Anatomy of Multibaggers

Key to Multibaggers

In this dull, drab and boring market I thought why not pick up the pen after a while and write something about a key Mental Model which has led to multibagger outcomes in the past. Apologies for using the term Multibagger in advance :)

The Mental Model is

Product Mix Change

Lets understand this mental model better from the Story of the Business X and then we will discuss plenty of Indian & International Examples

Ten years ago, there was a small manufacturing company that made basic industrial components which had low margins and plenty of competition.

Every year, they tried to grow by selling more of the same.

More volume.

More clients.

More pressure on pricing.

The business survived.

But never became special.

Then one year, management changed one thing.

They didn’t increase capacity.

They changed what they sold.

Slowly, they started supplying customized parts to a few critical customers. Products that needed engineering support. Products that couldn’t be easily replaced.

At first, it was just 5% of revenue.

No one noticed.

But every year, that share grew.

5% → 15% → 30% → 55%.

Margins improved.

Cash flows strengthened.

Customers became sticky.

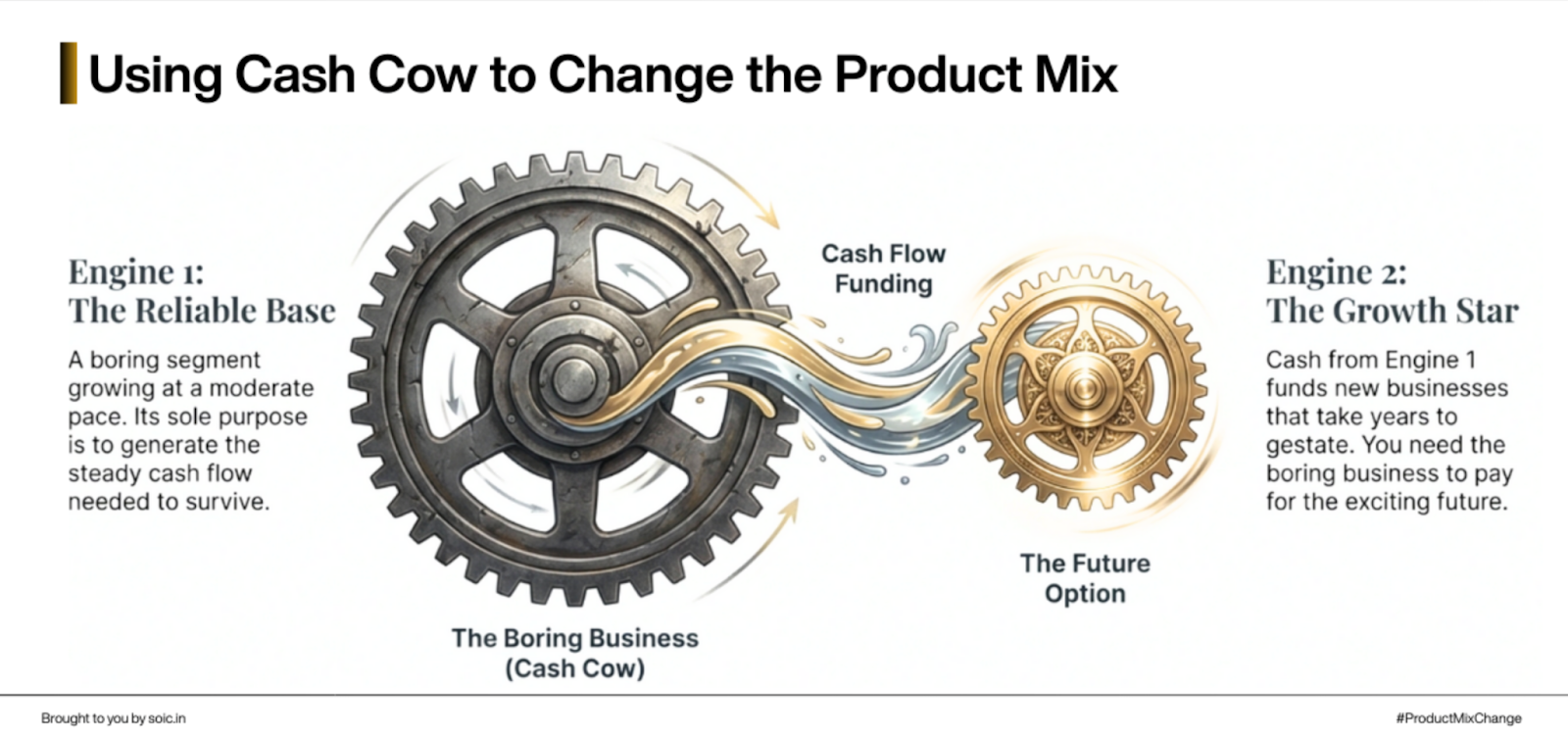

From outside, it still looked like the same company. But the ROCE profile, Margin profile, & Competitive advantage of the business improved. This led to a Multibagger outcome over a period of time.

One thing that is common amongst all these businesses is that they have a cash cow product segment which grows at a moderate pace, and the cash flows from here are used to generate newer businesses/optionalities which start to reflect a few years down the line in financials for these companies.

Lets jump into examples and the we will see how to find these stories:

1. Sansera Engineering:

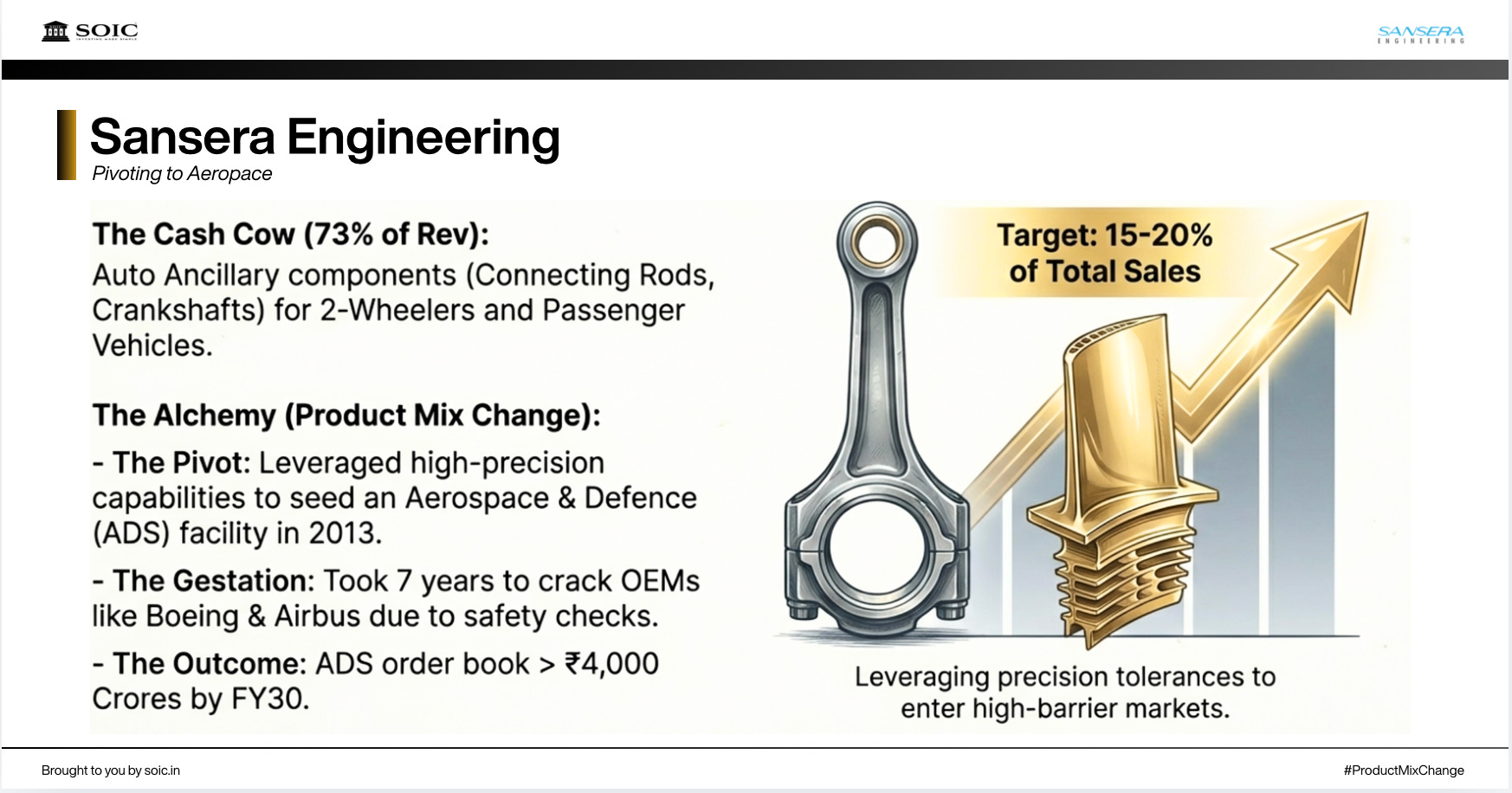

Sansera is an Auto Anc which is a market leader in connecting roads, rocker arms and crankshaft assemblies. Majority of their Base AUTO business comes from ICE engine vehicles. Majority of their AUTO Anc business comes from 2 Wheelers, followed by Passenger vehicles and Trucks. Their core focus is Precision-forged and machined components for automotive OEMs in primarily engine, transmission and powertrain parts. This part of the business contributes to 73% of their revenues.

Sansera is known for making products with high accuracy, complexity, & tight tolerances. Using these capabilities Sansera seeded a new business optionality way back in 2013 by setting up a dedicated facility for aluminium and titanium machined components for Aerospace parts.

Now, for 7 years this business didn’t get any mention as the scale was small and it takes minimum 5-10 years for a company to successfully enter this in spite of their capabilities given the First Article Inspections involved and the mission critical nature of the business.

After cracking key OEMs like Boeing, Airbus in aerospace and LLAM Research in semiconductors, Finally, Sansera spells out this business segment separately into ADS business where the order book has gone to above 4000 crores by FY30. Can this business be 1000 crores+ and contribute to 15-20%+ of sales? That is the key Question.

This is how Product mix change is, it starts off slow and then becomes visible to everyone. There were times last in Sansera where post QIP a lot of investors kept questioning them as the results were disappointing. These stories are also super volatile and lumpy. Always remember this before looking at product mix change.

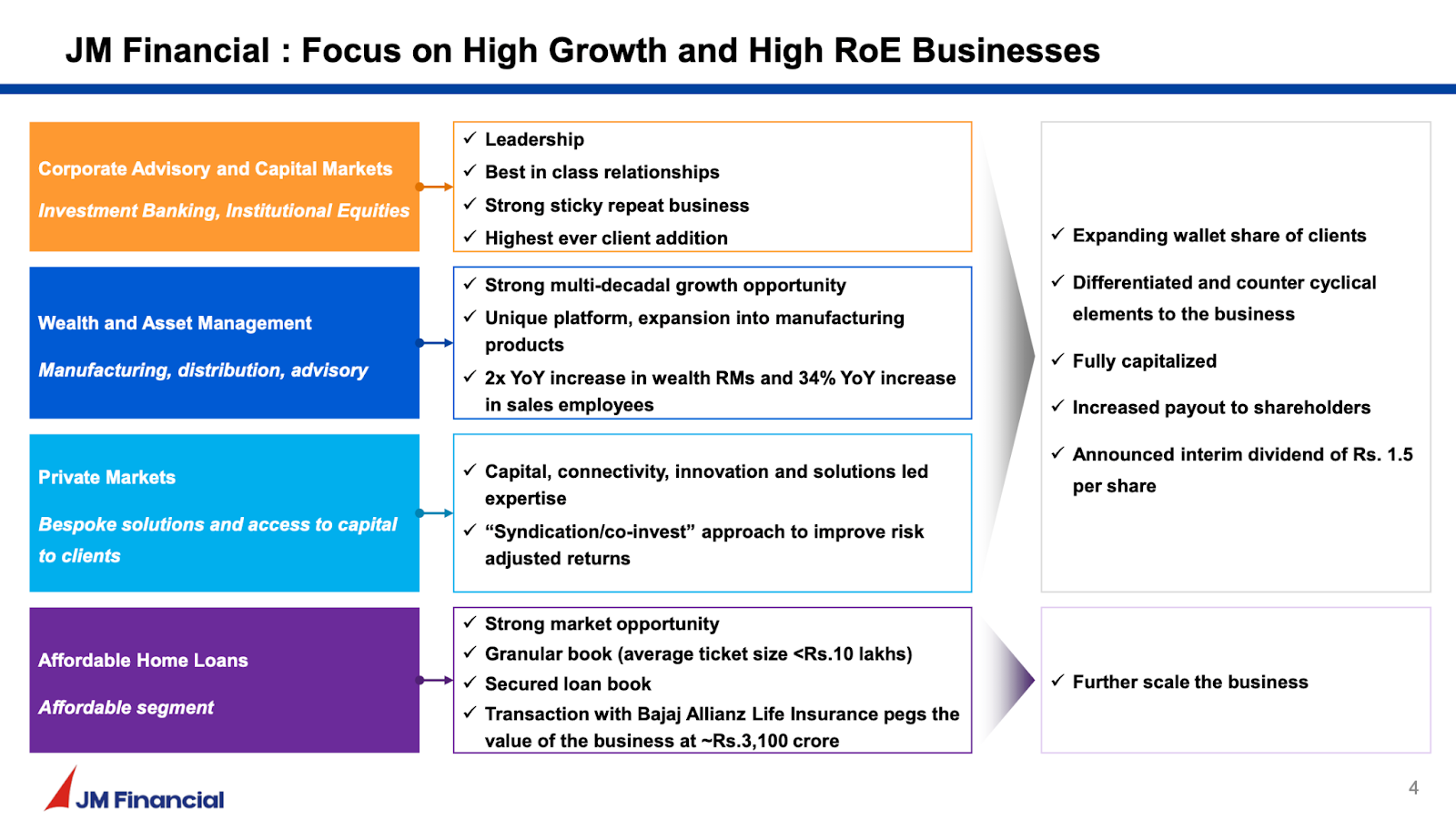

2. JM Financials:

For the better part of the last decade, JM Financial’s narrative was hijacked by its exposure to wholesale lending, a capital-intensive, cyclical, and regulatory-heavy sector. This dragged the company’s perceived valuation down to that of a standard NBFC, ignoring its pedigree.

The current story is one of aggressive product mix change. JM Financial is shedding the “boring,” capital-heavy skin of a wholesale lender to reveal its original DNA: a high-ROE, fee-generating Investment Banking and Wealth Management powerhouse. The Investment Banking segment generates stellar returns, with ROEs ranging between 19% and 24%. JM in IB has a 50 yr vintage where it managed India’s first billion dollar IPO of TCS and recently of Tata Technologies

These businesses were balance-sheet heavy. A significant portion of capital was tied up in segments that were dragging overall ROE down to single digits. The market viewed JM Financial not as a premier investment bank, but as a wholesale financier struggling with a difficult real estate cycle

In 2024 they finally decided to completely run down this wholesale business and move to an asset light structure putting more focus on to the side where there is better value and less volatility. This run-down is expected to release approximately ₹2,000 crore in incremental cash over the next 3-4 year.

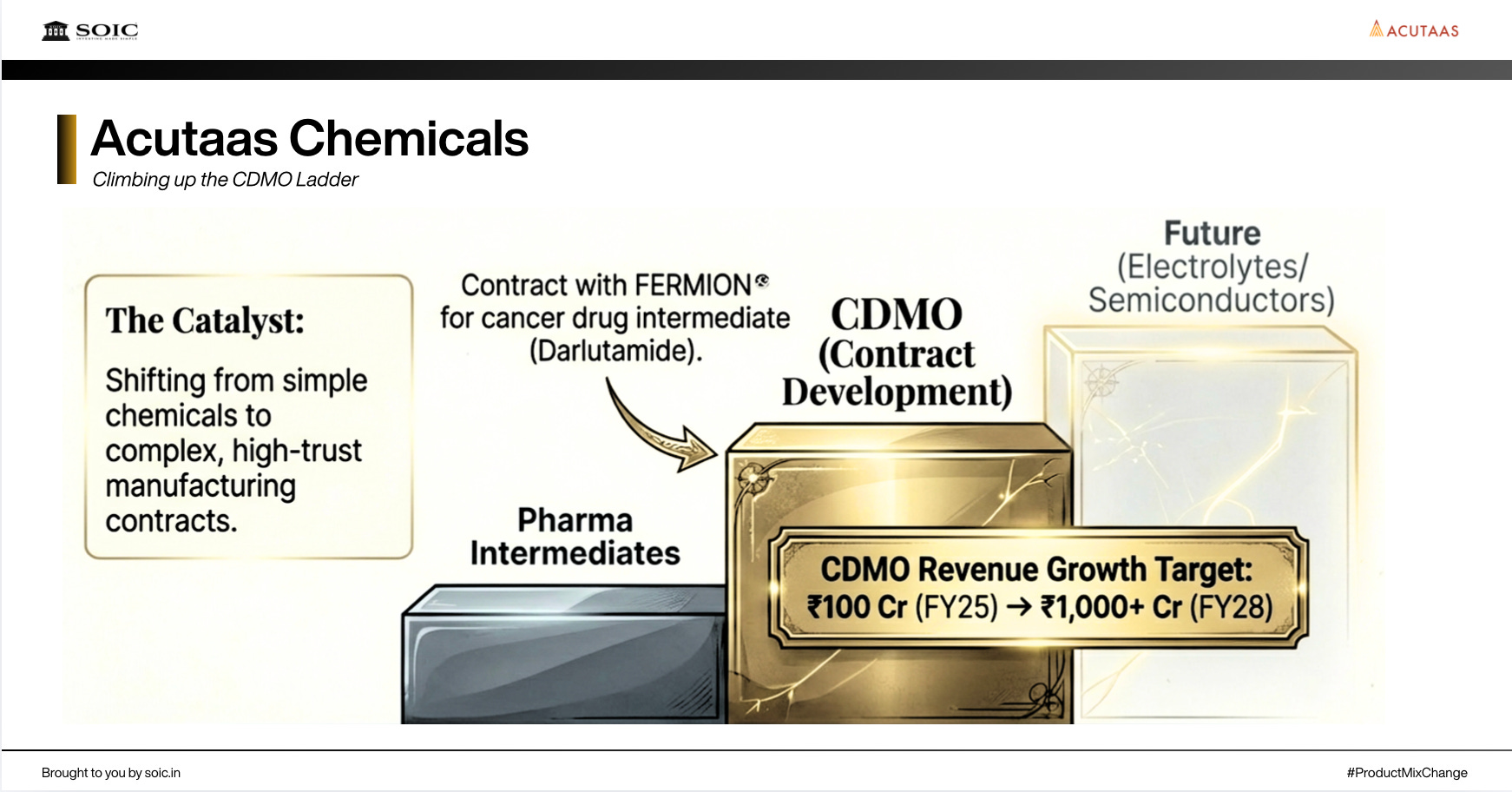

3. Acutaas Chemicals:

Acutaas is a story where product mix change has played out and is playing out. When they IPO’d the story was more to do with Pharma intermediates and Chemicals. But the company was building a CDMO business and they landed a big contract with FERMION for Darlutamide which is a key intermediate for NUBEQA which is a prostate cancer drug by Bayers. Interestingly, Darlutamide was recently approved in China too, which can lead to further growth for ACUTAAS & Navin which is the other supplier to Fermion. In FY25, the company talked about growing their CDMO business from 100 crores to 1000+ crores by FY28. Now, 2 other stories of Electrolytes and Semiconductor chemicals seem to be emerging here at the moment.

Just see what has happened to the margins of the company post this mix change has started reflecting into numbers

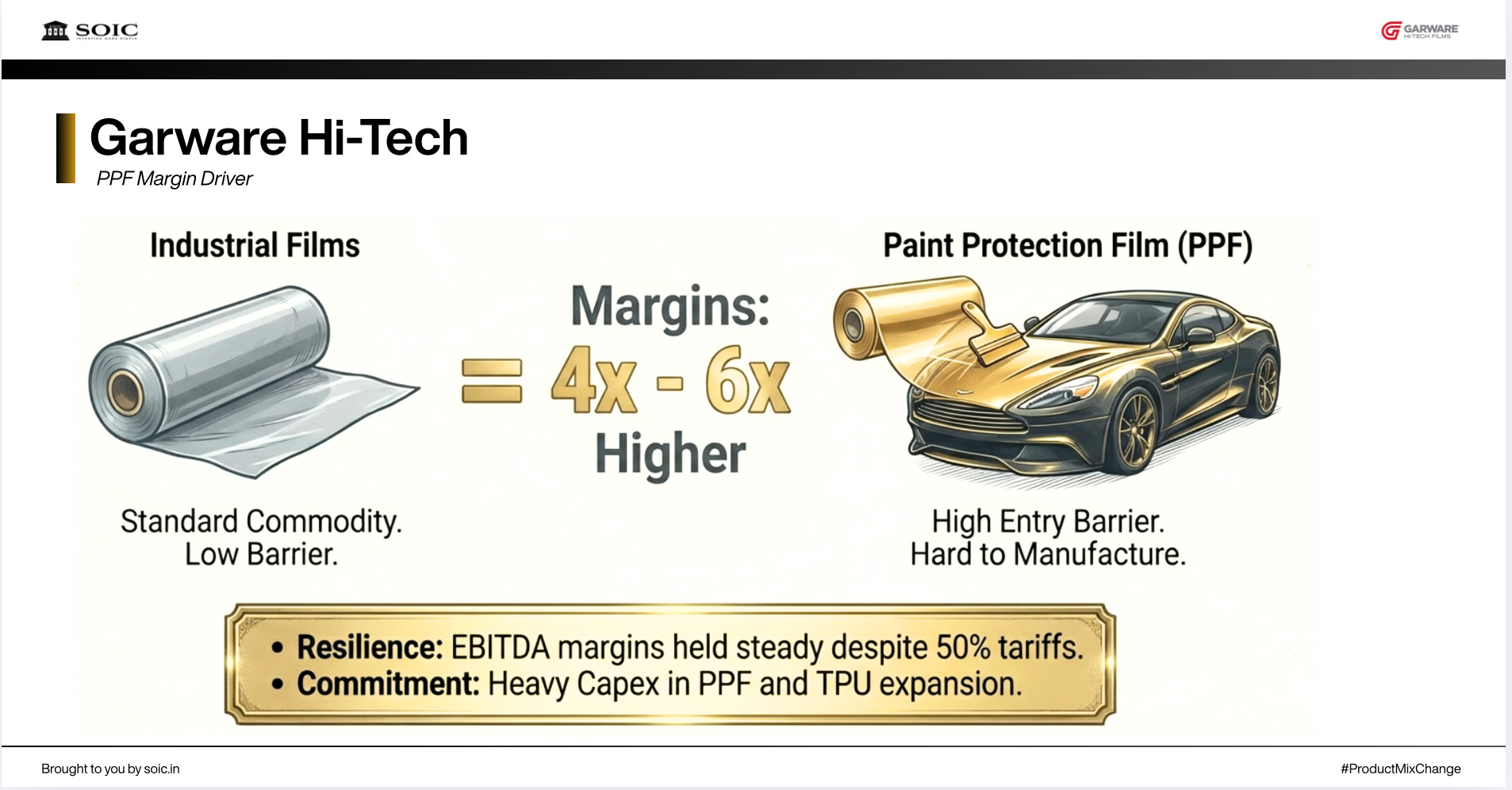

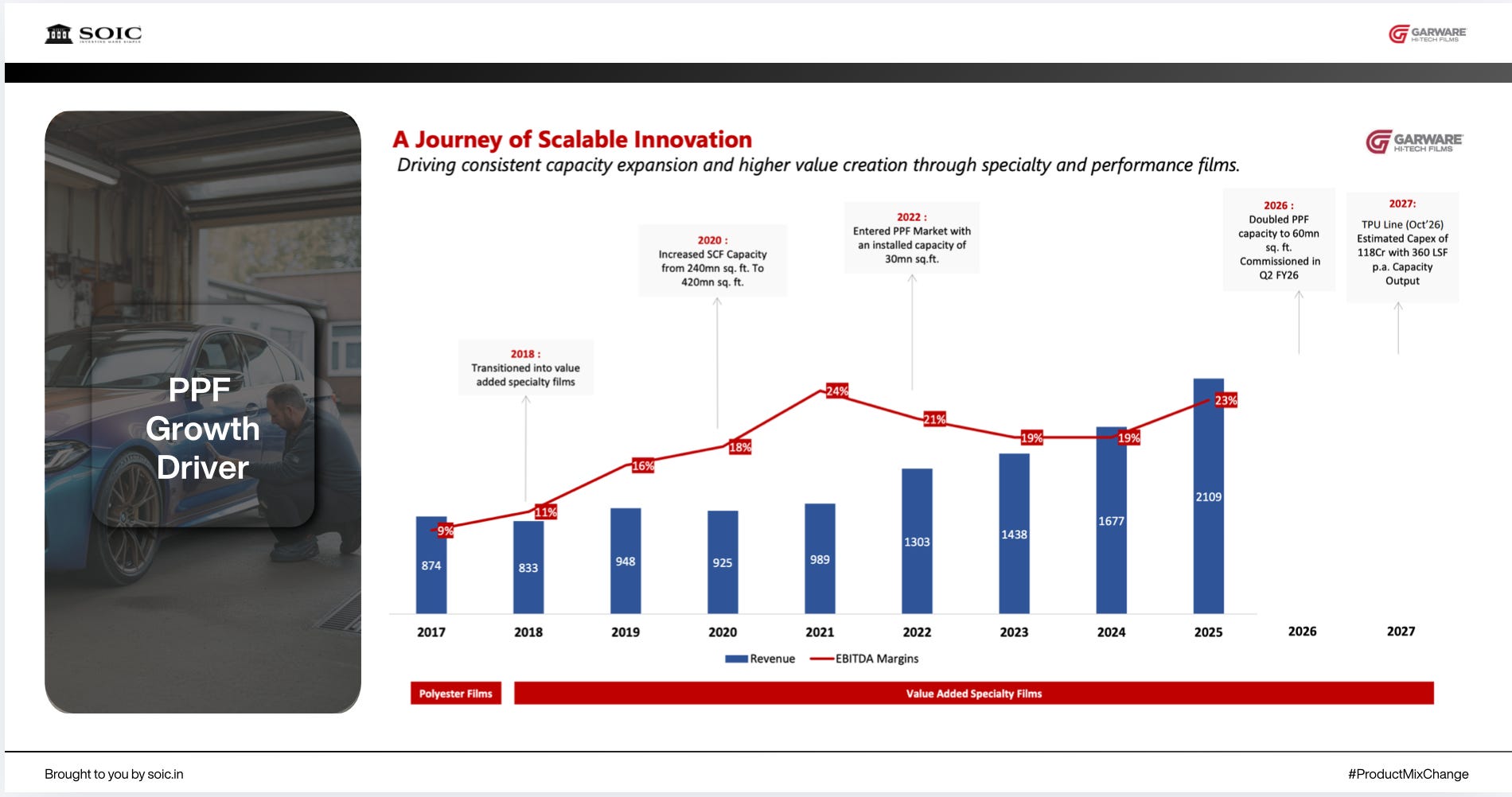

4. Garware HI tech:

Garware Hi tech used to make industrial films and started getting into Paint Protection films and Solar control films in 2017-2018. These films are much harder to crack and the margins earned can be 4-5 to even 6 times higher than Industrial Films. PPF films are used as a protection layer on cars and Solar control films are used to control the temperature of buildings which blocks UV radiation and controls heat.

I was wondering what will happen to the margins of this business given more than 40% of their Sales comes from the USA. To my surprise, the company has largely held its EBITDA margins in spite of tariffs of 50%. They have just done capex to expand their PPF line and are doing capex to get into TPU which is a type of PPF film which they weren’t making before.

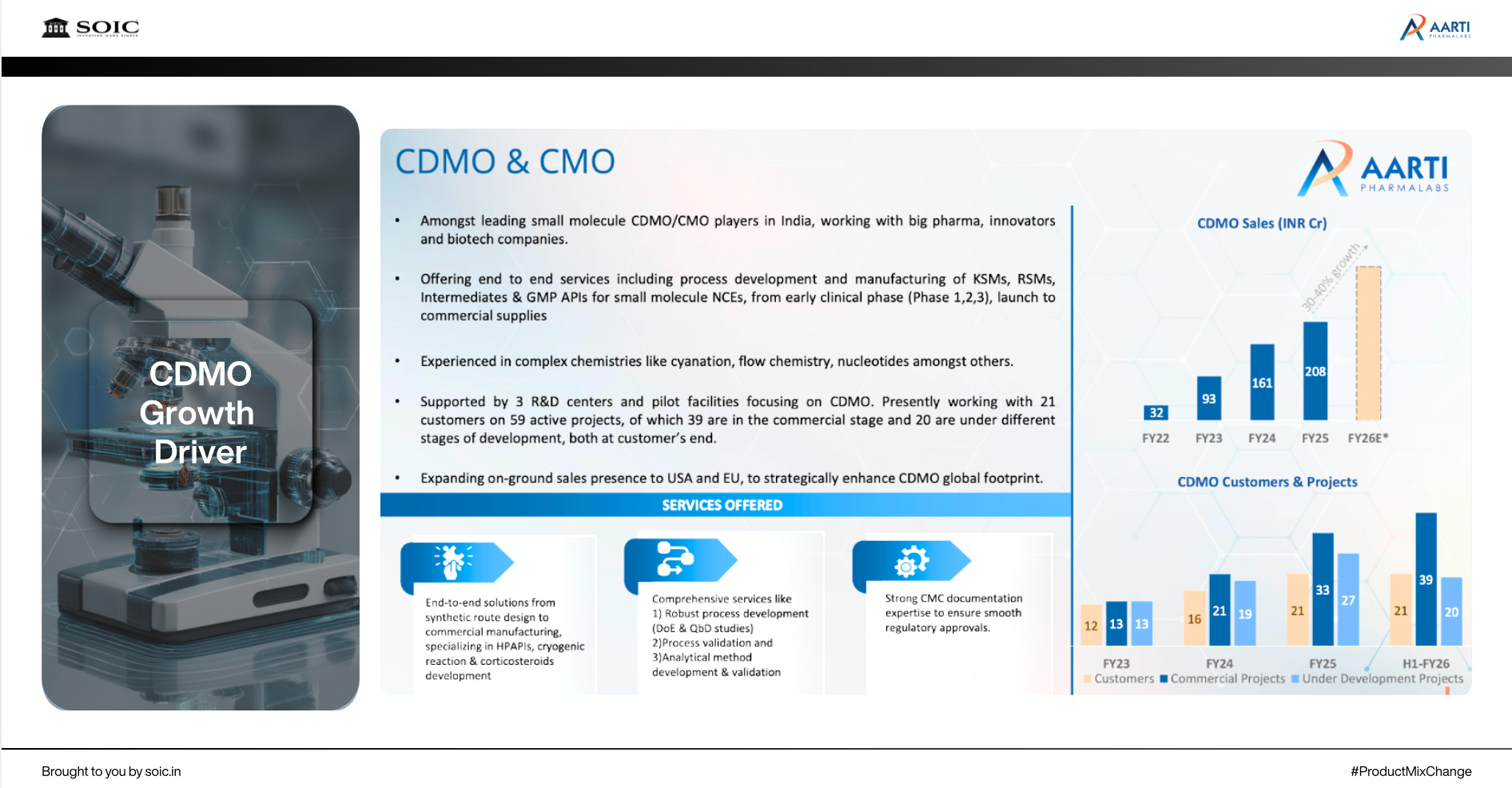

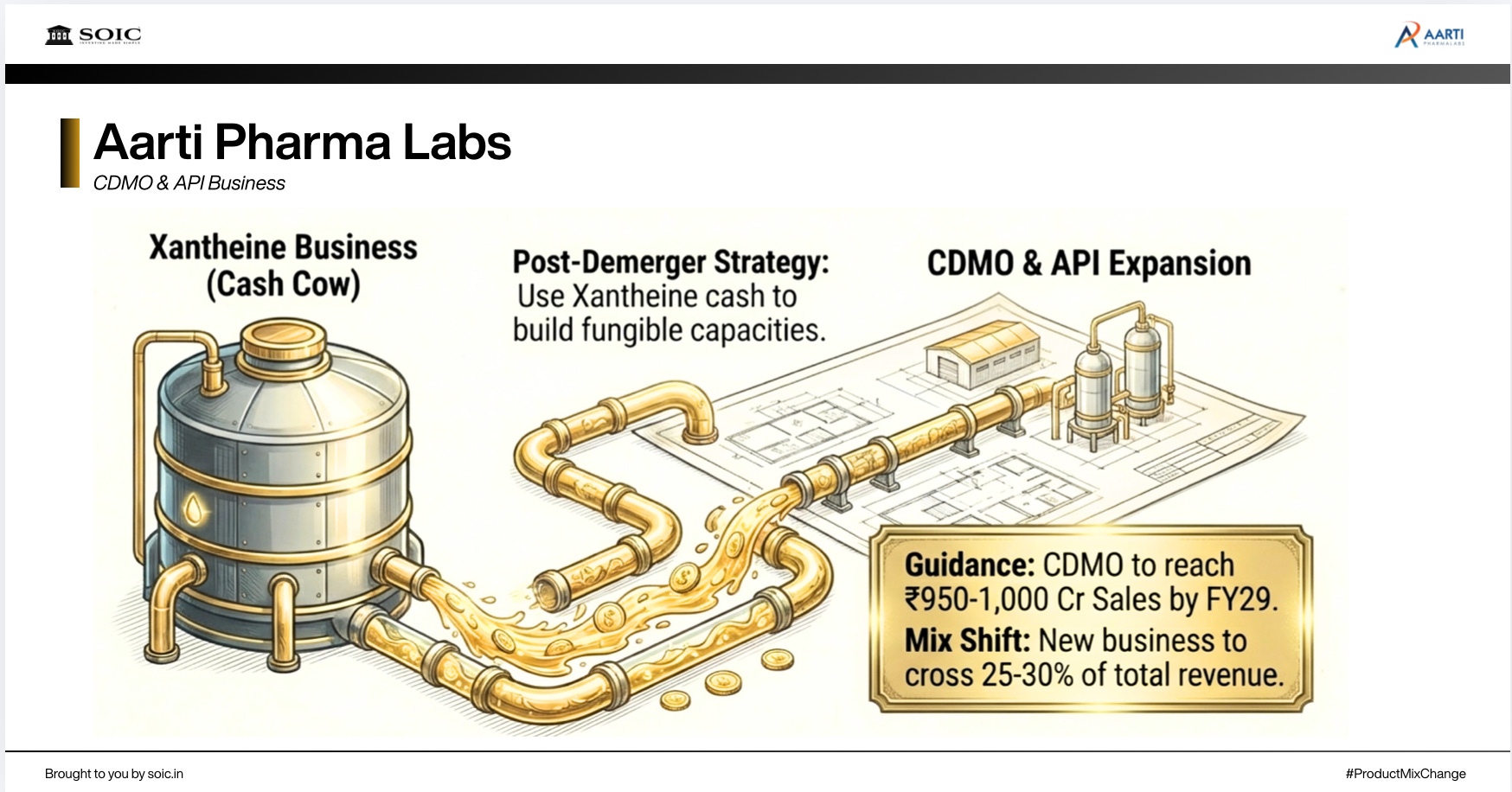

5. AARTI Pharma Labs

Just like the stories above, AARTI Pharma labs has 3 business segments:

1. API

2. Xantheine

3. CDMO

Post their demerger from the AARTI group, AARTI Pharma labs has been using cash flows from their Xantheine business to do capex for the CDMO/API fungibile capacities. Just see how the CDMO business has been growing

Post the capex at ATALI, the company is guiding for CDMO business to touch 950-1000 crores of Sales by FY29. Which means that the business will cross 25-30% of their overall revenues and can drive significant margin expansion.

How to find these stories and what is the cost of looking at such cos?

1. Look for words like new product introduction, new business segments and value added products in conference calls of companies.

2. Check results of different business segments and see if any new business segment has started growing faster vs the overall business.

3. See if the company has started doing capex for the new business segment separately. This is usually a big tell sign that the business is inflecting. Eg: How NAVIN did separate capex for its CDMO facility.

There are only two costs of looking at such businesses:

1. Volatility

2. Lumpiness

Hope all of you emerge and do well when this bearish or sideways phase of the market is over. I intend focus more on teaching and learning during such phases 🙂

In case you want to join my latest webinar, I am doing one on finding Unique and moated businesses this Sunday at 12pm. Do let me know what you think of this blog in the comments below!

Registration Link: https://learn.soic.in/learn/fast-checkout/257760?priceId=246938

Use a browser to enrol, mobile apps apply an additional 30% fees

Disclaimer - This is only for education purpose and not a buy/sell recommendation

What was your exposure in these stocks at nascent stage. One can find umpteen such multibaggers on hindsight.

Cool