Privi Speciality Chemicals

Plant Visit & Management Meet Notes

Date - 19th June 2026

Management present -

R.S. Rajan (President), Narayan S. Iyer (CFO), Sanjeev Patil (EVP – Strategy & Biotechnology), plus the technical/project team (Vivek Madhav, Saleem, Usman, Prashant, Ram Subbu – HR head)

Disclaimer - This is only for educational purpose and sharing our plant visit experience to the larger audience. Please think independently before taking buying and selling decision

Privi is not a commodity aroma-chemical maker that happens to have good margins rather it is a vertically integrated waste-to-wealth platform that buys other industries’ effluent (kraft-pulp turpentine, kerosene side-streams, corn-cob) at near-scrap prices and chemically climbs the value chain on every single stream, main product and by-product.

The ~25-26% EBITDA margin that the market keeps questioning is the output of that by-product economics. The next two legs, the “5K:1K” plan and the “beyond-5K” biorefinery are the same playbook applied to new feedstocks.

The visit was less about numbers (those are public) and more about management answering the question they themselves posed: “What is it that brings these numbers?”

We do different things, and we do things differently

This is the company tagline and it ran through the whole meeting. Babani’s broader point was about the generational transition crisis in Indian chemicals: most good chemical names that went public from the 1990s were built by first-generation IIT/IIM founders now in their mid-60s, whose children often have no interest in running plants

Converting a founder-run organisation into a professionalised institution is, in his view, the single biggest challenge facing the sector. He cited SRF and Navin Fluorine as the two that have already made the jump (third generation, professional managers).

Privi’s claim is that it has built the institution from the start:

No family member in any operating, finance, or board function run entirely by professionals; Babani sits at the head “because he knows the business better than all of us.”

Independent board, Big Four audit, SAP S/4HANA, strong internal reviews, clean governance track record.

A multi-year HR transformation (HR = heart response, not human resource), with Ram Subbu (3 yrs Privi + 3 yrs Microsoft) leading it.

Extreme retention / tenure: senior team (Rajan, Iyer) has 12–18 years; ask any manager or GM at the plant their tenure and the answer is ~10 years for 99% of them. Saleem (~25 yrs), Prashant (~15 yrs). A “~30 M2” (manager/senior) leadership pipeline is being formally trained.

Culture described as “family + professional”: a GM can get torn apart at 1:14 pm for a process failure and be served fresh roti by the same boss at 1:45 on the lunch table.

Why is the 25% margin real? At the point where customers make lesser margins than them!

Management’s answer was rather simple -

Givaudan, IFF, P&G, Unilever/HUL, Henkel. These buyers have top-notch technical talent and understand exactly what it costs to make every molecule. Privi has literally presented its growth and EBITDA-margin slides to the #2 in the hierarchy at IFF to a customer whose own EBITDA margin is ~21–22% and said, in effect, “I supply you, and I still make 25%, because I am extremely efficient and I keep rediscovering my own processes.”

This is the right way to underwrite the margin durability. The customers are the audit. If the 25% were unsustainable gouging, this concentrated, technically capable buyer base would have re-sourced or backward-integrated years ago. The fact that even BASF couldn’t displace Privi on Privial is the proof where BASF holds almost 80% of this market

The core moat - by-product / side-stream economics (”Plan B so strong that Plan A always wins”)

This is the heart of the visit and the most important section. Privi’s stated principle:

“Your Plan B should be so strong that on your Plan A you are still in the game. Make your by-products earn all the money, then offer the main product at a fair price. Until somebody cracks the by-product value chain, there is no price competition.”

The hierarchy of what you can do with a chemical by-product/side-stream:

Worst: burn it as cheap fuel (₹30–50/litre — common in Mumbai bakeries).

Second worst: dump it into low-grade products (e.g., cheap floor-cleaner / phenyl fragrance).

Best: extract the molecules and sell them up the value chain.

Worked examples management gave:

Terpene processing: 100 kg of terpene oil yields ~30 kg of by-products. One extracted by-product mixture used to sell at ₹100/kg; Privi now extracts and sells it at ₹350/kg. Volume scaled 30 → ~50 tons/month, targeting 75 tons/month. “30 tonnes of extra material on which you earn ~₹200 extra — do the math.”

Rose-fragrance molecules - three grades: ~$3.0–3.25/kg (bulk), ~$15–17/kg (better), and ~$75/kg (finest). “The difference between eating Chinese at a roadside dhaba vs. a five-star hotel.” A perfumer blends mostly bulk + a little fine. Privi is a fully integrated, large-volume producer of all three, that integration is the margin.

A high-share molecule: the by-products of making it earn as much money as the main product itself.

Alpha-damascone: ~$75/kg, currently only ~2 tons/month; a completely new synthetic route is being developed that could double volumes once cracked.

Galaxolide (musk): Privi entered last into this industry, but with a 5,000-ton plant on latest technology vs. incumbents’ 2,000–3,000 tons and competes despite having no backward integration (it’s crude-oil-based). Edge comes from making side-stream products off the kerosene cut.

We are not L1 (lowest cost). We are L2 or L3. We make very decent margins on the main product but the cream comes from the side-streams.

Raw material & backward integration

Over 70% of the business is pine chemistry, and the key raw material is CST (Crude Sulphate Turpentine) and GTO (Gum Turpentine Oil). The molecules that matter — alpha-pinene and beta-pinene are complex, exist only inside pine trees, and cannot be made synthetically.

Two routes to get pine chemicals:

Tapping pine trees → gum turpentine (GTO). Done by ~100 farmers + an aggregator + a trader. Completely disorganised, unreliable, no price visibility, historically China-centric (Brazil now emerging). Privi got caught on the wrong foot once or twice trying to commit 5–6 year prices on this.

Kraft pulp / paper-making → CST (Privi’s chosen route from ~2010–12). When pine is pulped for paper, the pine chemicals come out as a sulphur-laden by-product with an obnoxious smell (~2% sulphur = ~20,000 ppm). Privi’s core technology brings that down to <1 ppm — turning a foul effluent into fragrance-grade aroma chemicals.

Why this is a near-uncopyable moat:

Privi is the largest single-location CST/GTO processor in the world: 36,000 TPA CST + GTO

It buys CST from 60+ mills, primarily Canada/US → rail cars → port → Mumbai → plant, run by a dedicated ~60-person logistics team. “Not a single mill will float a tender without calling Privi to participate.”

Privi procures 20–25% of global CST/GTO supply - a structural sourcing position no new entrant can replicate quickly.

No purchases from China for 10+ years - Chinese prices are unreliable and contracts not always honoured. Sources from Brazil, Indonesia, Scandinavia instead. (Privi exports to China.)

When the route was chosen (~2012), none of Privi’s own engineers/chemists had even seen CST yet they learned and mastered it from scratch.

Competitive landscape

BASF controls ~85–90% of global citral supply; fully integrated, makes its own raw material, now also in China. Privi competes against this on Privial (a lilac-smelling molecule; ~10–15k ton global market). Five years ago BASF’s commercial head literally called and asked “why are you doing this?” Today Privi contracts this product with multiple large buyers and has out-competed BASF despite BASF’s backward integration.

Privi is present in ~75 products today, heading to ~95–100 (ex-JV), out of ~3,000 known aroma chemicals. Most competitors carry only 10–20. The pitch to customers is “single door for all” 100 products from one doorstep.

Industry now is a closed oligopoly with 4–5 top players. Long development cycles, IFRA/REACH regulatory complexity, and high switching costs make it sticky.

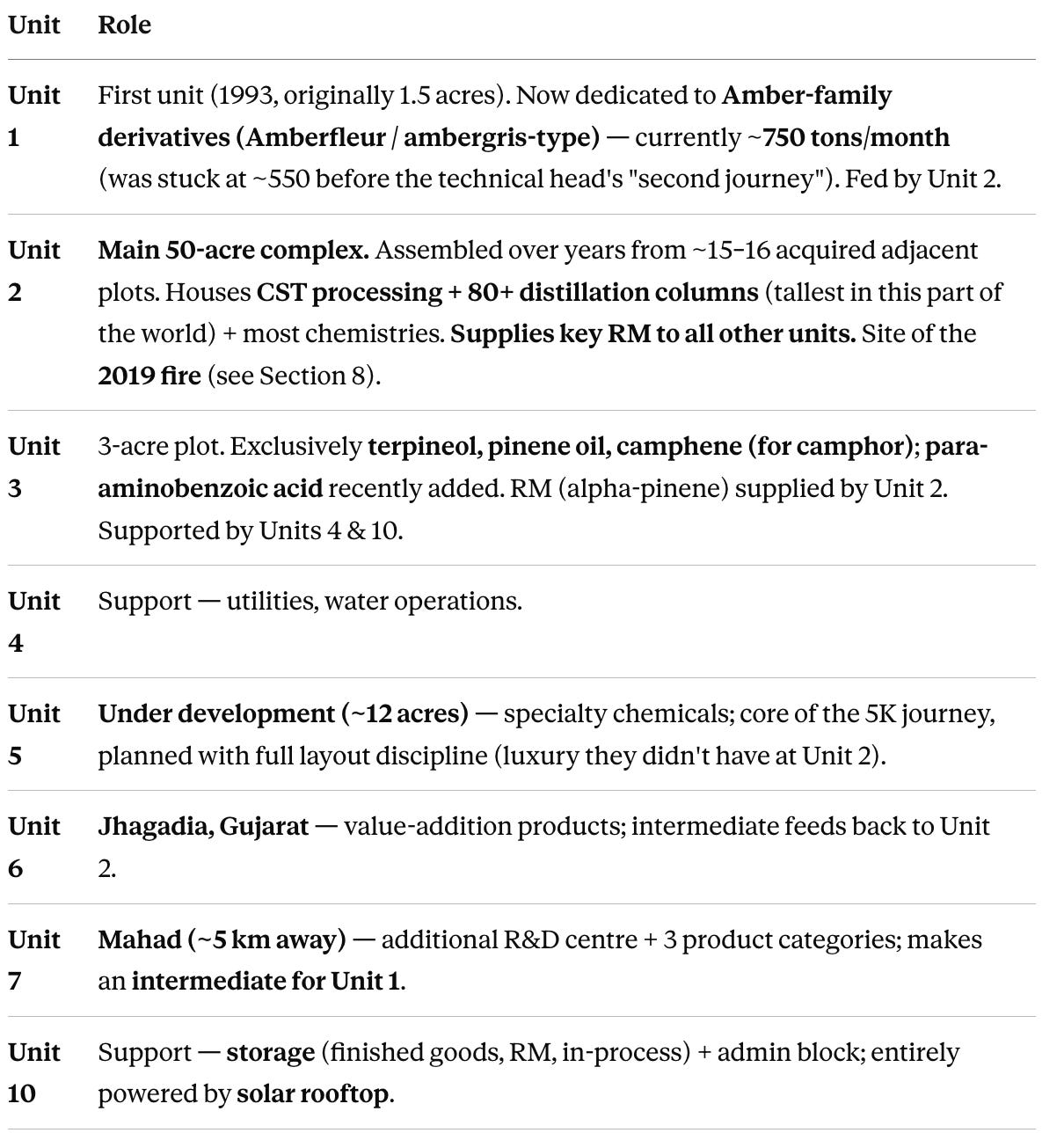

Plant / unit architecture (Mahad complex + Gujarat)

Privi runs 7 units - 4 manufacturing, 2 support, 1 under development

2019 Fire - The Challenge that turned out to be an opportunity

A fire at Unit 2 (caused partly by the legacy layout: hydrogen generation at one end, hydrogenation at the other, with hydrogen piped across the site, and tanks scattered everywhere the result of acquiring 15+ plots piecemeal).

Two gates (one of which Babani had insisted on building on the east side over the CMD’s initial reluctance) turned out to be critical both had tankers burst on them, and without the second gate, fire engines couldn’t have reached.

The rebuild became a redesign opportunity:

Hydrogen generation + hydrogenation consolidated into one corner behind a ~1-foot-thick firewall designed to contain any explosion.

All storage moved underground; tankers no longer roam the site; roads widened; control rooms moved outside the plant.

Restarted in 29 days despite India requiring ~28–29 separate permissions to restart a plant of that size which takes almost a year for most players.

Growth roadmap - the 5K:1K vision

5000 cr revenue and 1000 cr+ EBITDA by ~FY29–30 (~2x current scale), with EBITDA margins sustained around the 25% range.

Capacity build-out:

48,000 → ~72,000 MTPA after 3 phases (transcript said 74,000; the May earnings call says 72,000)

Phase 1: +6,000 MT → 54,000 MTPA, targeted complete by 30 June 2026 (half done at time of visit; rest “a month or two” out). Calibrated ramp-up over subsequent quarters.

Phases 2 & 3 (multi-specialty aroma project): ~12–15 months each; end capacity ~72,000 MT by ~June–Sept 2028.

Capex & funding:

Total ~₹1,200 cr for the journey.

Largely funded by internal accruals; worst case ~₹250 cr incremental borrowing. Peak debt capped at ~₹1,250 cr.

New capacity supports ~₹500 cr of incremental revenue from the existing/near-term product set; the rest comes from new molecules.

Sales happen three years before the plant. Products are sampled from lab → kg → pilot with customers, so by the time a facility is built, demand is already locked. Most new products are customer-requested

New molecules

The near-term specialty additions, all customer-validated:

Maltol & Ethyl Maltol -flavour molecules, currently imported into India; CBAM tailwind (Section 13).

Renewable Cyclopentanone - Privi has proprietary technology; lower price point but very good margins.

Furfural - a building block made from corn / corn-cob (COB) waste. Furfural then feeds 3 downstream molecules incl. methyltetrahydrofuran (MeTHF) and cyclopentanone.

10+ other high-end specialty products.

Strategic logic - waste → wealth. Buy corn-cob crop → make furfural → climb to flavour chemicals and specialty molecules, fully backward integrated, only player of that type. This new vertical is ultimately sized at up to ₹1,000 cr in revenue.

Management indicated that they are also working on the beyond 5K vision for newer derivative chemistries that increases there TAM beyond the current 5K vision. Even if the management is able to click 3-4 of this new chemistries then also they can reach another 5k

PRIGIV - the Givaudan JV

51% Privi / 49% Givaudan SA (world’s largest F&F company; notably, Bill Gates / Cascade is a major Givaudan shareholder

Makes 40+ specialty products exclusively for Givaudan proprietary Givaudan molecules not sold anywhere else, entrusted to Privi specifically for its scale-up and chemistry capability.

Turned PAT-positive in Q4 FY26 (first time).

50 cr additional equity being infused (51:49) for new products/revenue, not backward integration.

~₹180 cr non-interest-bearing trade advance from Givaudan to help cut Privi’s debt and interest cost.

Revenue trajectory: ~₹55 cr (FY26) → ~₹130 cr (FY27E) → ~₹300 cr in 3–4 years. Evaluating additional capex for high-value molecules using in-house tech (potential ~₹100+ cr revenue).

This is the first such dedicated specialty JV Givaudan has done in the fragrance industry. Other MNCs are now in discussion for dedicated-capacity arrangements; IP / data walls between customers are fully set up so a Givaudan relationship doesn’t block, say, an IFF one. IFF alone needs ~1,000 tons/year for its India requirement and would rather buy from Privi than make it. They in the next 2-3 years want to scale this business to max 500 cr types with 20% margin. The main purpose of this JV is to build a long lasting relationship with them and learn from them to build for themselves similar capabilities.

Group restructuring

Proposed amalgamation of Privi Fine Sciences (PFSPL) and Privi Biotechnologies (PBPL) into Privi Speciality Chemicals (PSCL):

PFSPL: Privial, Anethole, Cyclamen Aldehyde (fine & functional F&F).

PBPL: 100% subsidiary, biotech-driven F&F development (the bio-vanillin / green-science engine).

Status: NOC / observation letter received from BSE and NSE; NCLT filing next; approval expected FY27 (Q3 FY27 target).

Purpose: simpler group structure, operational synergies, scalability. (Note: the 20% standalone growth guidance is pre-merger; consol numbers fold in once the scheme is effective.)

Before we go towards conclusion a quick note - The business discussed today, is also part of our TVGP Watchlist under the SOIC Research (India + Global)

The watchlist is a curated universe of around 50 businesses in India + 10-15 businesses Globaly that we track continuously using our internal TVGP framework: Theme, Value, Growth, and Promoters. The objective is not to chase hundreds of companies but to build deeper understanding of a smaller set of businesses across sectors and market caps.

Every Sunday, we conduct a live session where we break down one company from this watchlist in detail, discussing the industry structure, business mechanics, growth triggers, risks and valuation context. Over time, this creates a structured repository of business analysis rather than isolated stock notes. The recording of these sessions are also available in our repository which is also accessible to our subscribers

For readers who enjoy studying businesses this way, the broader watchlist and research library can be explored here: https://www.soicresearch.in/home

Privi’s plant visit reinforced that this is not a margin anomaly waiting to mean-revert but a structurally engineered “waste-to-wealth” platform: the ~25-26% EBITDA is the output of by-product and side-stream economics layered on a near-uncopyable CST sourcing position (60+ mills, ~20-25% of global procurement, world’s largest single-site processor), and it is underwritten by deep process tenure and a customer base - Givaudan, IFF, P&G, Unilever, Henkel and sophisticated enough that their continued sourcing is the audit on the moat.

Thank you for sharing. That's increase my conviction.

Very deep insights, thanks for sharing