Portfolio Allocation Approach: Diversify, Concentrate or Both?

The thought of writing this blog comes from the emails that I receive every now or then. This is how the emails go:

“Hi Ishmohit, hope you are doing well. This is my portfolio of 115 stocks. Can you please suggest to me any good reading material or any way I can reduce these holdings to a manageable level?”

Or the second most common emails I receive are like this:

“Hi Ishmohit, hope you are doing well! I own Dubilant dengrevia and Smith labs. My allocation in the first stock is 55% and in the second stock is 45%. I am down by 30% in the first stock and 10% up in the second stock. Any reading material or suggestions do you have to help me make a proper portfolio. As the results in the Dubilant weren’t that good, and I am down on the position. I don’t know what to do. Any suggestions?”

These are the two most common emails that I receive when it comes to the question of Portfolio Allocation. Whenever I receive these emails I realise that the joy of investing has been taken out from the person who is sending the mail. In the former example one is tense because of owning too many stocks and lacks the ability to track them. In the latter example, one is tense because of the volatility in a concentrated portfolio. Just close your eyes and imagine you have a two stock portfolio with 50% each. One of them falls by 40% from your purchase price. This effectively means your portfolio will go down by 20%. That is the type of volatility which just kills the fun of investing yourself without the help of any mutual fund or a professional.

Let’s deep dive into 5 truths about portfolio allocation:

1. The story of a too diversified portfolio

“I don’t know anybody who can really do a good job investing in a lot of stocks except Peter Lynch.”- Bill Rouane

What is the purpose of diversification in the first place? Diversification helps you reduce systemic or sector specific risk.

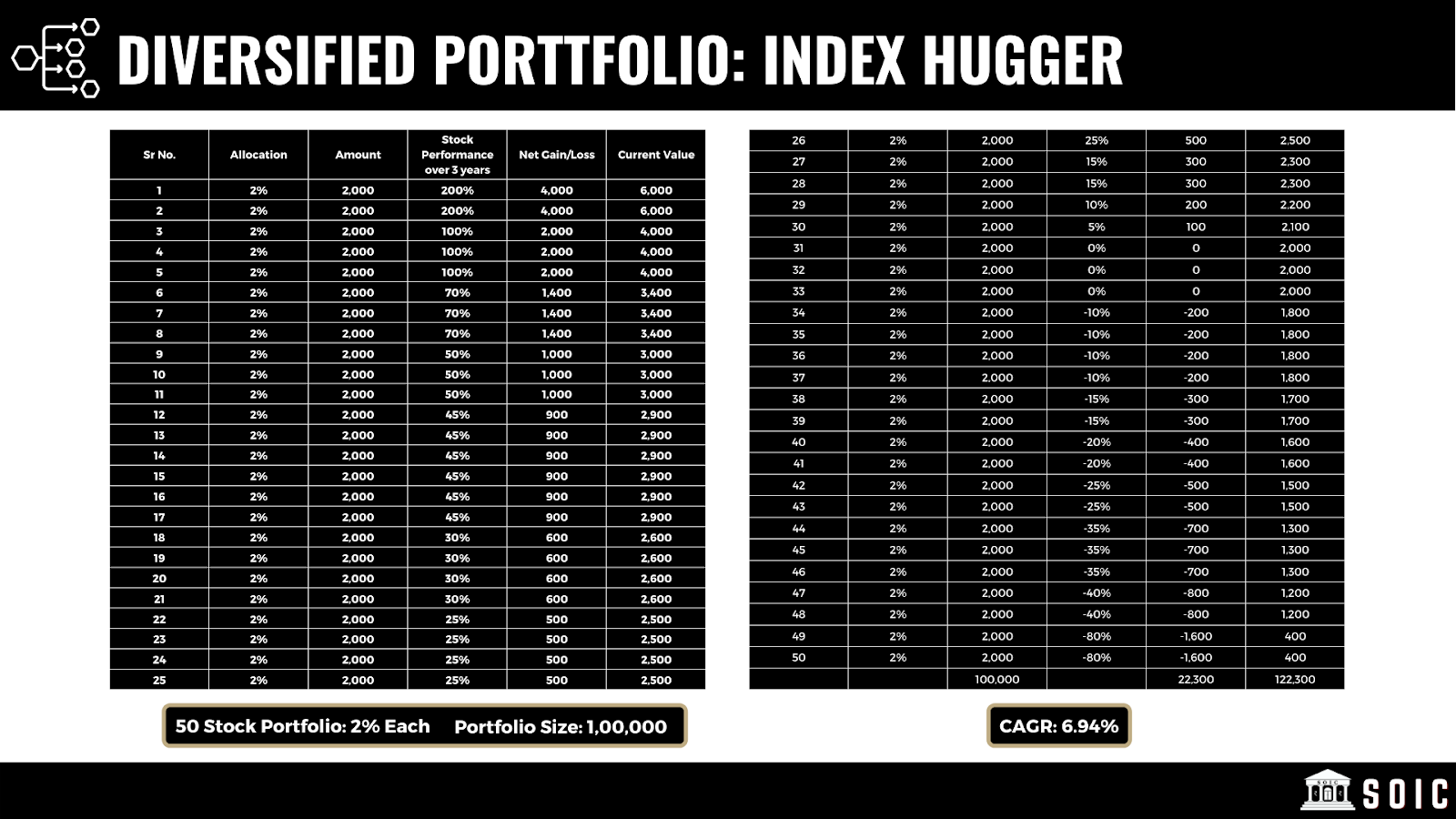

Let’s look at the following portfolio and let's look at the performance of the portfolio 3 years out.

For a lot of investors who are reading this blog, this will be a familiar sight, as they will have such a widely diversified portfolio. If you look at this portfolio closely you will observe two things: first, you will observe that there will be a few winners which go up by 200-300%. Then there are few losers which go down by 60-70%. The best thing about a widely diversified portfolio is that you will never go bust as an investor. You will ensure that you will survive for a long period of time. However, on the other hand the bad thing about a widely diversified portfolio is that you kill optionality. You won’t ever have a life changing investment. Even if you have one, what's the point of owning 1% in a stock that goes up by 1000%? This basically means a 10% impact on the portfolio. A widely diversified portfolio is good in the beginning as it ensures you won’t go bust or it is good for the institutions who have a mandate to deliver consistent returns or returns that are not too different from the benchmark. Most of these institutions are known as ‘index huggers’. My ultimate question to you, the retail investor is, given that you have all the flexibility in the world and are not answerable to anyone apart from yourself for the returns. Why will you hug the index or go for a widely diversified portfolio?

If you really want to follow this approach, I suggest you read this entire thread: https://forum.valuepickr.com/t/gurjot-portfolio/710

You will get the real insight from a practitioner's point of view and not just bookish knowledge.

Those who have less time to devote or want to survive for a long period of time then 50+ stock investing might work for you. A good question worth asking in that scenario, then why not just invest in a good mutual fund which is also similarly diversified?

2. The story of a too concentrated portfolio

“ Condoms aren't completely safe. A friend of mine was wearing one and got hit by a bus”- anonymous.

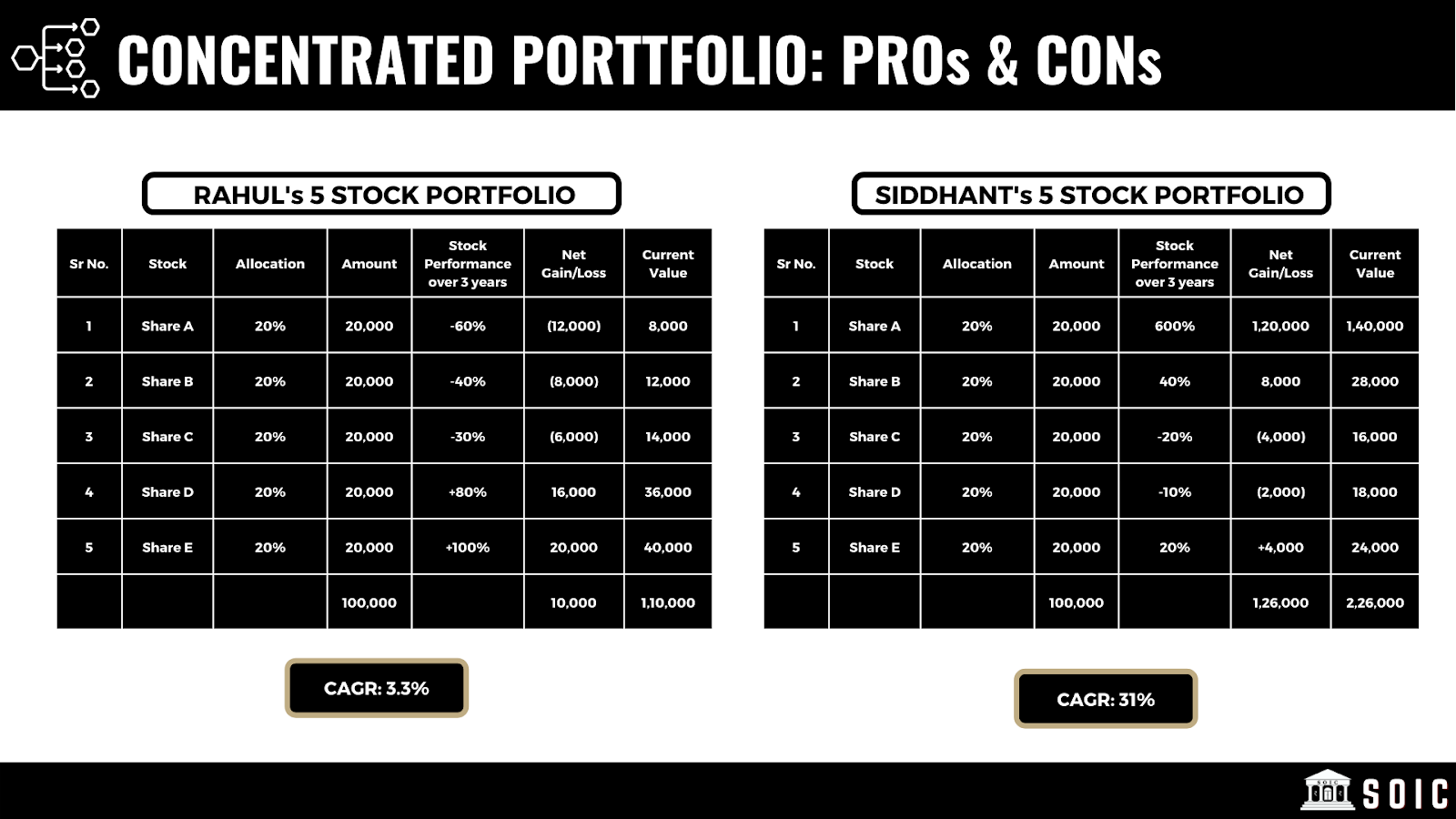

Let’s look at the story of two friends, Rahul and Siddhant. Both run a concentrated portfolio of 5 stocks and have researched their ideas well. Let's look at the outcome 3 years down the line.

In Rahul’s case, 3 companies in his portfolio went through severe headwinds as the world changed. In the first company's case there was a massive escalation of freight cost and raw material hike. In the second company’s case, due to the availability of substitute products the future profits that Rahul projected went for a toss. In the third company's case, the CEO who led the turnaround and made the company well known suddenly quit to find greener pastures elsewhere (rings a familiar bell?). Rahul couldn’t have imagined these outcomes three years ago, yet this is what happened. His PF went through a severe drawdown during a time when the index itself gave a 17% CAGR in the last 3 years.

Now let’s look at Siddhant’s portfolio and the eventual outcome. In Siddhant’s case what ended up happening was: in one of the companies that he owned, his bet was that the truck division would do well. But what really ended up happening was that the bikes division which he never even thought about, ended up doing really well. That division ended up conquering the market share. Stock was a huge multibagger for Siddhant (rings a familiar bell with Ramdeo Agrawal's Eicher story?). This is often the story with more than half the multibaggers in one’s portfolio. You bet on something, yet something else which is even more powerful works out.

In both stories, the point is that both investors had a good process and researched well. Yet they had different outcomes. The biggest downside of a concentrated approach is that you won’t be able to live to tell another story. Yet, the upside is such when it really works out. Then you attribute everything to your skill of adequately allocating. When the outcome can be equally credited to luck. Just like excessive diversification, a concentrated approach which hits the speedbreaker of bad luck often again ends up killing the optionality (Your survival in the markets). One lesson over the years I have seen with people experiencing good or bad outcomes with concentration is: Never let optionality die. Some risks are just not worth taking as a do it yourself retail investor.

3. Is there an optimal way?

Now you will think, Ishmohit you have told me about the pitfalls and upsides of both concentrated and a diversified approach. Is there an approach that combines the power of the two?

The answer: There indeed is. :) Before we get to it, there is one thing that you must understand.

“Allocation sachi mei hai khaas and baaki sab bakwaas”- SOIC

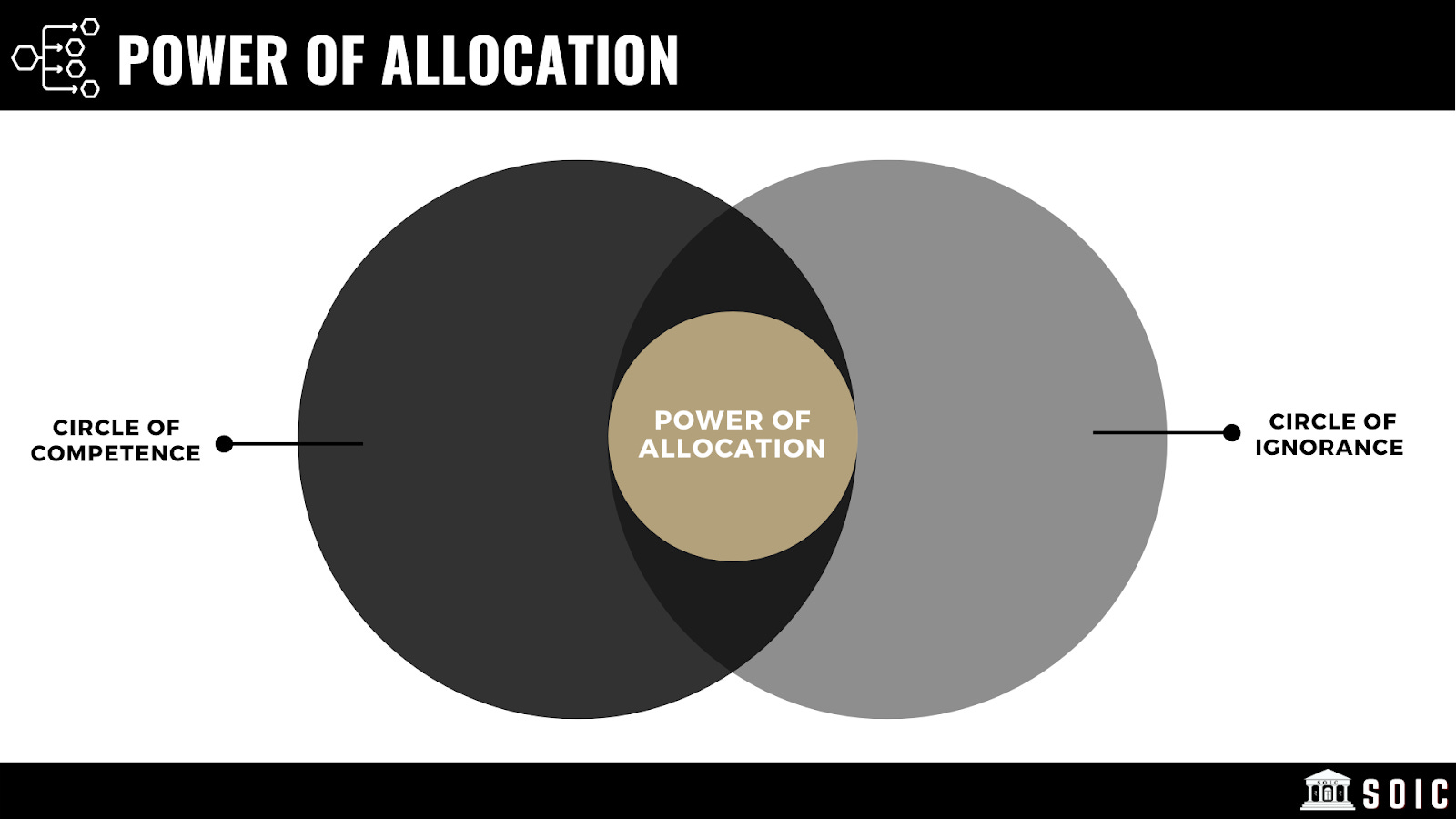

We all have heard about the circle of competence and why it is important. The inverse of the circle of competence is the circle of ignorance. What it means is that, In spite of investing in things that we only know we can still make a mistake. Make peace with the fact that there are some things that we will never know in spite of spending a number of years in the sector. For e.g. Warren Buffett who’s been renowned to pick financial stocks well. Still went wrong in his bet in the Irish Banks and similarly he read IBMs annual report for over 50 years and understood the business well. Yet, he still went wrong on the growth aspect. If such a great investor can go wrong and then mere mortals like us will also go wrong.

There’s a way to make peace between the circle of competence and circle of ignorance. This bridge is known as power of allocation.

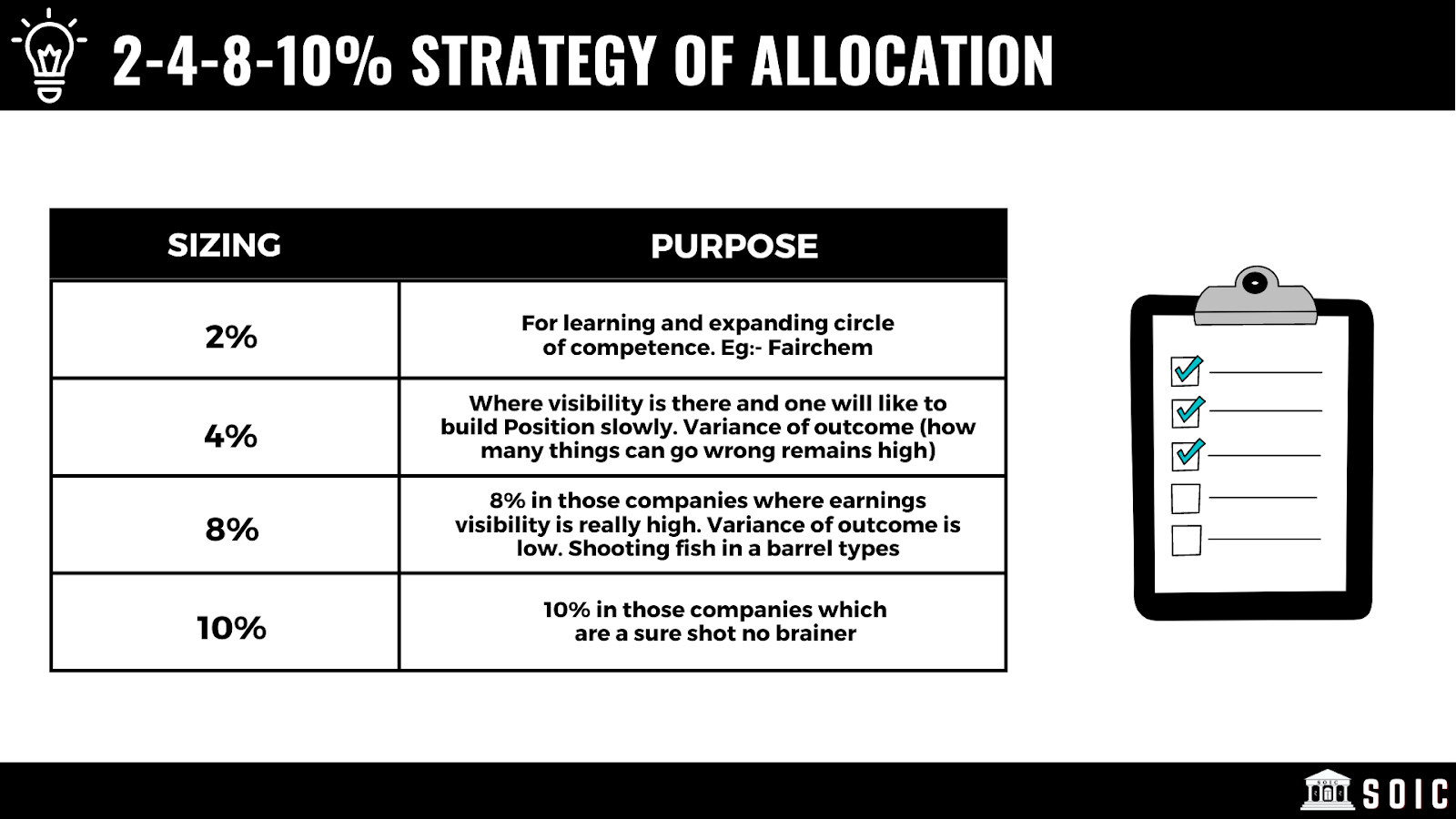

This is what I personally follow: I view diversification as a strategy of aggression, as diversifying across sectors and companies in the small cap space with 15-20 good businesses that can potentially grow at 20%+.

I use allocation as a strategy to concentrate in where my understanding and conviction in the cash flows is really high. This is how I cherry pick best of both concentration (optionality of huge winners) and diversification (ability to survive). For e.g. in one of the positions where I had 9% of my capital allocated, that one did phenomenally well and has been a 5 bagger since the initial purchase. Whereas, in another one where I initially allocated 4% that position is down by 30%. The first one had an impact of 45% on the portfolio in terms of returns and the second one had a negative impact of -1.2% on the overall PF returns.

I follow the 2-4-8-10% strategy of allocation:

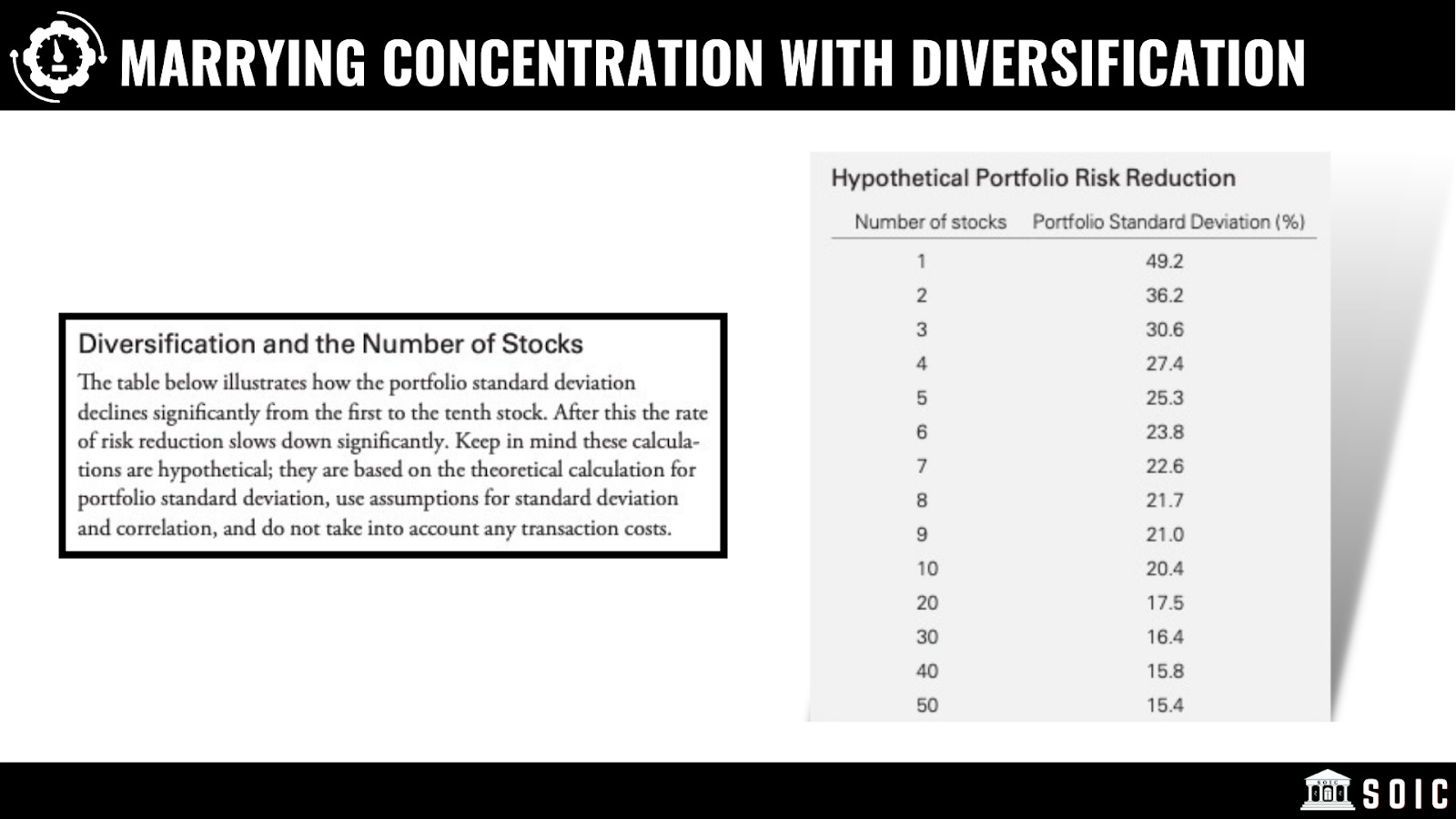

4. What about the risk in a portfolio of 15-20 stocks?

What you will find is that once you have more than 10 stocks in your portfolio then the rate of risk deviation reduces drastically. Having 15-20 stocks signifies that you are adequately diversified. See the proof for yourself here:

Conclusion:

I have been recently reading a book about Geghis Khan and how he was able to conquer the world in 25 years. Here’s a passage from the book which really hit me:-

“His fighting career began long before most of his warriors at Bukhara (the place which he conquered) had been born, and in every battle he learned something new. In every skirmish, he acquired more followers and additional fighting techniques. In each struggle, he combined the new ideas into a constantly changing set of military tactics, strategies, and weapons. He never fought the same war twice.”

When it came to war and conquering empires. Genghis Khan was practically a learning machine. The ability to learn, adapt and be agile is what gave him an edge in conquering vast territories of land within a span of one lifetime.

Thus,Genghis Khan was essentially a learning machine. The best thing about Do It Yourself Investing are not the returns. But, the continuous process of learning, you learn something new everyday. Who even knew that the music sector existed 20 months ago? This is how learning happens. We grow everyday as we learn new things in investing. Don’t let anything stupid (over diversification or over concentration) spoil this experience.

Let me know what you think?

Let me know which approach works for you and why in the comment section below and the number of stocks you own in the portfolio. :)

Thank you for reading!

Ishmohit Arora