Pricol: Turned Around A Loss-Making Debt-Laden Business

Pricol: Turned around a loss-making debt-laden business

Pricol is a Coimbatore-based auto ancillary company that, until now, has not been able to perform well. The company was typically facing problems of huge debt, bleeding cash, and huge labour problems. Pricol was a missed-priced bet with high expected growth and ROE mitigation leading to change.

The problem

For a long time, the company was facing acute labour problems, which was one of the reasons it did not perform well operationally. The conflict between the management and the workers proved fatal in 2009, as the workers killed the HR head of the company. The company also saw many senior levels exist, which resulted in the promoter family taking control over the management.

The company’s image was damaged, leading to falling revenues and profits. Since 2011, the company has entered a restructuring phase where it has reviewed its product mix, market leadership, management financials, and future road map.

The change

In August 2014, the company appointed new professionals to the management team and also signed a wage agreement with workers in the Coimbatore and Manesar units.

This has not only improved their image in the market but also won the confidence of their customers. The Promoter Group took complete control of the management in June 2015, and the turnaround has started.

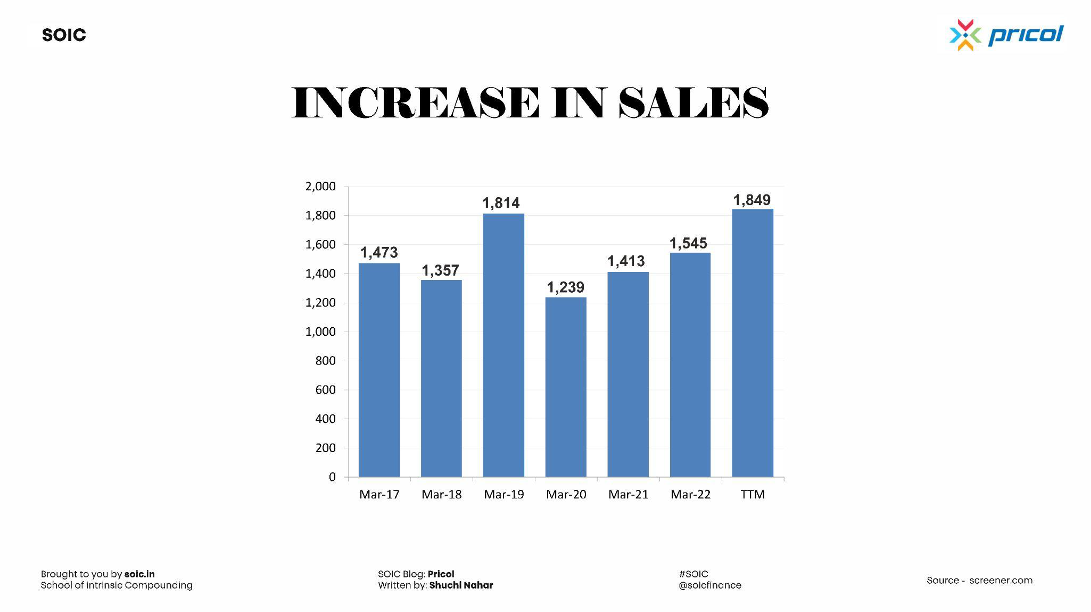

The effect of the management change and restructuring process is already visible on their financial statement. This company, which has grown at a CAGR of only 10% in the last 5 years, has managed to grow its topline by 26% in 2016 and has turned positive on the profitability front.

Strategy

The new management has a simple rule focusing on the products to make them the top three, and if they are unable to do so, they will immediately exit those products. They not only want market leadership in all their products but also aim to have multi-location plants to meet customer requirements just in time.

Separating the wheat from the chaff

Pricol, with an ambition to diversify and attain a global footprint, acquired businesses outside India, which had been draggers on its profitability & B/S. The company had a subsidiary in Spain that was the holding arm for step-down subsidiaries in Brazil (acquired in FY15), Mexico, and the Czech Republic (both for wiping business; acquired in FY18).

The companies were lossmaking, with combined losses across three step-down subsidiaries at ~105 crores in FY19 and ~89 crore in FY20, respectively. The three companies, along with the Spanish holding company, have now been hived off with all liabilities addressed and investment of ~400 crores in these companies written off.

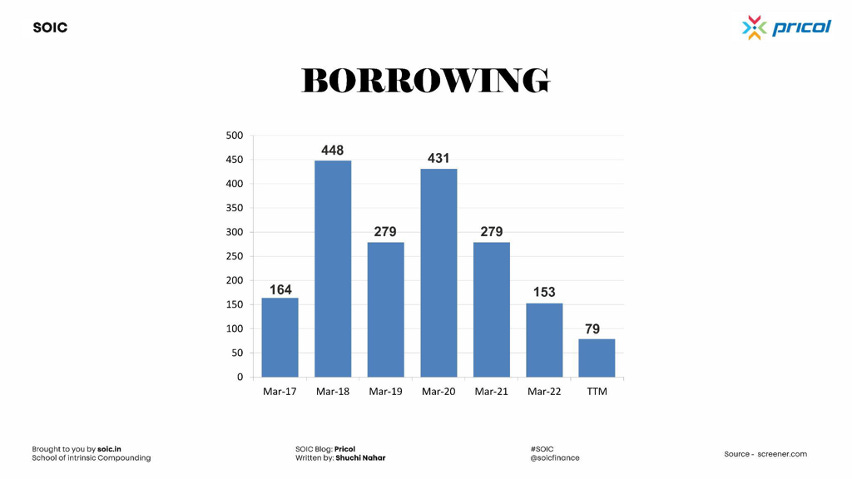

Consequently, consolidated debt on books was reduced sharply from ~431 crores in FY20 to 283 crores as of February 2021. With no more cash support towards erstwhile loss-making entities & heavy capex cycle behind it (invested ~300 crores in FY18-20).

Revenue was expected to grow by 12% in FY23 and a significant improvement in the company’s net profit in FY23 majorly due to the sale of loss-making subsidiaries, deleveraging measures, cost control measures, and the addition of technology-intensive products in the company’s product portfolio

Net sales are expected to grow at an 18.8% CAGR over FY22-25E to 2,591 crores, whereas margins are expected to inch up to 12.2% in FY25E. PAT is expected to grow at a 44.5% CAGR over FY22-25E, albeit on a low base and with an improvement in the margin profile.

After the management change, there’s been a constant improvement, which is clearly visible from the financial data. This is a typical case of a financial turnaround.

How did the turnaround happen?

Controlling the operating cost by opening facilities in a place where they have a good market instead of manufacturing in Coimbatore (where they don’t have any clients).

Restructuring the product portfolio by exiting the products that do not add any value to the company.

Eyeing two acquisitions in two years. One in commercial vehicle space and the other in oil and water pump space in replacement space in four-wheelers and commercial segments in Europe. For all their acquisitions, they will have to spend anywhere between 350-400 crore in the next 3 years.

Continuous decrease in Liability

The company has reduced its debt from 448 crore in 2018 to a much more manageable level of 79 crore in September 2022. In its analyst meeting, the management indicated that they are averse to taking on debt and that they will mostly use internal accruals for their expansion plans.

What’s next? – Grab opportunities!

The company is a leading supplier of instrument clusters for large 2-W players domestically and enjoys a significant wallet share with them. With consistent focus on de-leveraging of b/s amid calibrated capex spends

The move towards increasing digitization of instrument clusters post-introduction of BS-VI emission norms is slated to be a large growth opportunity in the coming times. BS-VI switchover has also benefited the fuel pumps. Sales from these margin-accretive new products formed 40% of 9MFY21 revenues, with further increases in contribution expected in the coming years.

Pricol serves most major OEMs, such as Hero MotoCorp, TVS Motors, and Bajaj Auto in 2- W, Tata Motors, Ashok Leyland, and VECV in 4-W and M&M, Swaraj Tractors, and TAFE in tractors. The expiration of the non-compete clause with the erstwhile partner post-closure of JV has enabled the company to re-enter the PV segment over the past year.

Importantly, it has emerged as the sole supplier to Tata Motors for its PV (most models) and CV divisions. Thus, with new-age electronic clusters in the offering, an increase in content in BS-VI transitions, and an impressive client profile, Pricol is well poised to grow ahead of the industry, going forward.

Display of futuristic products like HUD, E-Cockpit, TFT smart clusters, and an electric tilt cabin system at the recent Auto Expo 2023. Growing presence in PV space with clients like Tata Motors (SOB ~70%), Citroen, etc. Work in progress with 22 EV players (including big and small) for instrument clusters.

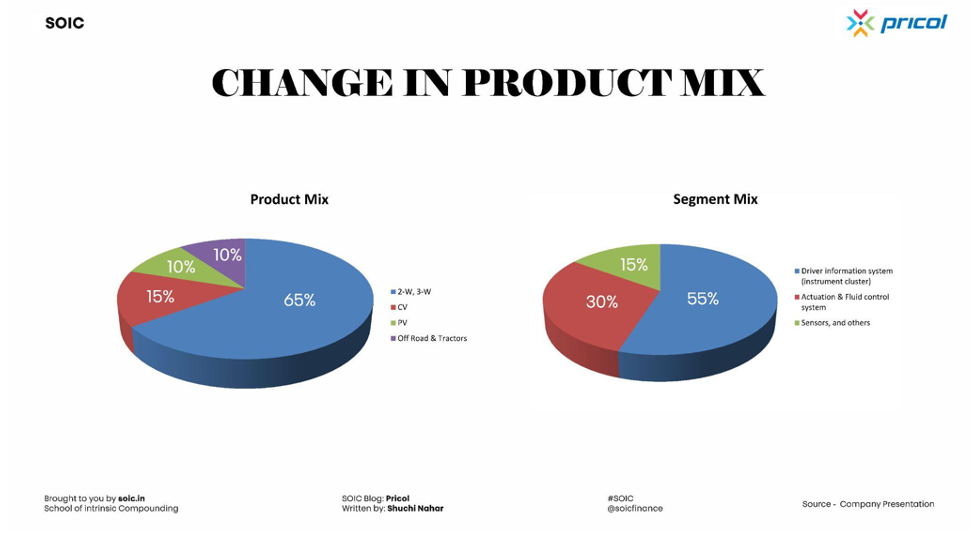

Change in product mix –

Product mix: - ~65% from 2-W, 3-W, ~15% from CV, ~10% from PV, ~10% from off-road & tractors.

Segment mix: - ~55% from the driver information system (instrument cluster), ~30% from the actuation & fluid control system, ~15% from sensors, and others.

The company has won many new businesses across various segments, including next-generation products like Connected Vehicle Solution, and around 10 % of the revenue of FY22 was contributed by the new business.

A recent comment by Management

The management was informed about an integrated circuit (IC) shortage, due to one of its key IC suppliers, impacting overall performance during the quarter. The management believes the worst is behind it and expects healthy growth, going forward.

On Sibros' front, the company said value addition would be in the form of a cloud solution as the company has already been the supplier of telematics for the last 10 years and more than 300,000 units of telematics are already successfully operating in the field. On the BMS front, the company is evaluating conditions in Indian markets and has already received several inquiries from customers.

The company said 2-W, PV contribution during the quarter remained at ~65:35 and DIS/Fluid systems contributed ~65:35. Export was at ~12% of the overall top line.

The management informed about starting mass production of water pumps for Caterpillar The management said DIS ranging from ~300-10,000 per unit with telematics and other software-driven functionalities would be the key driver for the increase in content/vehicle. Currently, ~<5% of the topline is from EV OEMs.

Key triggers to track the transformation of Pricol

De-leveraging of b/s along with the target of being debt free by FY24E. Sweating of assets, healthy cash flow generation, and calibrated capex spending. Growing presence in the PV space with clients like Tata Motors, Citroen, etc.

A new product pipeline and confirmed LoI from customers (including new-age EV OEMs) will help boost sales. New product launches will help boost sales, and PAT will grow at 23% and 24% CAGR, respectively, in FY23-25E. Margins are seen improving to 12.5% by FY25E.

Recent technology tie-ups for the battery management system (BMS) with BMS Power Safe and forays into connected clusters (incl. Telematics) with SIBROS.

Ambitiously aimed topline of 4,000 crores with planned capex of 600 crores in the coming seven to eight quarters, of which ~200 crores for inorganic capex to diversify into industrial clusters to de-risk from the cyclical auto business. Recent technology tie-ups for Battery management systems (BMS) with BMS Powersafe and the launch of cloud services with SIBROS in FY24E. Consistent focus on de-leveraging of b/s amid calibrated capex spends.

Disclaimer: The information provided in this reference is for educational purposes only and should not be considered as investment advice or recommendation. As an educational organization, our objective is to provide general knowledge and understanding of investment concepts. We are not registered with SEBI (Securities and Exchange Board of India) and do not provide any buy/sell/hold investment advice, suggestions, or recommendations, nor do we provide any Portfolio Management Services.

It is recommended that you conduct your own research and analysis before making any investment decisions. We believe that investment decisions should be based on personal conviction and not be borrowed from external sources. Therefore, we do not assume any liability or responsibility for any investment decisions made based on the information provided in this reference.