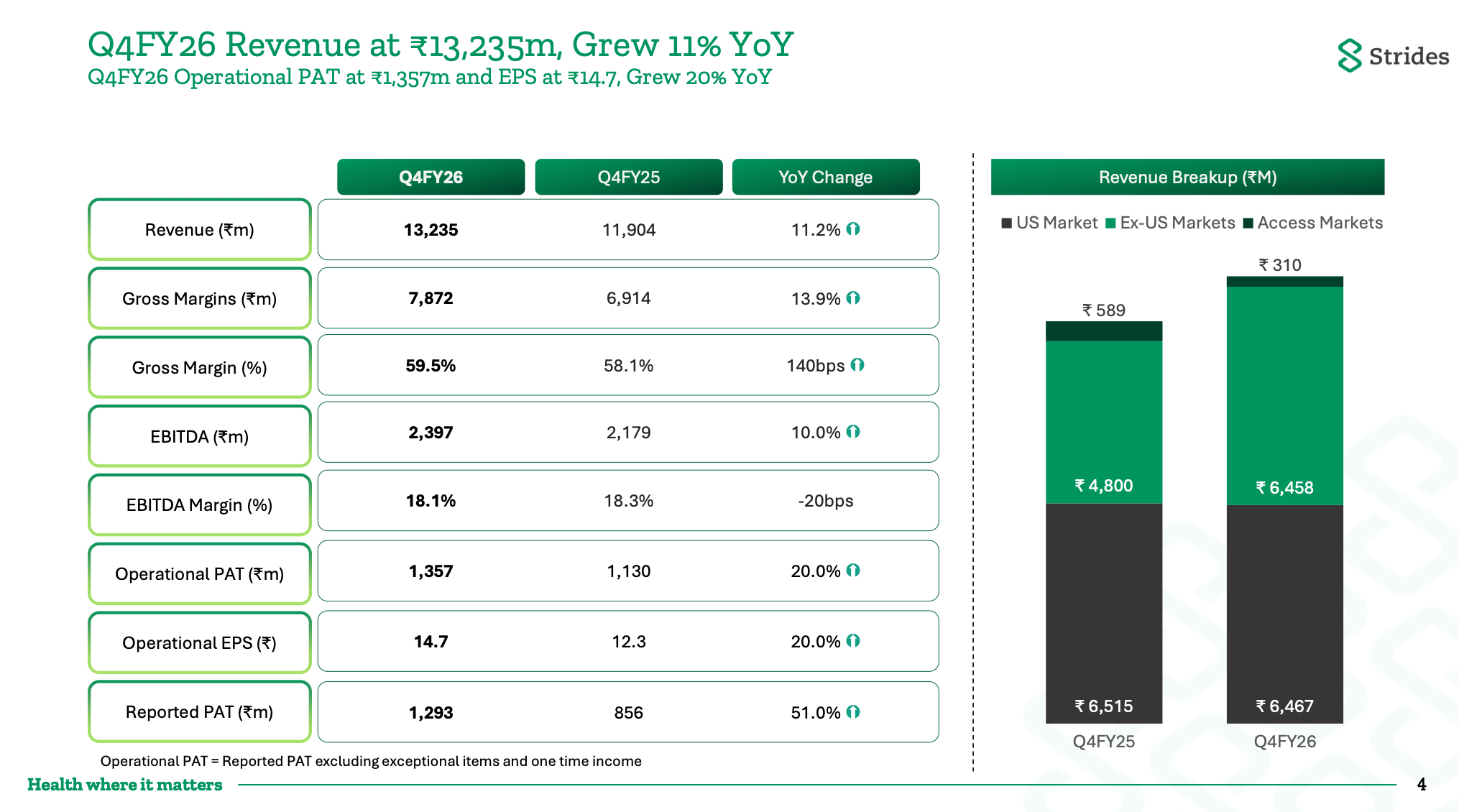

13) Strides Pharma - The Ex-US Transformation Story + Controlled drug substances

Strides’ transformation from a US-centric generics player to a diversified international formulator is one of the most underappreciated stories in Indian pharma. Ex-US markets now account for ~50% of revenue and are growing at a 19% CAGR over 3 years, compared to the US business which has been volatile.

MD Badree Komandur captured the strategy: “Profitability has been the cornerstone of our transformation journey... EBITDA has compounded at approximately 26% over the last 3 years, driven by EBITDA margin expansion of 400 basis points.”

The Africa strategy is particularly noteworthy Strides acquired Sandoz’s sub-Saharan portfolio, gaining established brands and distribution in a market with enormous unmet healthcare needs. Gross margins at 59.7% reflect the branded/tender mix in these markets, structurally above US generics.

In their US business controlled drug substance can be an interesting story. 4 products launched from Chestnut Ridge ANDAs. Only 18-19 months of operating history. Have now completed one full year, gone back to DEA requesting additional quota. Timing of quota approval is uncertain but they’ve formally applied. As this approval process gets underway US business can also start to contribute to growth. Management is guiding for growth in US business which went out to be flat in Fy26

With this scale up in ROW and inflection back in US business in FY27 with levers for margins to expand while the company can also go net cash BS in next 2-3 years. Triggers seem to be in place to at least keep this one in your watchlist.

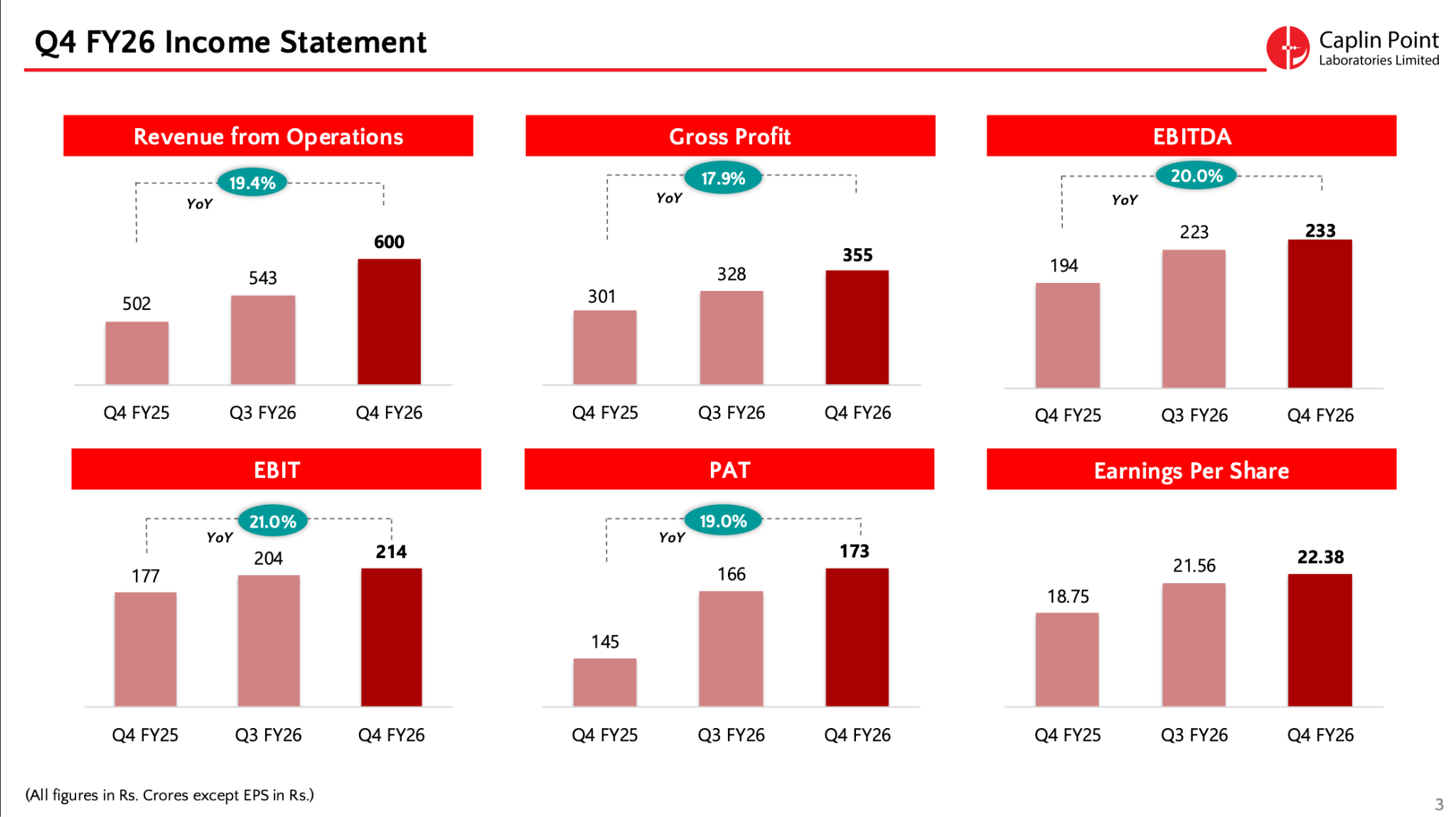

14) Caplin Point - The Latin America Deep Moat

Caplin Point is perhaps the most unique formulation story in Indian pharma. The company has built a Latin American empire over 20+ years by keeping inventory in local subsidiary warehouses, a model that provides both customer stickiness and supply chain resilience that few competitors can match.

Chairman C.C. Paarthipan described the moat: “Our model of keeping the goods next to the customer in the last 20 years has produced this compounding effect. Hence, we always keep the goods in our subsidiary warehouses for a minimum of 6 months’ stock.”

The numbers are striking: 135 registrations in Chile, tenders won in Mexico, 41% shelf space in Central American markets. This kind of entrenched distribution creates a competitive moat that’s nearly impossible to replicate quickly.

The US business with 60 ANDAs, 10 approvals in FY26, and EBITDA margins mirroring the parent at ~30% adds optionality but isn’t the core thesis. Caplin Point is a LatAm story, and the LatAm story is compounding beautifully.

15) Kwality Pharma - The Small-Cap ROW Rocket

Kwality Pharma is the kind of small-cap story that gets investors excited, a 503 Cr revenue company growing at 36%, guiding 650 Cr next year and 1,000 Cr by FY29, with an EU GMP-approved manufacturing base (4 out of 5 units cleared) and a fast-expanding oncology portfolio.

The margin profile is differentiated by product type:

Oncology: 100 Cr revenue at 30-32% EBITDA margins (looking this to grow 3x)

Peptides: 40% EBITDA margins- the highest-margin segment

Overall: Growing rapidly while maintaining blended margins in the high teens

The company is filing extensively in regulated markets (EU GMP, ANVISA) and building branded positions in semi-regulated markets. At 503 Cr, the base is small enough that even a few successful product launches can move the needle materially. The FY27 guidance of 650 Cr (+29%) and 100 Cr PAT (+49%) suggests management sees clear visibility.

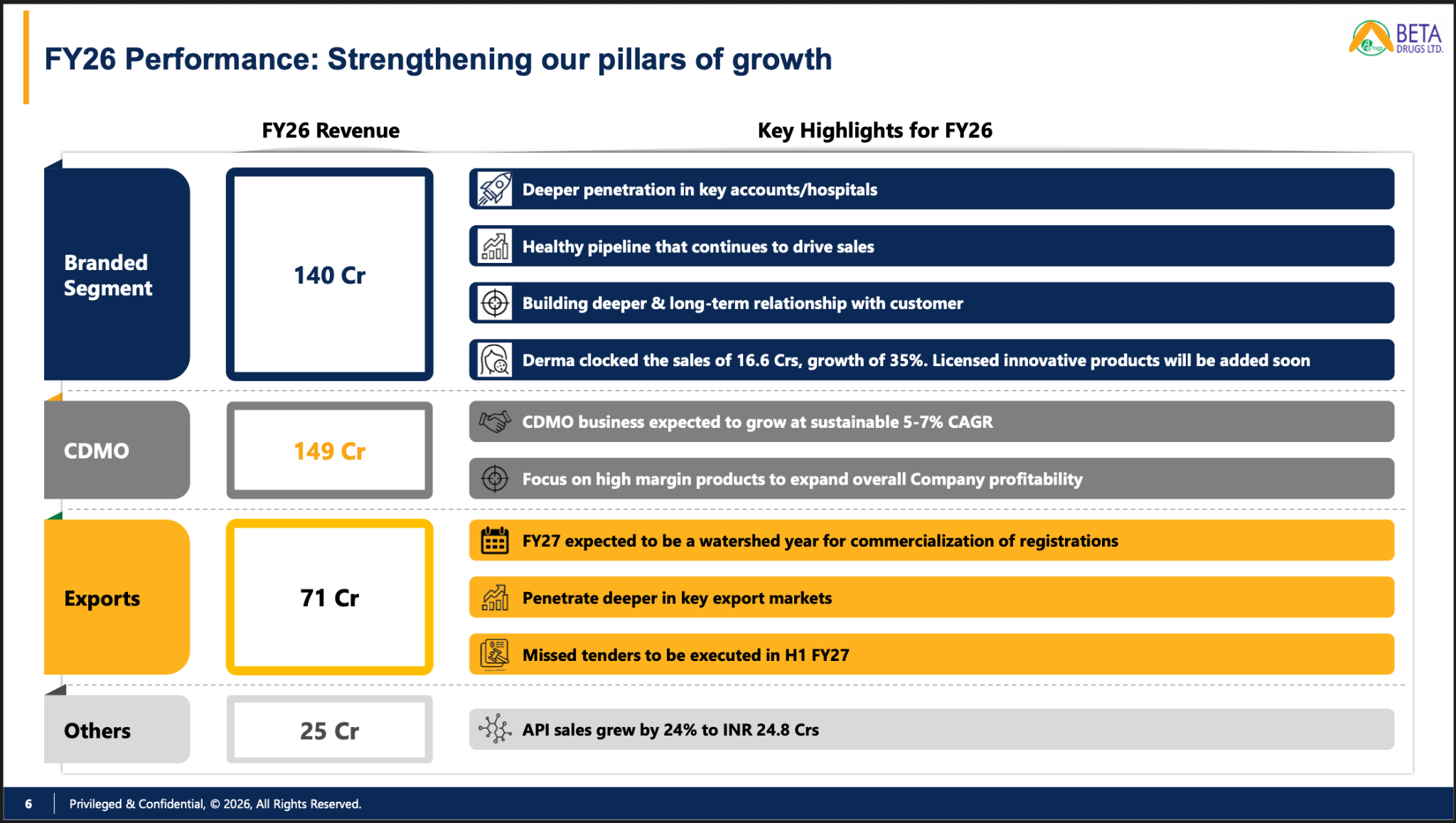

16) Beta Drugs - The Oncology Specialist with Export Ambitions

Beta Drugs is a niche oncology-focused formulator that had a mixed FY26:- branded oncology grew 20%, but exports declined 11% due to tender delays.

MD Rahul Batra was candid: “We accept that the growth expected last year was not encouraging for the entire company.”

Reasons for the bad performance this year was 1) company stopped platin sales as the raw material prices ran up but domestic prices were not revised and it became unviable to make sell this and 2) Due to audits their facilities were shut for a few days in multiple quarters so that hampered the operations in CDMO.

The forward story is more interesting:

200+ dossier submissions in the last 18 months, with ~100 new registrations expected this year

EU audit scheduled for September 2026 (3 dossiers filed)

Export target: 30% of revenue by FY30

Nibvin acquisition (IVF/fertility business, 69 Cr for 66.1% stake) — adds a second super-specialty vertical growing at 30%+

API backward integration: In-house KSM manufacturing to reduce import dependence

The PIC/S approval for the API plant is a notable regulatory milestone that opens doors for export markets. If the delayed tenders (awarded March 2026) start reflecting from Q1 FY27 as guided, the export business alone could drive significant topline acceleration.

The dermatology segment is also growing really well for them in domestic formulations where they have gone breakeven and as the revenue scales their margins can further improve their.

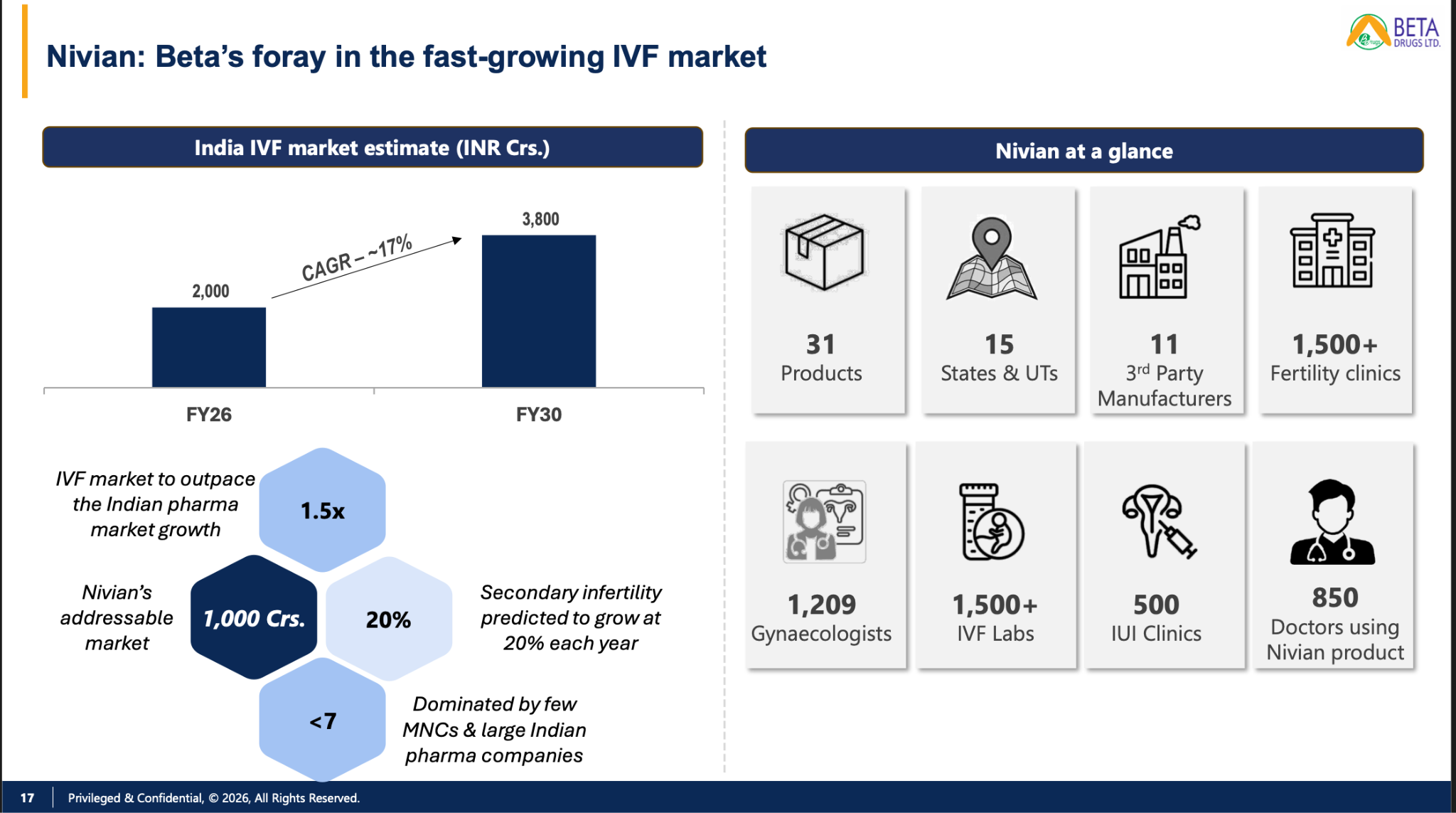

Also diversifying out of oncology in domestic business they have recently acquired Nivian lifesciences (a company formed by the founders of BSV - yes the same company that mankind acquired). Interestingly founders of the company have not exited or diluted anything in this acquisition and are involved operationally. This company is in IVF formulations which again is a niche in IPM which is growing at 17%. This business can scale really well in the coming 2-3 years and is a key development that one should watch.

Now let’s decode what’s happening in US formulation ?

The US generics market is no longer the commodity business it was a decade ago. Indian companies have systematically moved up the complexity curve, and Q4 FY26 results show that this shift is now generating premium economics.

The new playbook involves:

Complex generics: Injectables, respiratory/nasal sprays, ophthalmic, transdermal products with technical barriers that limit competition

Controlled substances: A sub-theme gaining momentum at Strides through its Chestnut Ridge facility and DEA quota

Biosimilars: The next major wave is pembrolizumab, bevacizumab, ranibizumab, trastuzumab

505(b)(2) specialty: Branded differentiated products filed through the 505(b)(2) pathway (Alembic’s PIVYA)

Peptides: Semaglutide filings by Zydus and Lupin as the frontier opportunity

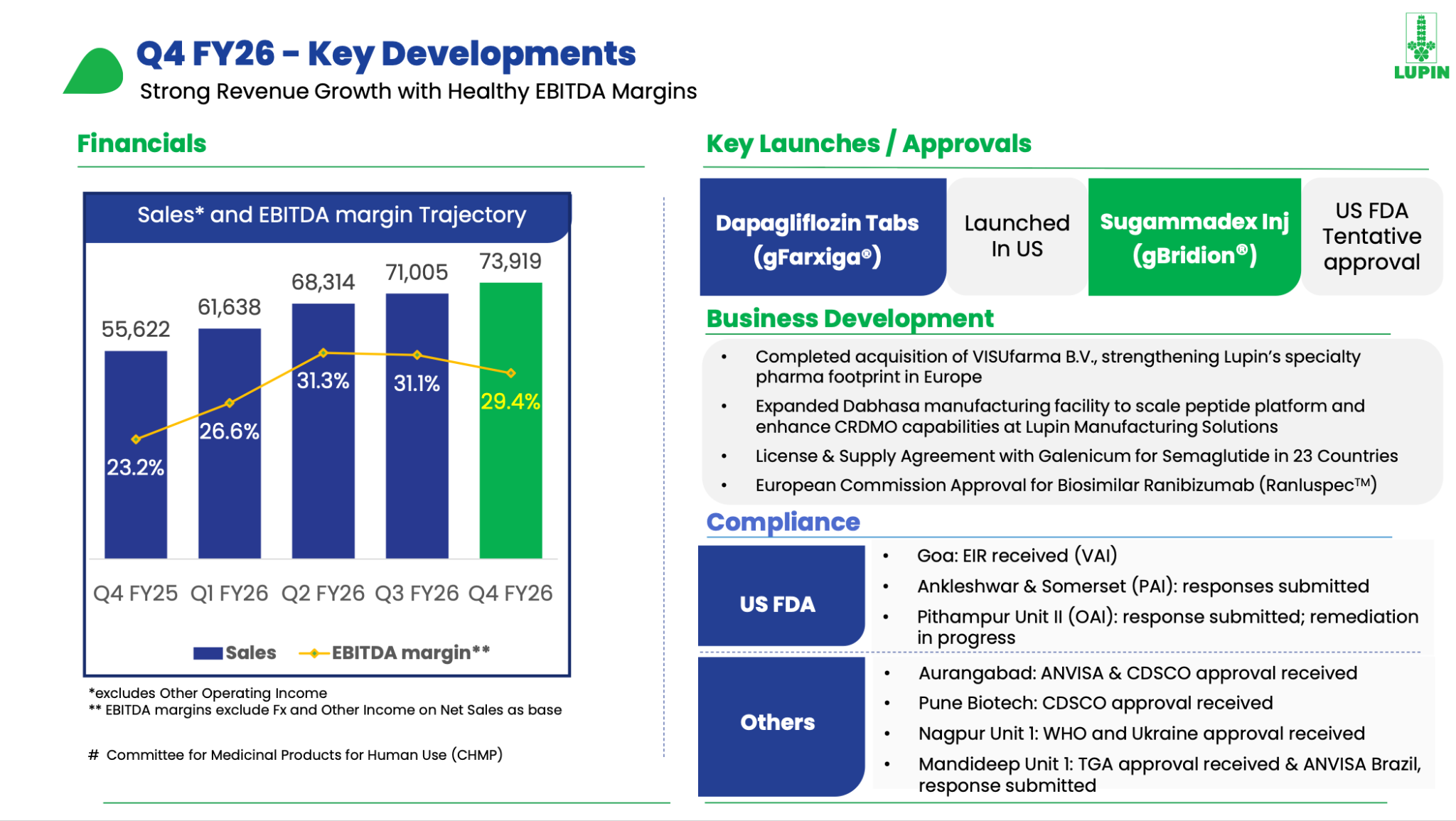

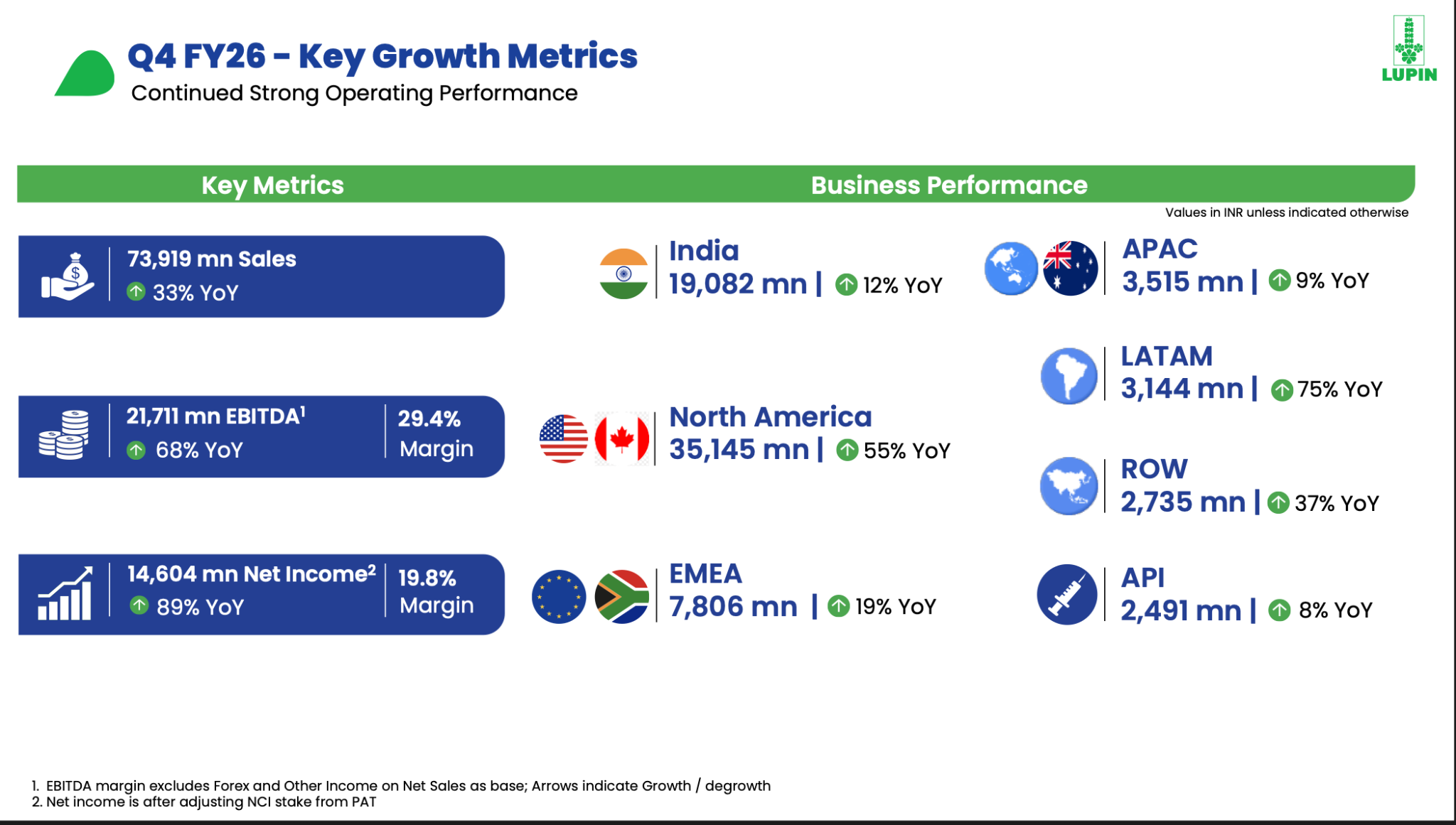

17) Lupin US - $1.3 Billion and Still Accelerating

FY26 US: ~$1.3 Bn (+~40% YoY) | Q4 US: 33,987 Mn ($371 Mn, +55% YoY)

Lupin’s US performance is the headline story of Q4 FY26. The business recorded its highest-ever quarterly sale at $371 Mn, with the full-year US business at approximately $1.3 billion, an extraordinary ~40% growth rate for a business of this scale.

The growth is driven by key product launches (Tolvaptan exclusivity, Mirabegron, Dapagliflozin, Sugammadex injection) and a deliberate strategy to increase complexity. CEO Vinita Gupta stated: “FY26 has been a stellar year for the organization, with revenues and profitability at record levels.”

The pipeline visibility is equally strong having 50+ products to launch in the next 3 years, including 10 exclusive FTFs. The company plans to “double the share of complex products in our US business led by respiratory and complex injectables augmented by our biosimilars.”

The VISUfarma acquisition in Europe, Galenicum semaglutide license (covering 23 countries), and biosimilar ranibizumab EU approval all add geographic and product diversification.

18) Zydus US - $1.3 Billion Franchise, Innovation-Led Optionality

FY26 North America: ~$1.3 Bn range | Semaglutide NDA filed | Assertio acquisition completed

Zydus’s US franchise matches Lupin in scale at ~$1.3 Bn. The near-term headwind is mirabegron competition, with management guiding single-digit US growth for FY27. But the optionality is significant:

Semaglutide NDA: Filed in the US if approved, this could be transformative

Assertio acquisition: Oncology supportive care portfolio for US branded presence

Biosimilars: World’s first nivolumab biosimilar (Tishtha) launched; pembrolizumab in development

Buyback: 6,000 Cr at 1,150/share signals management confidence in long-term value

19) Cipla US - Crossing $400 Mn Quarterly, Ventolin CGT Milestone

FY26 US: ~$780 Mn | First AB-rated generic Ventolin with CGT approval

Cipla’s US business has been built methodically on respiratory leadership (inhaler franchise), and the generic Ventolin approval with Comparative Bioequivalence Study/CGT represents a significant competitive moat; this is a technically complex product with limited competition.

However, the broader Cipla story in FY26 is one of margin compression where EBITDA margin fell from 25.9% to 21%, driven by higher R&D spending and competitive dynamics in some product categories. The US revenue is growing, but the profitability trajectory needs watching.

20) Dr. Reddy’s - Base Business Growth Masked by Lenalidomide SSA

FY26: Revenue 33,593 Cr (+6%) | EBITDA Margin 22.8% | Lenalidomide SSA impact: 453 Cr

Dr. Reddy’s headline growth looks muted at 6%, but this masks two offsetting forces. The base business delivered double-digit growth, while a 453 Cr shared savings adjustment (SSA) on lenalidomide (post patent expiry, pricing collapsed as competition entered) dragged down reported numbers.

The other notable development was a CAR-T impairment, signaling challenges in the cell therapy ambitions. The NRT (nicotine replacement therapy) business acquisition is contributing, and the company continues to build its biosimilar and specialty pipeline.

21) Biocon - Biosimilars Coming of Age

FY26: Revenue 16,927 Cr (+13%) | Biosimilars 10,431 Cr (+16%) | Q4 Biosimilar EBITDA Margin 26%

Biocon’s biosimilar franchise has reached a scale and profitability that vindicates years of investment. At 10,431 Cr, the biosimilars business alone is larger than many listed pharma companies. Yesintek (bevacizumab) is a market leader in US biosimilars, and Q4 EBITDA margin of 26% demonstrates that the investment phase is largely behind.

The forward pipeline includes trastuzumab, adalimumab, and novel biologics/ADCs — represents the next growth wave. The key debate is whether Biocon can sustain the margin improvement trajectory as newer biosimilars face more competition.

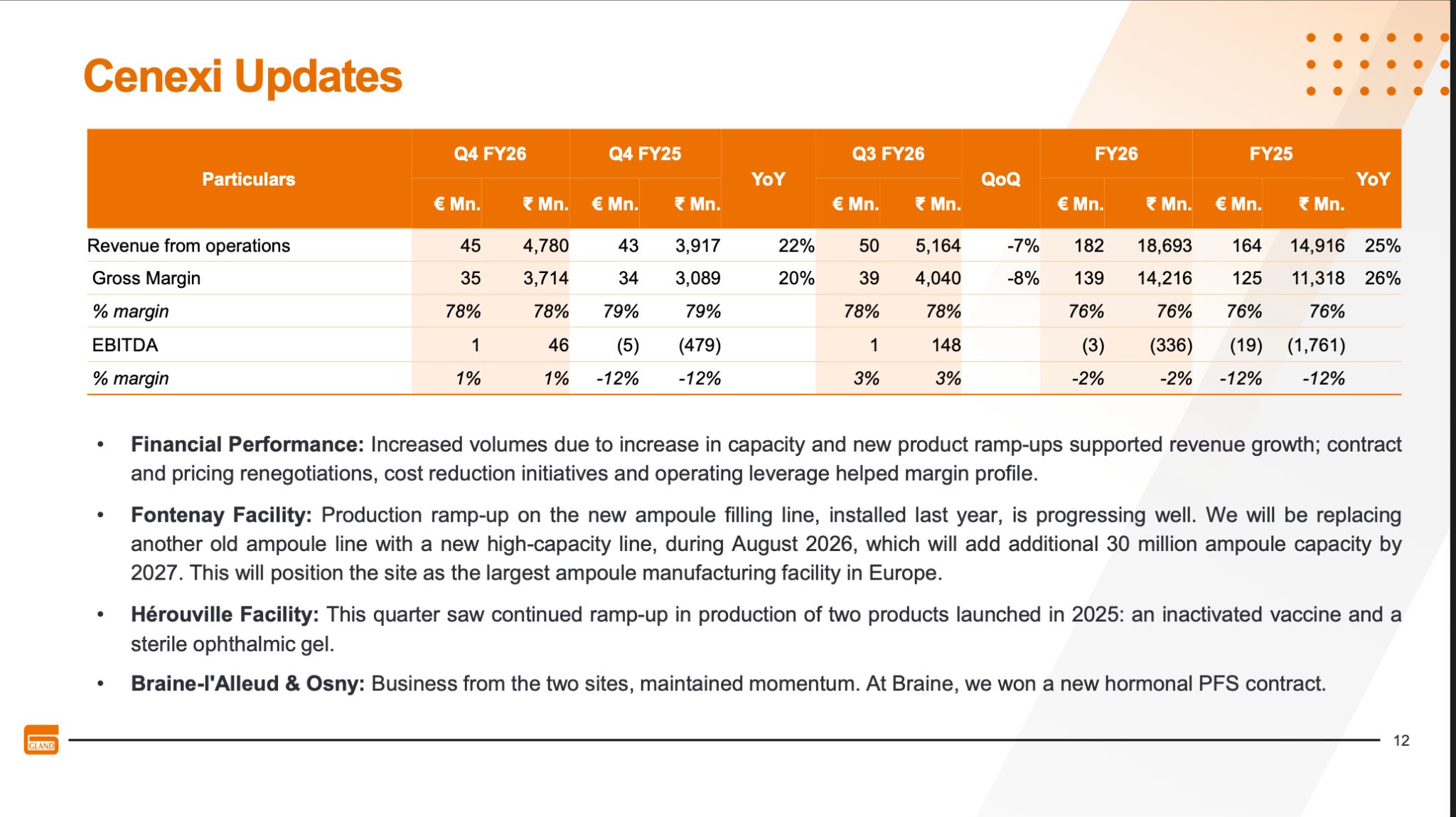

22) Gland Pharma - The Injectable Specialist

FY26 Data: Injectable-focused US and ROW strategy

Gland Pharma operates as a pure-play injectable formulations company with a focused strategy that benefits from the technical barriers and limited competition in sterile injectables. The Shanghai Fosun parentage provides access to Chinese markets while the India operations serve the US, EU, and ROW markets. The company has been expanding its CDMO offerings alongside its own product portfolio.

Interestingly here a big overhang of one of its acquisitions not doing well seems to be going away where Cenexi from this qtr is showing signs of turning back for them. Where this has been a real drag on margins from the last 3 years where base business does excellent margins were not reflecting in the consol results. Just like in this qtr on a standalone basis the company did ~40% margins but on consol ~29%.

After a long time there are a lot of earning upgrades there. This seems to be the business that fits into framework of growth and margins coming back of a good quality business which at the least should not be ignored

The US business for Indian pharma companies in Q4 FY26 is defined by three interesting shifts:

a) Complexity is the new competitive weapon

b) Biosimilars are becoming real revenue contributors

c) The semaglutide NDA/ANDA race

Indian pharma’s US business has permanently graduated from har-ghar generics yojana at declining prices to complex, differentiated products at stable-to-improving economics.”

Before we move on,

If this deep dive is the kind of analysis that gets your investing brain firing, there’s more where this came from. This Sunday (24th May, 1 PM onwards), we’re running the same playbook across multiple sectors breaking down the most explosive Q4 FY26 earnings, identifying the themes that matter, and mapping where the real opportunities are hiding in plain sight.

Think of it as your cheat code to stay on top of results season without reading 200 concalls yourself.

With this let’s move to another section that is CDMO (The Thekedars of Pharma Universe)

Here are a few simple tailwinds that are there in this segment that are driving strong growth..

1) China+1 is real

2) The innovator outsourcing trend is deepening

3) Patent cliffs are creating massive demand

4) New modalities (peptides, ADCs, oligonucleotides) require specialized capabilities

These tailwinds are specifically for patented CDMO space. With this let’s understand what is happening in the players in this space -

PATENTED / INNOVATOR CDMO (CRDMO) - Where the Real Re-Rating Is Happening

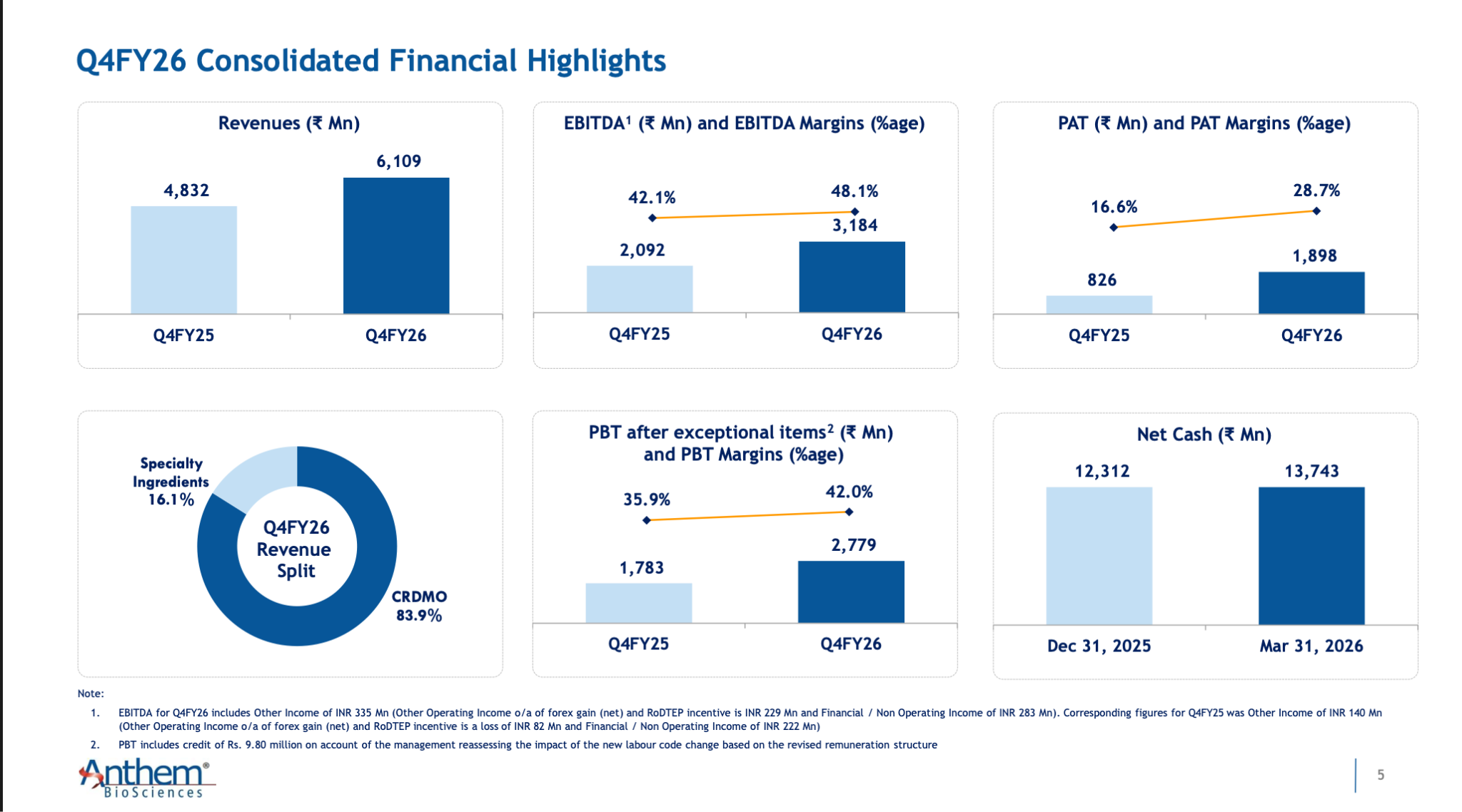

23) Anthem Biosciences (formerly Dishman) - The Quiet Powerhouse

If Neuland Labs had the most impressive single quarter in API/CMS, Anthem Biosciences had the most impressive full-year performance in CDMO. A 43.4% EBITDA margin for the full year expanding to 48.1% in Q4 is extraordinary by any standard, globally.

MD and CEO Ajay Bharadwaj was measured in his commentary but the numbers speak for themselves: “Our EBITDA and PAT for the year grew by more than 30%, in line with our growth aspirations. We continue to maintain a healthy financial position and remain committed to delivering sustainable growth across all business segments.”

The CRDMO business (83% of revenue) is anchored by commercial molecules and a growing pipeline of late-stage programs. The company works with 3 of the top 20 Big Pharma companies and added 2 more direct relationships in FY26. Ten programs in Phase 3 with small biotechs provide a pipeline of potential future commercial molecules

When asked about growth trajectory, management referenced the company’s 10-year track record: “Historically, if you look at the last 10 years, our revenue growth has been around the 20% level... Our aspirations are quite high. We are investing in people, facilities, and technology, and all of this is also seen by our customers.”

Unit 2 expansion added ~50% reactor volume (270 KL to 376 KL), Unit 3 is fully operational, and Unit 4 is being planned as a future-readiness investment.

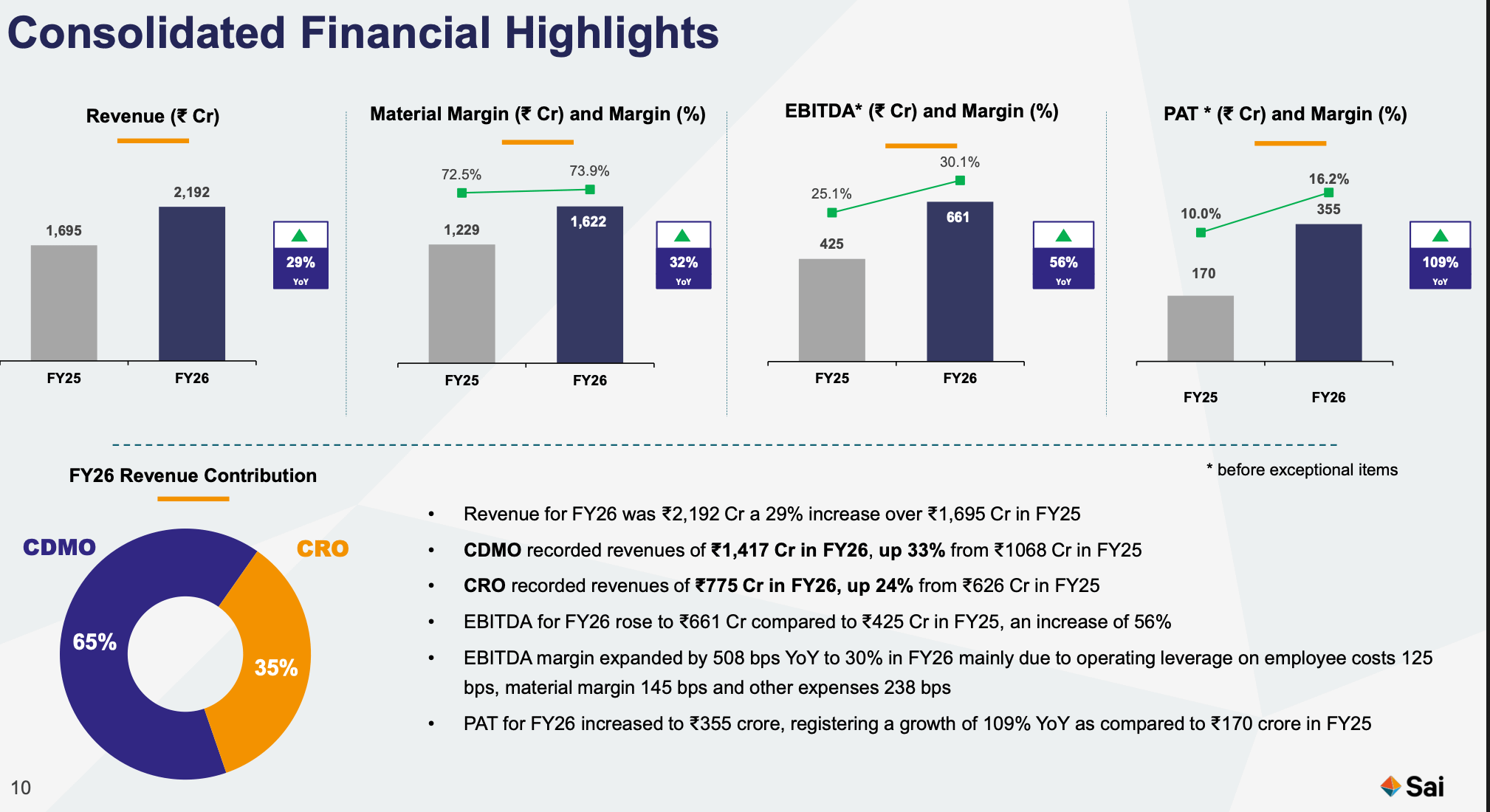

24) Sai Life Sciences - Doubling Down on Large Pharma, Massive Capex Ahead

Sai Life Sciences is in full investment mode. The FY26 financial performance - 29% revenue growth, 56% EBITDA growth, 109% PAT growth is impressive. But it’s the FY27 capex guidance that tells you where the company is headed: 1,100-1,300 Cr in capital investment, nearly doubling from the ₹633 Cr spent in FY26. That’s an enormous bet on future growth.

And historically this management has not done capex until they have strong visibility of growth

CEO Krishna Kanumuri was deliberate in framing this as demand-driven, not speculative: “These investments are being undertaken either with clear demand visibility or through active strategic conversations with our large pharma customers.”

The guidance for FY27 is measured: 15-20% revenue growth, 28-30% EBITDA margins, with H2 expected to be stronger than H1 as new capacities come online. Customer concentration is manageable - top 10 at 54%, top 5 at 37%, top 1 at 12%.

Also this was the guidance that management had given in Fy26 and here is the proof point of what they have delivered. Sai Life is investing nearly 50-60% of its annual revenue in capacity expansion. This is the right move if the demand materializes. But anything on the demand side falters this can create a BS risk for the company.

If you want to understand this business in detail then here is the link for the same -

25) Syngene International - Can it finally execute ?

Syngene’s FY26 was, by its own standards, a disappointing year. Revenue growth of just 3%, EBITDA margin compression from 29% to 25%, and a leadership transition (Siddharth Mittal from Biocon appointed as new MD/CEO) make this a year of reset rather than growth.

The company completed 85 audits during the year, reflecting client engagement, and the ADC platform expansion is a strategic positive. But in a year when peers like Anthem posted 18% CRDMO growth and Sai Life grew 29%, Syngene’s 3% growth stands out as an underperformer.

The investment debate centers on whether this is a temporary blip (customer destocking, leadership transition) or a more structural challenge (competitive intensity, capacity constraints). The new leadership’s strategic direction, expected to crystallize over FY27, will be critical. Syngene’s brand, scale (3,739 Cr revenue makes it one of the largest CRDMOs), and Biocon ecosystem provide a strong foundation for recovery. But the market is right to demand evidence of growth re-acceleration before re-rating the stock.

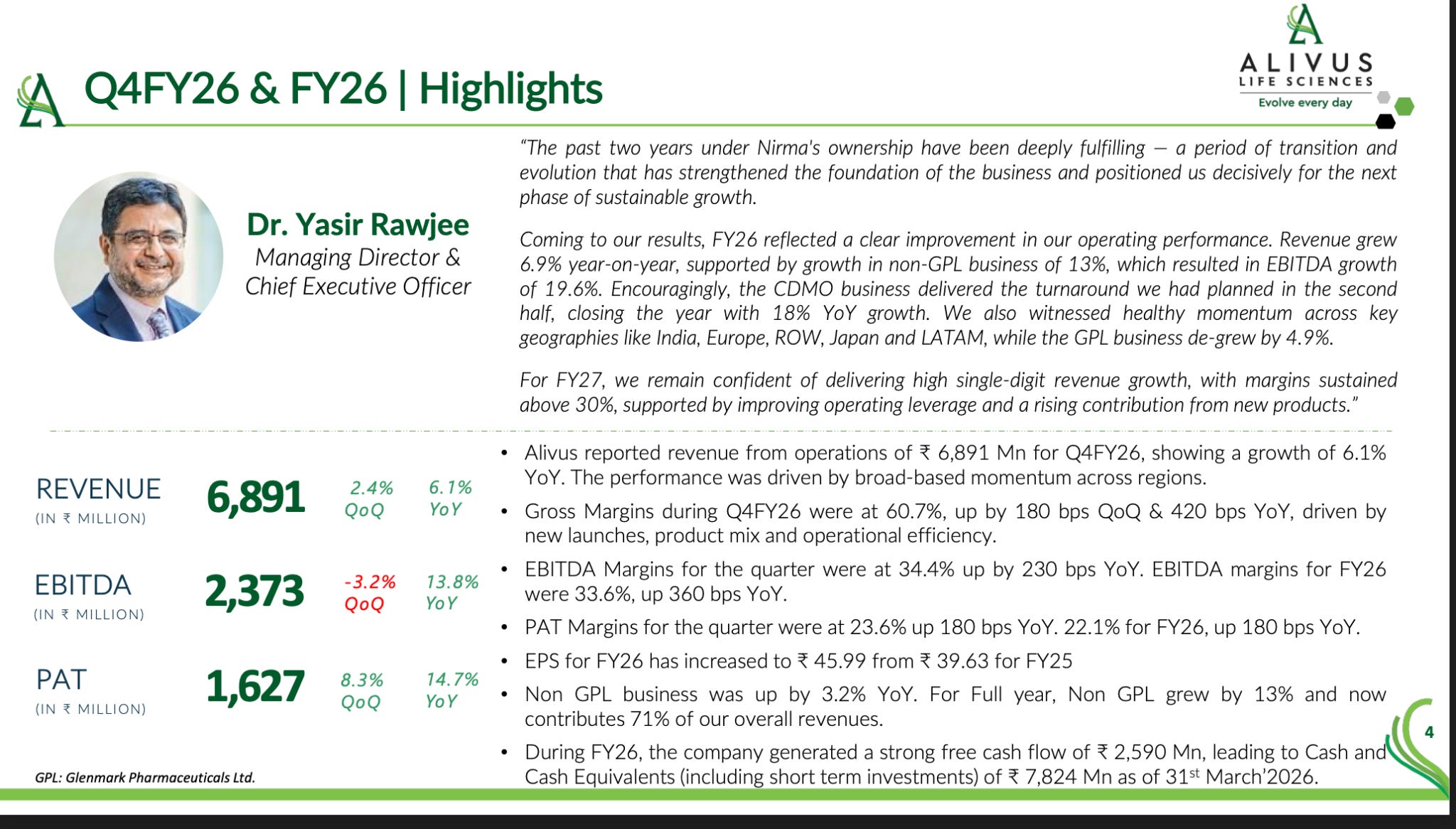

26) Alivus Life Sciences (formerly Glenmark Life Sciences) - Margin Excellence Under Nirma Ownership

Alivus (the rebranded Glenmark Life Sciences, now under Nirma promotership) delivered a masterclass in margin expansion - revenue grew 6.9%, but EBITDA grew 19.6%. The secret: a deliberate shift toward higher-value, higher-margin products in the non-GPL (non-Glenmark Pharmaceuticals) segment.

MD and CEO Dr. Yasir Raoji was transparent about the strategy: “Between FY24 to FY26, our revenue CAGR stood at 5.7% while EBITDA CAGR during the same period was 15.8%. In absolute terms, we approximately added 270 crores of incremental revenue over the last 2 years and 220 crores on the EBITDA side.”

Think about that: 270 Cr of incremental revenue generated 220 Cr of incremental EBITDA. That’s an 81% incremental EBITDA margin almost unheard of in pharma. This reflects the power of adding high-value differentiated products on a largely fixed cost base.

The portfolio has expanded to 176 unique molecules, with 611 DMF/CEP filings globally and a high-potency API pipeline of 28 products (12 validated, 7 in advanced development). The Solapur Phase 1 expansion (expected operational Q2 FY27) and a new R&D center in Taloja are the growth capex investments.

EBITDA margin guidance of 30-32% going forward is conservative relative to the 33.6% delivered in FY26 management is building in a buffer for geopolitical uncertainty and the loss of PLI benefits. The net debt-free balance sheet provides financial flexibility.

27) Cohance Lifesciences (formerly Suven Pharma) - ADC and Oligonucleotide Capability, But Execution Challenges

Cohance is the most complex and potentially most interesting CDMO story — but also the most challenging to evaluate. The company operates across three verticals (Pharma CDMO, API+, Specialty Chemicals), with cutting-edge capabilities in ADCs (antibody-drug conjugates) and oligonucleotides that very few Indian companies possess

New Executive Chairman Umang Vohra (formerly CEO of Cipla — a heavyweight appointment) signaled ambitious intent: “Having spent over three decades in this industry, I am excited to be part of a platform that is anchored in science with capabilities such as ADCs and oligonucleotides, which are well-differentiated and hard to replicate.” .

One needs to watch out the execution here with the new CEO on board.

The capabilities are genuinely differentiated:

a) ADC: Filed 3 payload DMFs in FY26, completed first cGMP bioconjugation campaign at NJ Bio (US facility), expanding with $10 Mn capex for Phase 2/validation readiness, traction in exatecan-linked platforms

b) Oligonucleotide: cGMP building block facility under validation through the Sapala platform, follow-on purchase orders received

c) Small Molecule CDMO: 140+ active projects, 70%+ from commercial products, 90%+ reload conversion rate

d) Phase 3 pipeline: 10 programs including 1 under priority review and 1 awaiting clinical data readout

However, FY26 was operationally challenging. The Pharma CDMO business was impacted by destocking in two large commercial molecules. The API+ business declined 8% due to product-specific issues and a temporary disruption at the Nacharam formulation site (~₹610 Mn revenue impact). Specialty chemicals declined marginally.

The investment thesis for Cohance comes down to a single question: can the ADC and oligonucleotide capabilities translate from pipeline to commercial revenue? If yes, Cohance could be one of the most valuable CDMO platforms in India. If the commercial molecule destocking persists and the new modalities remain early-stage, the financials will continue to underwhelm relative to peers. The Umang Vohra appointment suggests the board is serious about execution and expects a strategic blueprint by year-end.

While we discussed earlier how well in 2026 Neuland and Laurus had executed.

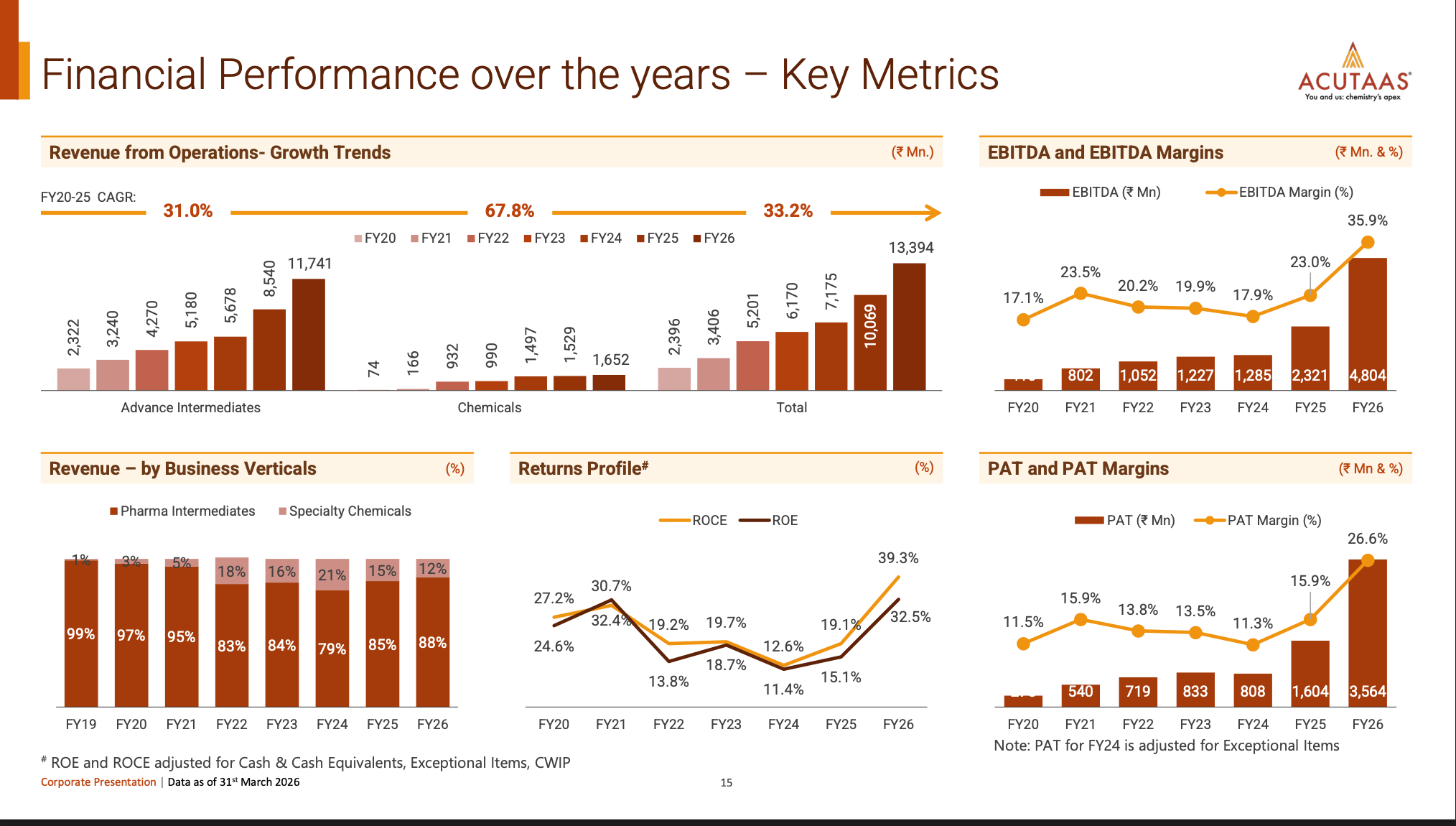

28) Acutaas Chemicals/ Navin fluorine - Driving the Bayer’s Growth

Acutaas has executed really well in FY26 driven completely by the scale up in its CDMO business driven by strong scale up in Darolutamide supplies for the company. Nubia is a blockbuster drug for Bayers and that is driving the growth for both Navin and Acutaas chemicals.

Acutaas has the target to do 1000 cr on CDMO by FY28 and Navin is guiding to do close to 2000 cr in its CDMO vertical by FY30.

Acutaas is the primary supplier for this drug and Navin is the secondary supplier for the same.

CDMO as a theme is structural but the trajectory can be lumpy -

The CDMO sector in Q4 FY26 reveals a landscape of extraordinary opportunity combined with significant execution divergence. Here’s what the earnings tell us:

1. The margin dispersion is enormous.

2. Commercial molecule revenue is THE differentiator.

3. The capex cycle is massive.

4. New modalities are the next frontier.

5. The China+1 tailwind is sector-wide but unevenly distributed.

CDMO is the most structurally attractive category in Indian pharma. The tailwinds are real, the TAM is enormous, and the entry barriers are rising.

Then there are these plays in India that are trying to be innovators themselves

NCE / INNOVATION - The Long-Duration Bets That Are Starting to Pay Off

For decades, Indian pharma was synonymous with one word: generics. Copy the molecule, scale the manufacturing, compete on cost. It worked brilliantly and built a $50 billion+ industry. But the knock was always the same: “Where’s the innovation? Where are the new drugs?”

Across the largest Indian pharma companies, innovation is no longer a PowerPoint slide labeled “optionality” — it’s showing up in revenue lines, regulatory approvals, and clinical milestones that would have been unthinkable a decade ago. Zydus has launched the world’s first nivolumab biosimilar. Biocon’s biosimilar franchise generates 10,431 Cr in annual revenue. Lupin has filed for semaglutide across 23 countries. Sun Pharma is acquiring a $6.2 billion specialty company. And Wockhardt has saved 51 lives with a novel antibiotic that’s 20% superior to existing treatments in global Phase 3 trials.

NCE/Innovation isn’t a standalone category of companies in the way that API or CDMO is. Rather, it’s a business segment within larger companies - Zydus still derives the majority of its revenue from generics, Biocon from biosimilars of existing drugs, Lupin from its branded and US generic businesses. But the innovation arms within these companies are reaching inflection points that could fundamentally alter their growth trajectories and valuation frameworks.

And then there’s Wockhardt/Sun pharma advanced, a company that has bet the house on novel drug discovery in antibiotics, creating what is arguably India’s most advanced NCE pipeline.

29) Wockhardt - India’s Most Ambitious Drug Discovery Bet

Wockhardt’s story is unlike anything else in Indian pharma. This is a company that has spent 25 years building an end-to-end novel antibiotic discovery platform from basic research to manufacturing to clinical trials to commercialization with a team of 145 researchers including 50 PhDs. The result is a pipeline of 6 NCE molecules in clinical development, with 6 QIDP (Qualified Infectious Disease Product) designations from the US FDA, confirming that these are not me-too drugs but genuinely differentiated molecules meeting unmet medical needs.

Dr. Murtaza Khorakiwala, MD, set the context with understated confidence: “We started off as an Indian company 55 years back in a generic business and over the last 25 years, we have evolved into a global company where 70% of our revenue is outside India. Also, our focus and our operations have fundamentally moved or are moving from being a generic focus to a research-driven organization.”

The Pipeline -

Wockhardt’s NCE portfolio is the most comprehensive novel antibiotic pipeline from any company in India and arguably among the most advanced globally for gram-negative resistant infections:

1. ZAYNICH (Nafithromycin/WCK 5222)

Status: Global Phase 3 completed with outstanding results are 20% superiority to existing treatment (not just non-inferiority, which is the typical bar)

India Phase 2: >90% efficacy against carbapenem-resistant organisms — the most dangerous class of drug-resistant bacteria

DCGI filing: Submitted March 2025

Compassionate use: 51 lives saved in patients otherwise untreatable by existing antibiotics

Positioning: Destination therapy for difficult-to-treat gram-negative infections (Acinetobacter, Pseudomonas)

Market: Global launch planned (Phase 3 conducted across US, Europe, emerging markets, India)

Dr. Khorakiwala shared the most powerful data point on the call: “We have saved 51 lives in the last 1.5 years by having ZAYNICH given to patients who are otherwise untreatable by existing treatments. And that just goes to validate in real life the results that we have got in the clinical trial of 20% superiority and 90% efficacy in case of resistant organisms.”

ZAYNICH is addressing one of the most critical public health crises globally, antimicrobial resistance (AMR), which the WHO estimates kills over 1.2 million people annually. A drug that demonstrates 20% superiority in a global Phase 3 trial against resistant infections has transformative commercial potential.

2. Miqnaf

Approved by DCGI, launched May 27, 2025

Used in community-acquired pneumonia and respiratory tract infections

Addresses macrolide resistance (azithromycin resistance is widespread) and is quinolone-sparing

Dedicated business unit created for specialist-focused commercialization

Saudi Arabia: Received Breakthrough Medicinal Product (BMP) status - facilitating accelerated approval

3. EMROK - 100,000 Patients Treated Successfully

Launched in India 3 years ago (post-COVID)

~10% market share achieved in MRSA infections

Expanding into additional indications: diabetic foot infections, orthopedic/bone infections (osteomyelitis)

Injectable + oral formulation - hospital-to-outpatient continuity of care

4. Foviscu (WCK 4282) - Phase 3 Ongoing

First-line empiric treatment for gram-negative hospital infections (cUTI, HABP/VABP)

Complements ZAYNICH: while ZAYNICH is the “destination therapy” at the top of the pyramid for resistant infections, Foviscu is the entry-level, broad-use first drug of choice

Global Phase 3 trial underway

If approved, the commercial TAM is significantly larger than ZAYNICH due to broader use

5. Odrate - NIH-Funded Phase 1 Complete

Once-daily injectable for gram-negative infections (vs. existing treatments given 2-3 times daily)

Enables outpatient/daycare treatment instead of prolonged hospitalization — massive cost-reduction potential for healthcare systems

Phase 1 sponsored and funded by the US National Institutes of Health (NIH) which is a powerful validation signal

Phase 1 completed with positive results

Additional early-stage molecules in gram-positive and gram-negative spaces

Beyond antibiotics, Wockhardt is building a diabetes biosimilar franchise. Insulin glargine is in the pipeline, Aspart has been filed with DCGI, and critically the company is developing GLP-1 analogs including semaglutide. A $30 million business development pipeline in biotech has been secured through partnerships over the next 24 months.

In the 3-5 year view, the growth vectors are: (1) novel antibiotics approaching global commercialization, (2) diabetes biosimilars scaling, and (3) GLP-1 analogs entering the market.

The Financial Turnaround -

The balance sheet transformation has been dramatic. Net debt has collapsed from 882 Cr in FY22 to just 64 Cr in FY25, aided by a 1,000 Cr QIP. With ~600 Cr cash on hand, Wockhardt has the financial runway to fund the NCE pipeline through commercialization without dilutive fundraising.

EBITDA margin expansion from 9% to 14% (+500 bps) driven by aggressive cost reduction manufacturing restructuring (external to internal), energy cost reduction, and wastage elimination shows operating discipline alongside the R&D investment.

Wockhardt is the purest NCE innovation bet in Indian pharma. While Zydus and Lupin have innovation arms within larger generic businesses, Wockhardt has staked its identity on novel drug discovery. The 25-year, 6-molecule pipeline in antibiotics, the most neglected therapeutic area in global pharma R&D represents both the highest-risk and potentially highest-reward positioning in the sector.

If ZAYNICH secures global approvals (Phase 3 data is exceptional), the revenue potential is measured in billions of dollars globally. If Foviscu follows as the broad-use first-line therapy, the combined franchise could redefine Wockhardt’s valuation from “struggling generics company” to “global antibiotic innovator.” The AMR crisis ensures the demand; the question is execution and regulatory timelines.

Then there are these speciality pharma companies that are kind of an ancillary company to the pharma companies we discussed above. Here comes the companies like Advanced Enzymes, Hester Biosciences, Accent Microcell

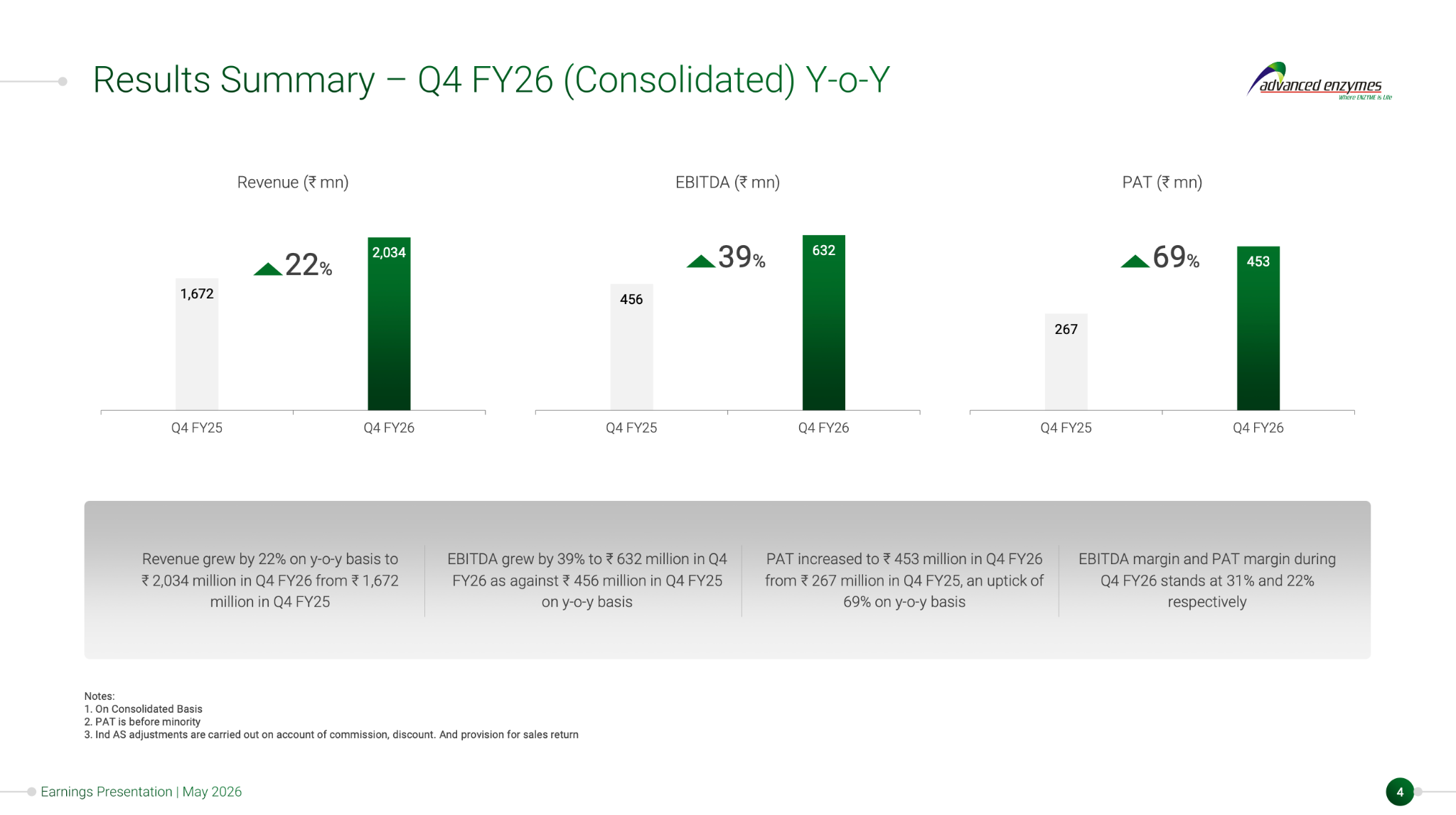

30) Advanced Enzymes - Where Enzymes Meet Pharma, Food, and Biotech

Advanced Enzyme is one of those rare companies that benefits from multiple secular tailwinds simultaneously pharma API manufacturing (biocatalysis), nutraceuticals (enzyme-based supplements), food processing (enzyme-aided production), and biotechnology (industrial enzymes). The company reported its highest-ever quarterly and annual revenue in FY26, and the growth trajectory is broad-based across segments.

Chairman Vasant Rathi opened with a macro observation that frames the company’s positioning: “Global pharmaceutical, nutraceutical, and biotechnology sectors are increasingly shifting towards wider adoption of enzymes across various regions. This macro trend is driving substantial market demand for a player like us, who can offer integrated end-to-end capabilities and customized solutions across these platforms.”

The Human Healthcare segment (pharma API, biocatalysis, nutraceuticals) drives the majority of revenue and grew 24% in Q4, the strongest quarterly performance. The company filed two food enzyme dossiers with the European Food Safety Authority (EFSA) and three with the US FDA during the year, while a new R&D center in Nashik is expected to become operational in H2 FY27 to boost the product development pipeline.

What makes Advanced Enzyme interesting in a pharma context is the biocatalysis angle. As pharma companies (both generic API and CDMO) increasingly adopt green chemistry and enzymatic synthesis for API manufacturing, the demand for industrial-grade enzymes grows. Laurus Labs, Neuland, and several other CDMO players have highlighted biocatalysis as a key manufacturing capability Advanced Enzyme is a supplier into that ecosystem.

31) Hester Biosciences - The Animal Health Vaccine Leader

Hester Biosciences operates in a pharma-adjacent niche that most investors overlook entirely animal health vaccines. The company manufactures and sells vaccines, health products, feed supplements, and therapeutics for poultry, large and small ruminants, and companion animals.

The positioning is genuinely unique: Hester is the world’s largest supplier of PPR (Peste des Petits Ruminants) vaccine and is the designated supplier to the WOAH (World Organisation for Animal Health) vaccine bank. In Africa, the company is a leading supplier of LSD (Lumpy Skin Disease) vaccine, a disease that caused massive livestock losses across India in 2022 and remains a global veterinary health priority.

The business model spans India, Nepal (manufacturing subsidiary with 1.24 billion doses capacity), and Africa (Hester Africa with local manufacturing), giving the company a production footprint across three geographies. The poultry healthcare and animal healthcare divisions cover the full spectrum from Newcastle Disease and Marek’s Disease vaccines for poultry to Brucella and Goat Pox vaccines for ruminants.

Hester’s relevance to the broader pharma story is thematic: as One Health (the convergence of human, animal, and environmental health) becomes a global policy priority, animal health vaccine companies stand to benefit from increased public funding and government procurement programs. The WHO’s global PPR eradication target by 2030 directly benefits Hester as the world’s largest supplier.

32) Accent Microcell - The Excipient Play on India’s OSD Volume Growth

Accent Microcell manufactures pharmaceutical excipients - the inactive ingredients (binders, fillers, disintegrants) that go into every tablet and capsule produced globally. The core products are Microcrystalline Cellulose (MCC), Silicified Microcrystalline Cellulose (SMCC), and Croscarmellose Sodium (CCS), essential inputs for oral solid dosage (OSD) formulations.

This is perhaps the purest volume play on global pharma growth. Every tablet manufactured anywhere in the world requires excipients. As India’s formulation output grows (both for domestic consumption and exports), and as global OSD volume expands, Accent Microcell benefits from the underlying production volume without exposure to product-specific pricing or regulatory risk.

With 63% export revenue, the company serves international formulation companies alongside domestic Indian pharma. The competitive moat lies in regulatory filings (excipients require DMFs/CEPs for regulated market use), consistent quality, and the cost advantage of Indian manufacturing.

They are also moving into speciality products but the new line commissioning for the company is delayed and management in this concall has not guided on to the commissioning timeline. One can keep a close eye on this development in the coming quarters as this can be a very interesting trigger for the company to increase the mix of value added products.

These companies won’t headline a pharma sector report. But collectively, they illustrate an important investment principle: when an entire sector is growing, the picks-and-shovels suppliers often offer the best risk-adjusted returns. Advanced Enzyme at 31% EBITDA margins, Hester with a global monopoly position in PPR vaccines, and Accent Microcell as a volume proxy for global tablet production each offers exposure to the pharma growth story with differentiated (and often lower) risk profiles.

So to conclude,

With these we have covered almost all the companies that have reported Q4 earnings in these theme and in the process we figured out few of the very interesting trends that are playing out across the sector which is driving these earnings -

1) Chronic shift in India is accelerating

2) US Market is graduating from generics to complexity

3) CDMO is structural theme but be ready for the lumpiness to be there

4) Margin expansion is real but its not just op leverage hitting but also the product mix change that is driving this change in mix

5) Capital allocation across the board is improving in the sector be it buybacks, M&A, Write offs, organic capex, or something else

6) API pricing which started to stabilise around Q2 is now starting to turn back up a little.

7) Innovation is becoming a core valuation driver - be it CDMO players trying to improve mix of new modalities or players trying to be an innovator (NCE players we discussed above)

This article has covered 30+ companies across 6 categories, analyzed over 80 earnings documents, and distilled thousands of pages of management commentary into what we hope is a coherent map of the Indian pharmaceutical sector in Q4 FY26.

The answer to why the Nifty Pharma index is at all-time highs is straightforward: almost every part of the value chain is simultaneously in the favourable part of its respective cycle. That’s rare. Historically, when API pricing was strong, formulation margins were weak (and vice versa). When US generics were booming, CDMO was a niche. When domestic brands were growing, innovation was a distant aspiration.

Today, for the first time in a decade:

1) Domestic branded is growing double-digit with chronic shift accelerating and GLP-1 creating new TAM

2) US formulations have graduated from commodity to complexity, with biosimilars opening a new profit pool

3) ROW markets are scaling with EU GMP and branded strategies

4) CDMO is riding the strongest tailwind in its history (China+1 + patent cliffs + new modalities)

5) API pricing is stabilizing after three years of deflation

6) Innovation pipelines are producing real clinical and commercial milestones

7) Capital allocation is disciplined and shareholder-friendly

But What Could Derail the Story?

1. US Policy Risk. Any material change to US drug pricing policy, FDA approval timelines, or patent challenge frameworks could impact the single largest profit pool for Indian pharma.

2. China Re-entry. If geopolitical tensions ease and Chinese API/intermediates/CDMO players resume aggressive competition, the pricing tailwind reverses for multiple categories.

3. GLP-1 Pricing War. If the Indian semaglutide market becomes a race to the bottom on pricing, the margin contribution from this massive new category could disappoint. But even in this case there will be some players like pharma distributors or injectables players that can benefit from this tailwind because for them volume matters more than pricing and both have inverse correlation

4. CDMO Capex Overshoot. The sector is investing heavily in Sai Life, Laurus, Neuland, Anthem, Cohance all building simultaneously. If demand doesn’t keep pace with capacity creation, utilization rates and margins will suffer.

5. Regulatory Surprises. FDA warning letters, import alerts, or clinical trial failures remain ever-present risks in pharma. A single regulatory action can impair a company’s largest market overnight.

6. Currency Reversal. INR depreciation has been a tailwind for export-oriented companies. A sharp rupee appreciation would compress export revenues in INR terms.

The opportunity for investors lies not in buying pharma as a monolith, but in understanding the six distinct categories, identifying which cycle each is in, and selecting companies with the best combination of structural positioning, execution track record, and valuation margin of safety.

In simple terms look for companies that have some unique competitive moat in right tailwinds with reasonable valuations so that even if the cycle takes a wild turn you do not wipe your capital off sitting on top of a commodity player….

GOAT Article on Pharma 🐐

👍👍👍👍👍👍👍

❣️❣️❣️❣️❣️❣️❣️