PSP Projects: Play on India's Growth Story?

About Industry

If you believe that India's GDP is getting back on its growth trajectory then the Construction industry is going to play a huge role in it as it generates a lot of employment. Whenever the government decides to push their country to growth they start spending on infrastructure as it leads to a multiplier effect. Such projects will provide jobs to labour, new infrastructure will attract developers to build houses, it will attract new retail stores or shops, etc.

India’s construction sector is the world's third largest market and growing at almost twice the rate of China’s and is expected to grow at the rate of 6.4% from FY18 to FY23 reaching a value of $690Bn. Pradhan Mantri Awas Yojana focuses on providing affordable housing to people. As per LiveMint , 5.5 million houses have been constructed, 9.2 million are under construction against the sanction 11.4 million for FY22. Further The Union Budget 2021-22 had allocated 1.18 lakh crore for the Road Transport and Highways, Rs.1.1 lakh crore for railways, and Rs.6,450 crore for Smart Cities.

As of FY21, Gujarat contributes 16.8% to the country’s industrial output which is the major market for PSP projects.

The darkside of the industry is that it has a very bad image as it consists of a lot of challenges. A developer might also need political influence to get contracts, corruptions also exist, if the customers delay the payment the burden is on the developer which leads to higher working capital days, major end customer is government, etc.

About Business

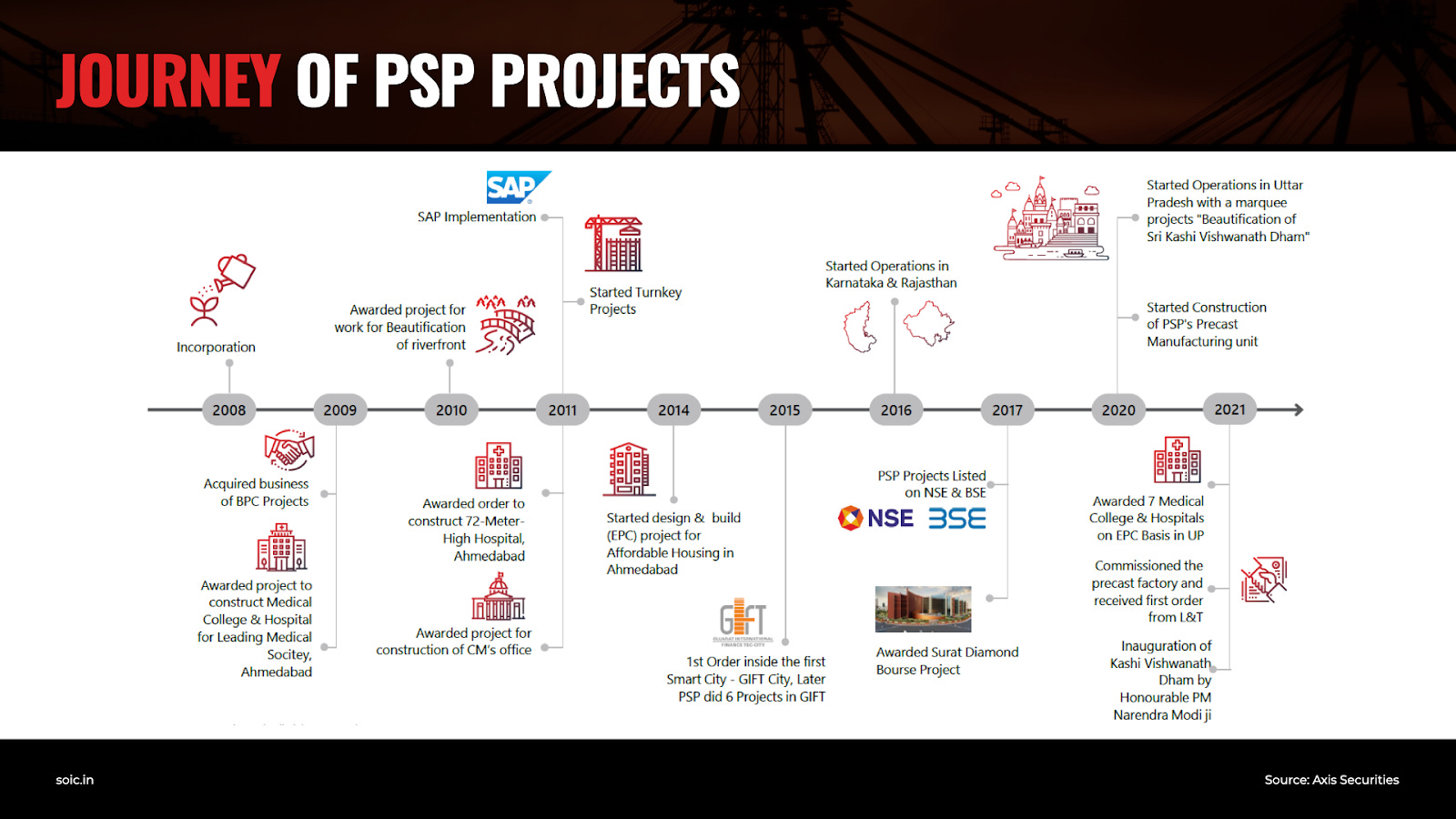

PSP Projects was created in 2008 by Prahaladbhai Shivrambhai Patel. He is the Promoter, Chairman, Managing Director and CEO of PSP Projects with 35 years of experience in the construction industry at the age of 58 years. He holds a bachelor’s degree in civil engineering.

There were two lines which he mentions in a recent interview :

“Mera requirement life mai zaada nahi hai Rs.2 lakh mai khana, pina, aur rehna”.

“Money is not important in the construction business. Quality of work, speed of work, and integrity matters which makes you big.”

Both of these quotes highlight that the promoter is more quality focused rather than money centric which could lead to saving of cost via use of poor material which is the most common problem people face when dealing with construction companies.

The company is in the business of construction and provides services like Design, Construction, Mechanical, Electrical, Plumbing (MEP), Interior, Engineering, Procurement, and Construction (EPC), etc. They have completed 179 projects in its lifetime and currently 45 projects are under execution.

Currently they are majorly into EPC, which means they are responsible for all the activities related to Engineering, Procurement, and Construction (as the name suggested) . EPC contracts are generally fixed on with raw material variation clauses which allow passing on the cost . Further all the funding is done by the government only the execution part is left on the contractrator like PSP Projects.

In the order book mix, EPC contracts contribute 60%, Turnkey Projects at 31% (Under “Turn”-“Key” projects the contractor has the whole responsibility of making the project ready till end step and handover the project to the owner so that they can “turn the key” and start using the premisses immediately), and 9% comes from Civil Construction. One thing to keep in mind is EPC contracts are the highest margin among three and turnkey projects being lower than EPC contracts.

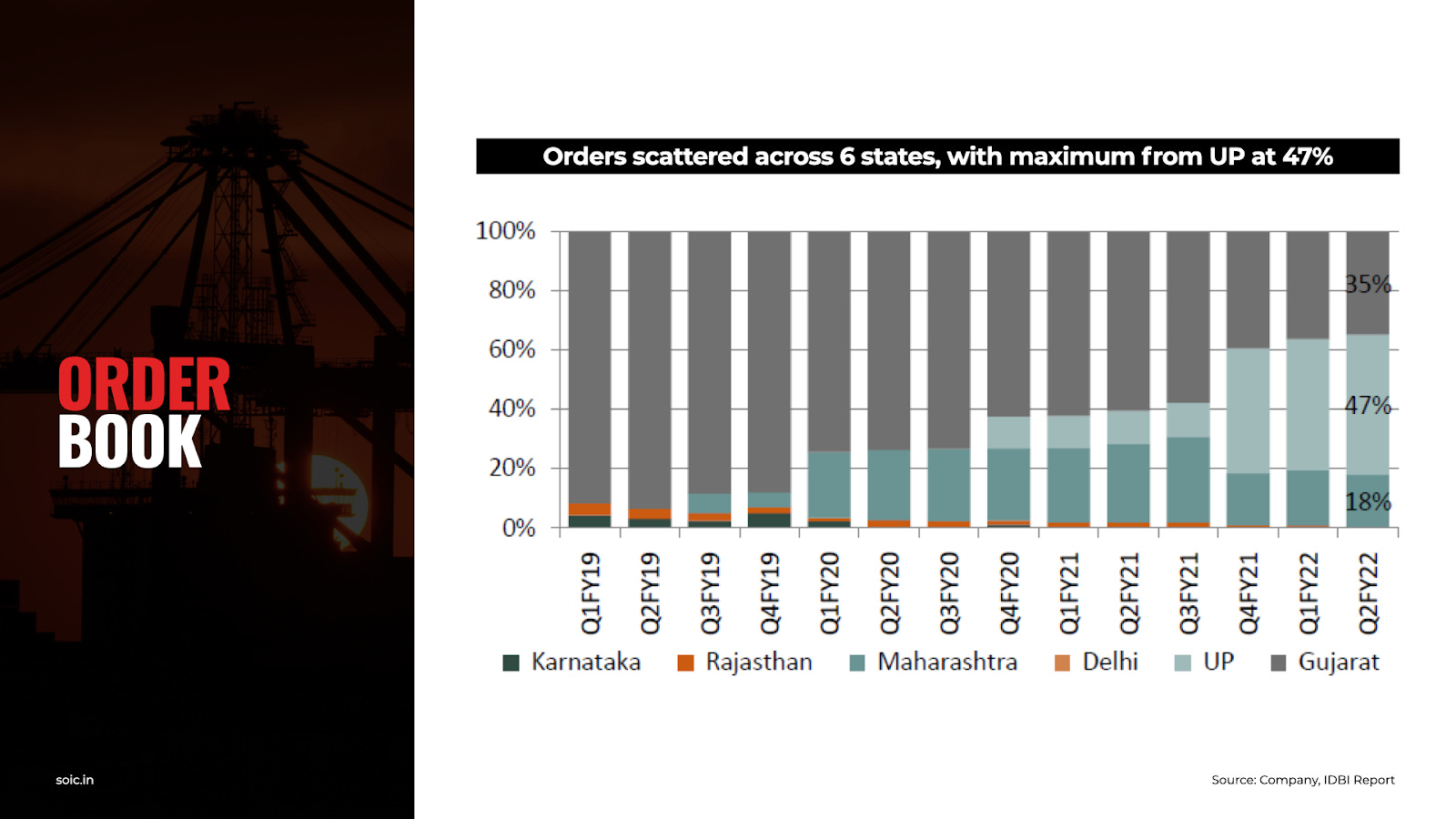

They are based out of Gujarat, which contributes 31% of the order book and around 50% of the book is from U.P. Other markets where they are present are Rajasthan, Karnataka, New Delhi, and Maharashtra.

Management on diversification

The real estate market runs on selling and is openly driven by the sell market so it is a little risky. As you don’t know the client and developer it will be risky then if they are capable to pay on time or not. Projects in which finance is dependent on sell companies believe that they should be selective on ground. (Q3FY18)

The biggest client of PSP Projects is the Government which contributes 63% (39% + 24%) of the projects and total order book stands at Rs.4121 crores as of FY21 and at Rs.4,008 crores as of 9MFY22 with average length for projects at 30-36 months.

The company's average ticket size has increased from Rs.8 crores in 2013 to around Rs.100 crores now. For every project they take 10% beforehand to fund their working capital.

PSP projects also had a USA subsidiary which they had setup for a specific project but as the project got completed now the management has taken the step of disinvestment and in Q3FY22 they announced the completion of the same. They sold the stake at $10,000/- and also received the Rs.2.14 crores loan which was provided.

Projects

PSP projects has executed many famous projects like IIM Ahmedabad, Surat Diamond Bourse, etc. and has marquee clients like Nestle, Reliance, Zydus, etc. who also give them repeat orders.

Surat Diamond Bourse (SDB) project

The promoter reached out to the committee of SDB and asked for the opportunity to present and they got shocked because they had done one high value project in their history which was only Rs.250cr and SBD project is around 1800cr. But the Promoter asked for the change to present. There he convinced the people that he would divide the project into three projects consisting each of 22 lakh sq ft (66/3 lakh sq ft) and he has done a project of 18 lakh sq ft building. Got the project in 2017 (which is the world’s biggest office complex on a single basement) and will be completed by February end 2022. After finishing this project, they would enter into the league of players with project size of 2000-2500cr (from 500-800cr currently), which means they would qualify to participate in bids like Central Vista, Airports, etc. In the view of schemes like ‘UDAAN’ (Ude Desh Ke Aam Naagarik) which was started in 2017 to bring in 100 new airports and 1000+ new air routes in the country, this made PSP Project interested in entering airport construction.

Other projects

Another breakthrough project which the company had was the setting up of Zydus Hospital. In 2008, owner of Zydus Cadila had a CSR activity project in Gujarat for setting up a hospital. The 1250cr capacity project was the first project which got MCI clearance in 1 years which generally takes 2-2.5 years. This helped them build a good image in the market.

Another work of excellence was their diary project Diary project in Karnataka which they finished in 150cr in 18 months whereas the average completion time by competition was 2.5-3 years.

PSP projects was also able to get 6 out of 8 building projects in the GIFT CITY in Ahmedabad, Gujarat.

The Central Vista Project

Currently the future revenue driver is going to be the Central Vista Redevelopment Project which included development of Parliament building, redevelopment of Supreme Court, etc.

The project is of around Rs.15,000-20,000 crores out of which two projects have been allotted in which PSP Project could not participate as their SDB project was not completed. The two allotted projects were given to Shapoorji and TATA.

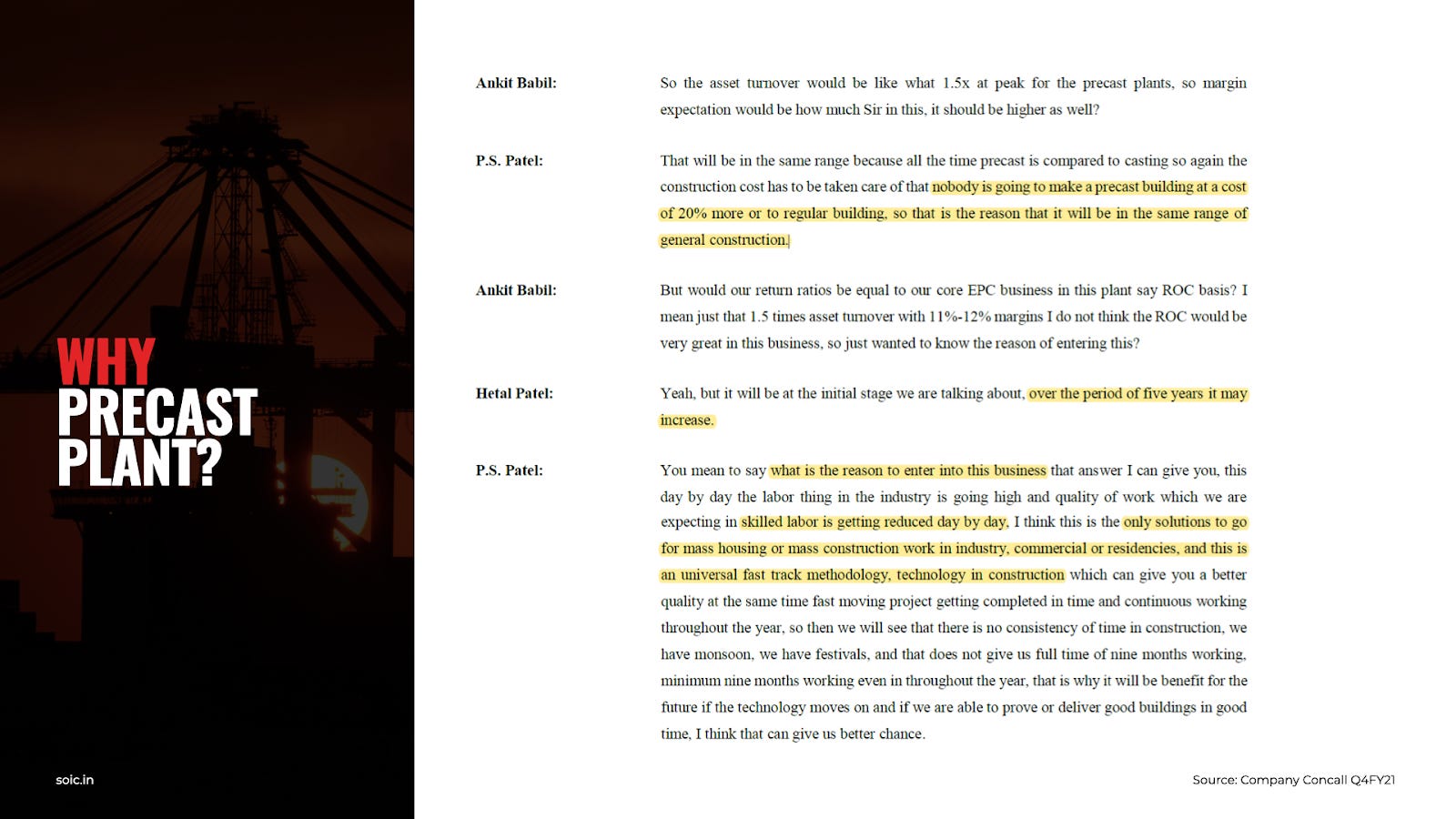

Precast Plant

Management had decided to set up a precast plant with capacity of 3 million square feet in Sanand, Gujarat, but in Phase 1 the capacity will have 1 million square feet capacity but as the land is of 60 acres it can add additional 2 million square feet capacity. The plant is now fully functional and has also received its first order from L&T worth Rs. 51 crores with the deadline of June 2022. The total capex done for the plant was around Rs.109 crores.

The plant will mainly produce precast material but they also plan to make beams and columns, piers, noise barrier walls, underground water tanks, etc, which they can sell to other players as well.

Precast is the raw material for doing construction work. The difference between Precast and Cast (that is on site putting of cement) is that Precast is prepared in factories and then transported to the site. This helps in saving time and one can prepare in advance and not wait for the cast to dry and gain strength (which takes around 25-30 days). It requires less labour as precast is more machinery driven and quality checks can be maintained. Finally it is also cost efficient if down at a large scale.

Precast is technology driven and hence requires technical knowledge of management which could be difficult to find with unorganised players. Plus, it comes with logistics costs.

The plant is not going to be margin beneficial but will help in reducing time and also help in reducing dependency on labour. Management believes that by reducing time for execution they would be able to get pricing power in future by showing their past performance. But one thing to consider is that even a competitor can come up with a precast factory if they start to realise that the benefits are worth it. This means that management’s idea of pricing power in future might not be true as competitors would enter the market.

Risks

Aggressive Growth: If they take a project outside of their capacity to execute then the company can fall in trouble.

Long Working capital days: This is the nature of this industry where all the players have long working capital days and there is nothing much the management can do about it.

Dependence on Government: The biggest client of PSP Projects is the Government which contributes 63% (39% + 24%) of the projects. Plus many of the government projects are generally fixed price contracts which makes it difficult to pass on raw material cost unlike in private contracts.

4) Execution risk: When one is analyzing PSP Project they should reduce the order book by 15-17% because their projects have been stuck and management is finding it difficult to execute.

First, Bhiwandi project which is under the Pradhan Mantri Awas Yojana. PSP Project triggers the escalation clause (which is to pass on the raw material price increase). So, management either wanted to trigger an escalation clause or terminate the contract but the Government did not agree, hence the matter went to arbitration where PSP won but now the Government has moved to court. They have already spent around 7-8cr on the project plus there is a 6.73 crores bank guarantee with the government which leads to total 13-15 cr loss.

Second, Puntarpur Project under Pradhan Mantri Awas Yojana where around Rs.10 crores have already been spent is stuck because the customer is not paying.There is no dispute here like in the previous project but the delay in payment in due to the tenants have delayed the payment to the customer. Management has also received a letter from the customer company that they are going to pay Rs.8 crore. So far the management has spent around 30 crores.

5) Keyman Risk: Currently the company is one man show dependent on Prahaladbhai Shivrambhai Patel. But management is looking to hire a CEO to professionalize the top management.

6) Geographical concentration: 50% order books are from Uttar Pradesh and second largest geography is Gujarat which contributes 31%. But this geographical concentration is a double edged sword - On one hand due to concentration they are able to utilize their asset better which led to PSP projects having good asset turnover and return ratio but as they start expanding to different geographies their assets would increase and the incremental asset turnover ratio would fall.

7) Aggressive bidding due to competition: On competitive edge management says that the bigger players like L&T, Shapoorji, NCC, etc. are not a threat to them as PSP Project works in a niche area as other players are not interested in smaller projects. But this contradicts their action of increasing average order value. Plus one can notice that management has mentioned various times that they have faced competition from above mentioned players.

Valuation

To understand the valuation for this business we like to provide a snippet from one of the concalls of PSP Projects:

As the image above shows that the company currently trades at the market capital which is equal to their revenue in next two years which matches with the management guidance of top line growth of 20-25% with EBITDA margins around 12-14%.

This means the business is cheap but the question to ask is whether such business always remains cheap?

Medium PE has been around 18 times with highest at almost 40 times and lowest at 9 times. Currently it trades between 11-12 times earnings. Such business definitely cannot be a long term holding due to the nature of the industry but one can ride such opportunities for short term purposes. As there is clear revenue visibility for next 2 years, one could expect some rerating as they start executing and book revenues going forward.

Disclosure: Nothing on this website should be construed as investment advice. Please consult your financial advisor. We are not SEBI registered Analysts/Advisors. We are not accountable for any loss or gains that might occur to you from this or any analysis on the website. The author and SOIC both DO NOT own the stock in their portfolio at the date this post was published.

About the Author

Arjun Badola is a law student who has interest in analyzing businesses. He shares his thoughts on investing via his blog and twitter. In case you have anything to discuss related to investing, feel free to reach out to him.

Blog: arjunbadola.blog Twitter: @badola_arjun