Refractories: Proxy to Steel Demand

10 mins readPublishing Date : 2022-02-08

Refractories: Proxy to steel demand

If you have been following SOIC for a long time you would be now aware that we prefer niche industries with consolidated profit pools like Gold Lending NBFCs , Music licensing, Steel Tubes , Bearings etc. Hence, today we bring analysis on another industry with consolidated profit pools that is Refectories.

What are refractories?

Refractories are materials which are crucial for manufacturing any item which is made in temperatures above 1,200°C because refractories are highly resistant to heat. So, if we put this refractory material into the inner wall of the machinery which produces the item requiring excess heat, like manufacturing of steel or glass, then it would protect the machinery from getting melted from the heat and curtail the heat within the inside limits of the machinery.

The refractory product is able to sustain such heat and prevent the outer machine/equipment from melting because of its characteristics it gets from an element called magnesite. This element is mined, crushed, and later burned under 1,800°C to bring in the refractory product characteristics. Further it is mixed with material called binders (which is generally used for shaping the product) and made into various forms like bricks. Once they are made into bricks, they are again burnt at the final stage depending on where its application is. Refractory products come in two forms: Shaped and unshaped. Forming them into bricks fall into the shaped category whereas products like mortars, castables, gunning mixes, etc. fall into the unshaped category.

If you are finding it hard to understand the above process it’s okay, all you need to know is that – refractory is a product which is crucial for producing any items which is made through extreme heat as refractory will protect the interior of that machinery. You can also refer to this video for a detailed explanation.

They form a very minimal part of the total cost being around 0.5-2% but the dependency on this product is extremely high, and many industries cannot produce their product without refractories. The replacement cycle for refractories depends on industry to industry but specific to steel it is around 1-2 months.

Currently more than 70% of the demand for refractory products comes from the steel industry and for 1 ton of steel 10 kgs and 12 kgs of refractories is used. Hence, growth of the refractory industry is linked with the steel industry. But despite the dependency refractory companies don’t show qualities of a commodity company as their gross margins do not get affected as they are able to pass on the fluctuation of raw material cost, which represents the pricing power for such a sector.

Therefore, this sector is like selling shovels during the gold rush if you believe that the steel industry is going to do well in the near future, as refractories are necessary products needed for any steel manufacturer.

Industry structure

Refractory industry has a production capacity of 1.5MT with a market size of around Rs.10,000cr where, as mentioned earlier, more than 70% of the demand comes from the steel sector and the rest from glass, cement, etc.

The industry is dependent on China or imports from parent MNCs for raw material like Bauxite and Magnesia and that is why due to supply chain issues this sector was affected a lot. There was a sudden increase in container cost (going up by 5-6 times) and raw material cost.

RHI and IFGL are the two players who have gained market share from FY15 to FY21 with IFL being the highest gainer of 0.8%. On the other hand, players like Vesuvius, Tata Dalmia, etc have lost market share. Industry remains fragmented with the largest player barely having 16% of the market share.

Steel demand

There are a lot of macro tailwinds coming in for the steel demand like PLI Scheme, infrastructure projects, Jal Jeevan Mission, etc. In the next 4 years, 38 million tonnes (MnT) of capacity are coming to fill the gap of global demand after China’s meltdown which amounts to a 35% increase in capacity from FY21 levels. Plus, consolidation happening in the steel sector is making the bigger players stronger.

The Indian Steel sector is the second largest steel producer in the word with an output of 9.8 MT and now The Indian Steel Ministry targets 300 MnT per annum steel capacity by 2030. National Steel Policy 2017 had stated its objective of taking per capita steel consumption to 160kg from 60kg and steel production 255 kgs from 109kgs currently, by 2030. Further, to reach the target of a $5 trillion economy by 2025 around $1.4 trillion money should be spent on infrastructure (Source: Annual Report FY21 RHI Magnesita).

As mentioned at the start of the post, this industry has consolidated profit pools, which is visible from the market share chart shown above, where large players dominate the market by having more than 56% of the market share. The reason being the entry barriers the industry brings in.

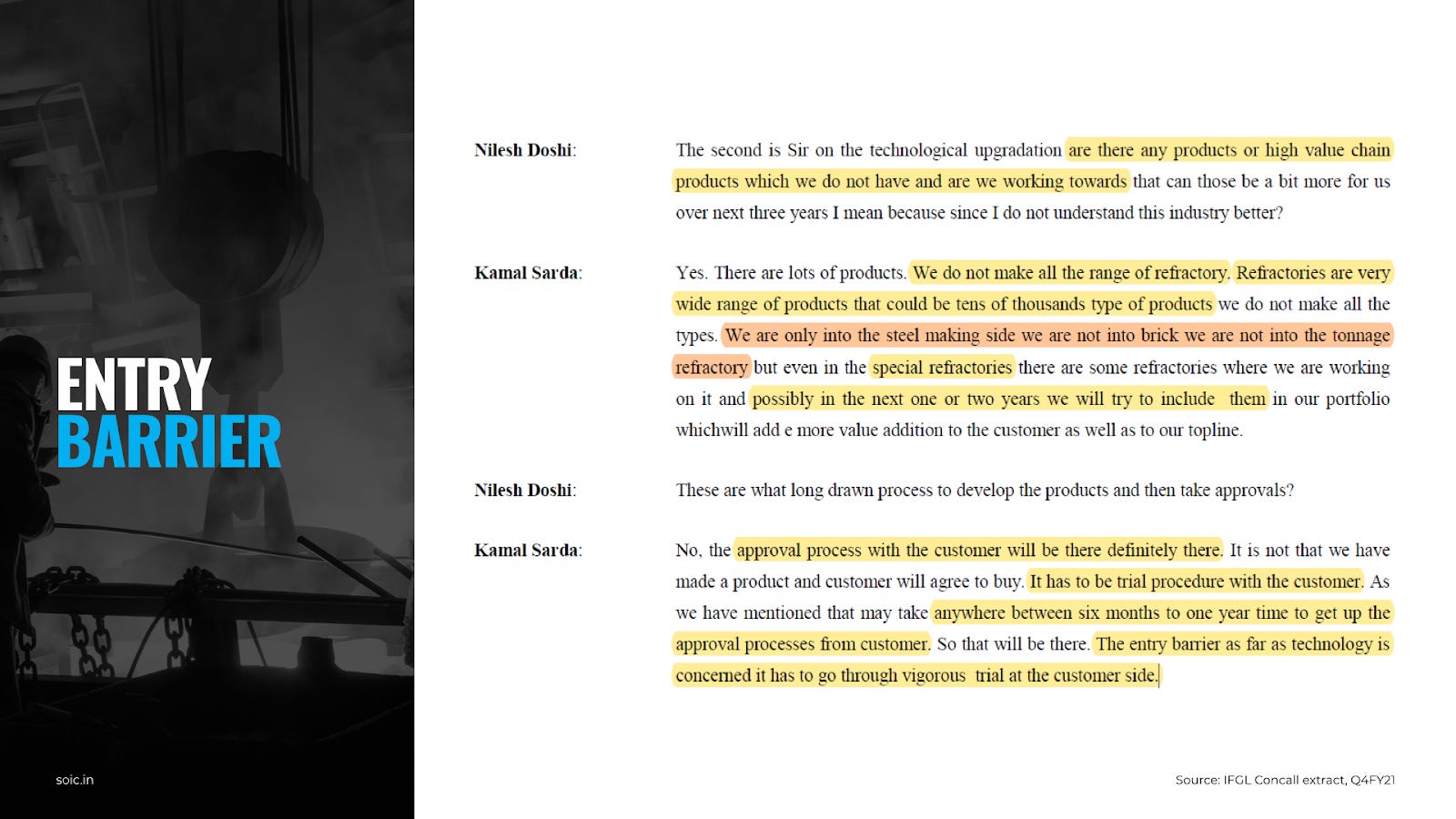

Refractories form a very minimal part of the total cost of steel production companies, it being around 0.5-2% but the dependency on this product is extremely high. Therefore, relationships with the customers are more important than giving cheaper products. Further as the demand for refractories is constant and should not be inconsistent in supply, as it would affect the customer’s business, they prefer dealing with well-established players in the sector. This building up of relations can take up to 4-5 years to get into the business for steel plants. Lastly, large players also have access to better technology and material due to their global parents.

Every capex goes through approval from each customer which takes from 6 months to 1 year.

China’s action to reduce carbon footprint has led to lower steel production combined with removing export rebate on steel which has created a supply gap in the global market for steel demand and that is where India comes in.

Whereas, Indian export of steel has been increasing.

Further there are other few macro events like $1 trillion USA infrastructure bill, recovery in Europe steel demand, Europe steel demand recovering after 2-3 years of muted demand, et.c

About RHI Magnesita India

RHI bought 69% stake in Orient Refractories Ltd (ORL) in 2013 making it their subsidiary and in 2017 RHI became the largest refractory player in the world after it merged with a Brazilian company called Magnesita. Finally in 2021 RHI Magnesita (The merged entity of RHI + Magnesita) decided to do another merger this time with their Indian subsidiary ORL, hence today the name got changed and RHI Magnesita got listed via M&A deal.

If you visit ORL’s website, they have provided the list of product they offer (reproduced below):

Isostatically Pressed Continuous Casting Refractories

Slide Gate Plates

Nozzles and Well Blocks

Tundish Nozzles

Bottom Purging Refractories and Top Purging Lances

Slag Arresting Darts

Basic Spray Mass for Tundish Working Lining

Castables

Website also mentions that these products are “custom made to suit the casting conditions and grade of steel being cast”. Their clients included names like SAIL, TATA, Jindal, Usha Martin, Lloyd, etc. As of FY21 the company has a production capacity of 130,000 tonnes of refractory products per annum.

One big advantage of the merger was getting a secured supply chain. Like we saw with Prince Pipes where their deal with Lubrizol protected them in procuring raw material where unorganised players struggled. Similarly, RHI fulfills around 70% of its demand from their own raw material plants which they have across the world. This brings stability for ORL because India is the largest market for RHI.

Merger: Orient + RHI Clasil + RHI India

The RHI Magnesita’s plan is to make India the manufacturing hub and export from here. They have also set up a new R&D centre at Bhiwadi for the same strategy from where they plan to launch new products. They believe India as a strategic market for future growth, and they are ready to take the benefit of the government scheme (Make In India) to increase manufacturing capacity here. RHI already had a subsidiary in India called RHI Clasil, therefore, to reduce complications and increase synergy between the subsidiaries they decided to merge them. One thing to keep in mind would be that the margin of the new entity is lower than Orient Refractories because of merging with a trading company that Is RHI India, but still ahead of its peers.

RHI Clasil’s Vizag plant is running at 90% utilization therefore they have planned a capex addition of 25,000 tones at the cost of Rs.50 cr which should be completed by Q3FY23 (Expansion towards Alumina bricks which has less heat absorbing capability than Magnesia bricks and are mostly used in EAF & BF steel manufacturing process).

As per parent RHI’s latest annual report, India and China combined contributed around 16% to the topline in 2020 which was 15% in 2019. Parent is also open to acquisitions to increase their market share in India and getting into full line solution contracts (providing all refractory related needs to the customer). Further parent could also provide technology for specialised value products to the new entity which earlier only RHI Indian subsidiaries had.

Capex & Import substitution

RHI Magnesita is very ambitious for their growth market this time and has announced to double their capacity in India from 1.42 lakh tonnes per annum to 2.8 lakh tonnes by the end of 2023. Management has set a target of Rs.1700 cr sales by FY22 and Rs.3800 cr target by FY25.

They will be doing brownfield expansion coupled with inorganic growth via acquisitions for which they have set out Rs.450 cr. Management has also confirmed that they have a target of 3-4 acquisitions which should happen in the coming 6-12 months. The capex is being spent mainly on three things: Vizag capacity expansion of 25,000 tonnes at Rs.50 cr (will talk about later in this post), new R&D centre at Bhiwadi + addition of new value-added products, and Cuttack plant.

Players within the refractory industry have adopted the practice of making refractories with recycled raw materials which helps in almost saving 30% cost with reducing dependency on imports. Such material is not easily available and hence not that easy to adopt this practice of using recycled material.

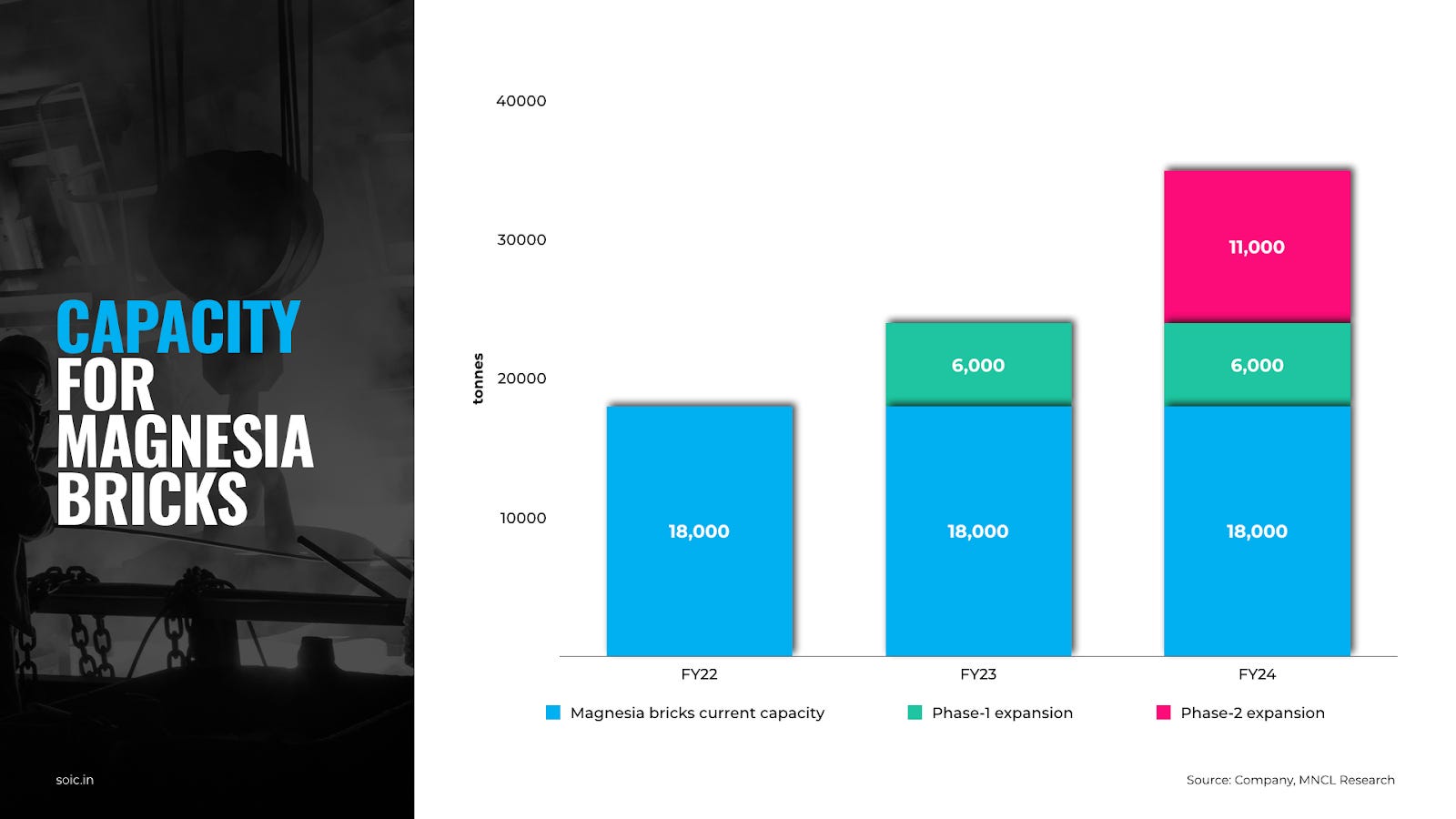

RHI Magnesita India has also announced their plans of setting up a plant for recycled material at their Cuttack plant, where they would recycle magnesia bricks. This plant was bought by Orient Refractories in 2019 which has the production capacity of 10,000 tonnes per year but through debottlenecking they have expanded it to 18,000 tonnes, further they plan to expand to a capacity of 35,000 tonnes in next 2 years. This capacity will be used for making Magnesia brick in India which will help the company get full line contracts i.e. Total Refractory Management services to customers as it completes the product basket. Earlier they couldn’t because importing Magnesia bricks would not be lucrative enough.

Further, making it in India would reduce the cost hence, attracting more customers. Dalmia OCL Refractories is setting up capacity for Magnesia bricks in a phased manner which will be the largest plant in India with 108,000 tons capacity.

More than 70-75% of the 300,000 tonnes of domestic demand for Magnesia bricks is catered by imports from China, which shows the opportunity size available for this high value product.

From the margins point of view RHI stands at a better position compared to its peers even after the merger which led to reduction in margins. Merger reduced the margin because Orient refractories got merged with a trading company i.e. RH India. But increased use of recycled raw material and import substitution should help in increasing the margin in future.

About IFGL Refractories Ltd

IFGL Refractories Ltd is mainly into specialised flow control refractories like isostatic, slide gate, continuous casting refractories where they command around 12-15% market share (6-7% of total market) and cater mainly to the steel sector. With no plans to enter new segments except the bricks business but that will lower the margin segment. Clients of IFGL include JSW Steel, Tata Steel, SAIL, ArcelorMittal, etc. They also have three international subsidiaries- EI Ceramics (USA), Monocon (UK), Hoffman (Germany).

IFGL did sales of Rs.1022 cr in FY21 out of which sales from subsidiaries were Rs.373 out of which 30% is contributed by EI Ceramics, 54% by Monocon, and 15% by Hoffman.

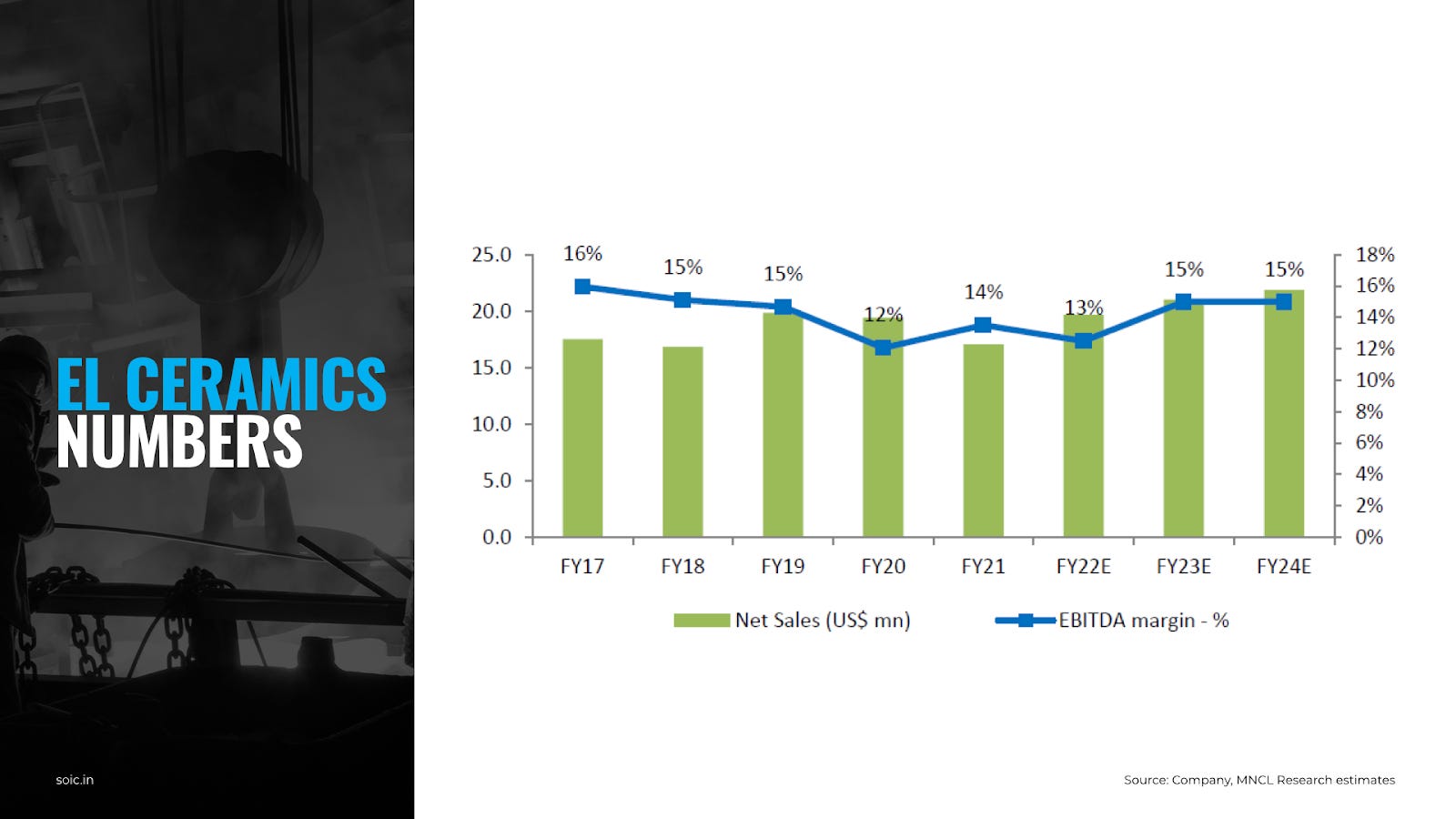

EI Ceramics with an utilization rate of 65%, is going to be a direct beneficiary of the $1 trillion dollar US infrastructure bill. But this is a very competitive market where there is no pricing power, and they have to match with the competition.

Monocon is their largest subsidiary with around 60-65% utilization. If the European market picks up after continuous 3-4 years of no growth, then it is going to be a beneficiary of it. Further, once the supply chain issues and freight cost increase get resolved slowly the margin would come back to normal.

Hoffman Ceramics is the worst performing among the three the reason being it having product acceptability issues. It is into manufacturing of filters which are used by foundries. Demand for their product is largely demand in the automobile industry hence, they have been performing poorly.

The margins for subsidiaries are going to be low compared to domestic business and management is not guiding for any improvement in margins here.

Capital Expenditure Plans

Vizag Plant:

In September 2021, IFGL had completed the phase 1 of their Vizag plant capex which they set up for Rs.30 cr with a capacity of 48,000 MT per annum, for producing Monolithics and Pre-cast products. The final phase of capex for the Vizag plant is expected to be completed by Q1FY23.

This plant is near to port which provides it a location advantage for exporting products, but management has said that as of now Vizag plant is majorly for domestic demand. Further this plant provides better access to IFGL towards their south market especially its customers like Vizag Steel and JSW Steel.

IFGL also has plans to launch new products from this plant such as lances which are used for removal of waste material from liquid steel and manufacture snorkel which is used for degassing the steel. Both of these products are going to act as import substitution products for the company.

“ Vizag capacity addition will result in a turnover of somewhere around Rs. 100 crores to Rs. 120 crores, depending upon the product mixes which we sell. It should reach optimum levels in 2-3 years. “(Q2FY22)

Management is also doing a capex of Rs.10cr at their old Kalunga plant and Odisha plant combined with some debottlenecking. Management guides that the revenue potential from Greenfield capex is generally 3-4 times where from Brownfield is 6-7 times.

But one has to remember all this capex being done by the company will take time to realize due to their industry structure:

P2P: Ratio Analysis

Looking at the gross profit margins (GPM) of peers we can see IFGL Refractories command the highest GPM among them, which indicates some pricing power with IFGL or lower cost of production.

When we look at the numbers, IFGL has lesser cost on raw material at around 47% of the sales compared to RHI at 67% & Vesuvius India at 59% therefore, it is able to command higher gross margin and I feel it's less about the pricing power because management has indicated in the concalls that the market is very competitive.

But when it comes to EBITDA margins, IFGL has the highest Selling, General, and Administrative expenses at 14%, followed by Vesuvius India at 11%, and RHI at 1%. That is where RHI beats the peers and commands higher EBITDA margins.

Coming to Return on Equity (ROE), by doing a DU Pont analysis of ROE we can understand why RHI has a double digit ROE at 17% whereas, IFGL at 7%, and Vesuvius India at 6%.

Always the reason behind a higher ROE is preferred to be either due to higher net profit margin or Asset Turnover because higher ROE from Financial leverage does not include debt in the formula. Therefore, a business can inflate their ROE by taking more debt (but that is not the case with RHI as their debt to equity 0.07%)

The most prominent reason here for higher ROE is higher Net Profit Margin of RHI with an average of 11.8%., followed by Vesuvius India at 9.6%, and IFGL at 5.2%.

IFGL management is currently planning to do a one time write off of goodwill which requires NCLT approval. If that happens then asset turns and net profit margins will also improve (one time hit on goodwill, lesser amortization expenses in the following years) will improve and that will lead to improvement in ROE as well. But management has clearly mentioned that even reaching NCLT for approval will happen next financial year. Therefore, it’s going to take quite a time.

Risks

Cyclicality: More than 70% of the demand of the refractory industry comes from the steel segment. But still the nature of cyclicality is not like a pure commodity player; rather , players in this industry are able to maintain their gross margins and are able to pass the cost with a few quarters gap.

Raw Material: There is huge dependency for raw material in China, which is slowly getting mitigated. IFGL sources 50% of raw material from China compared to RHI with 20-25%. COVID pandemic has led to an increase in freight cost substantially and disrupting the supply chain.

Forex Risk: As these players in companies do a lot of international transactions either with their parent MNC or subsidiaries, any forex change can come in as risk.

Valuation

Before valuation, business analysis comes first. If a business doesn’t qualify your business filter, then valuing the business becomes more difficult.

Out of the three listed players in the refractory industry, RHI Magnesita India Ltd only qualifies for my business filter. IFGL failed at the ratio analysis and Vesuvius India at disclosure level.

IFGL Refractories could get interesting after 12-18 months when they write off the goodwill but till then it would only be in my watch list.

Looking at RHI it is a business with end customers having deep cyclical earnings, trades around 38-40 PE multiple, capex being announced to double the capacity, and ambitious target of 3800cr sales by FY25. However, some of the other MNCs in this space like Honeywell or Cummins India (through unlisted entities?). Which have made India a low cost export hub and these MNCs are getting a multiple of more than 50 times earnings. RHI needs to execute and grow its earnings and the luck (steel sector) has to favour them for any material re-rating to occur from these valuations.

Disclosure: Nothing on this website should be construed as investment advice. Please consult your financial advisor. We are not SEBI registered Analysts/Advisors. We are not accountable for any loss or gains that might occur to you from this or any analysis on the website. The author and SOIC do not hold the stocks in their portfolio at the date this post was published.

About the Author

Arjun Badola is a law student who has interest in analyzing businesses. He shares his thoughts on investing via his blog and twitter. In case you have anything to discuss related to investing, feel free to reach out to him.

Blog: arjunbadola.blog Twitter: @badola_arjun