Safari Industries- All Bagged up to Travel Miles & Miles

SAFARI- All Bagged Up to Travel Miles and Miles

As we can see after covid, people are more excited about weddings and vacations that are around the corner. Brands like safari will play an internal role indicating that recovery and demand momentum. Being an investor, we are always inclined to find some hidden gems that are known by all but understood by none. As the economy opened, people are more inclined to spend on vacations, tours & trips. Weddings that have been delayed due to covid are all lined up and kids who were relaxed about not going to school – colleges are happily flaunting their new bags after their long vacation. Many employees are excited (maybe not) as offices reopen and they have to move out of their homes accessorising themselves with some stylish affordable laptop bags or backpacks.

So, to understand the actual scenario of the luggage industry lets understand Safari – A well known brand which caters the need of mass with their pocket friendly & exclusive products. The company focuses largely on the economic segment and benefited from a weakened unorganised sector due to GST implementation and pandemic related disruptions. Shift in customer preference to branded hard luggage from soft luggage has also benefited Safari in capturing further market share in the industry.

Safari was incorporated in 1980 by Mr. Mehta and family. The company was taken over by Mr. Sudhir Jatia in 2012. It manufactures and sells luggage under the brand, Safari. Safari is one of the fastest growing luggage brands in India with a market share of 24% as of FY22 (up from 10% in FY15). Expansion of distribution channels, introduction of new SKUs and entry into new product categories has resulted in consistent rise of market share over the last few years.

Basic Terminologies

1. HL – Hard Luggage

2. SL – Soft Luggage

3. PP – Polypropylene – (Raw material) Polypropylene luggage is made from thermoplastic polymers through the chain-growth polymerization of mono polymers. They lie between polycarbonate plastic and ABS luggage which gives them the best of both sides. They are more durable than ABS and lighter than polycarbonate luggage.

4. PC – Polycarbonate – (Raw material) Polycarbonate luggage offers ample impact resistance, durability, scratch resistance and water resistance. Plus, it's lightweight. This makes poly a top option for both checked luggage and carry-on. Polycarbonate luggage travels well on road trips, too -- the suitcases are easy to get out of a car trunk.

5. SKU – stands for stock keeping unit

Business Model

Safari’s DNA underwent a paradigm shift after Mr Sudhir Jatia (CMD) bought a majority stake (77%) in May 2012. Mr Jatia is an industry veteran with more than 28 years of experience in the luggage industry. An ex-MD of VIP Industries (served from Feb 2007 to April 2010) he instituted various changes like - Rationalizing product portfolio & eliminating non-performing SKUs. Introduction of SKUs in CSD segment & foray into PC manufacturing.

Safari’s market share is up 2x in 7 years

Product Profile

Safari has a diverse product portfolio comprising 800+ SKUs across HL, SL, backpacks, and school bags. The distribution network is well entrenched with 9,300+ customer touch points covering CSD, modern trade, MBO, EBO, E-commerce and institutional segments.

Safari’s manufacturing plant is located at Halol in Gujarat, wherein capacity expansion is lined up by incurring capex of Rs. 500mn. While Hard Luggage (~41% of sales in FY21) is manufactured in-house, Soft Luggage is outsourced from China (imports were negligible during the pandemic), Bangladesh and India.

Company’s will be enhancing their hard luggage manufacturing to 525,000 units a month, driving revenue growth over the medium term. Reliance on Chinese imports has also reduced over the past few fiscals, due to higher contribution from hard luggage segment (manufactured locally) and alternative sources developed domestically, partially mitigating any supply disruption risk. Contribution from hard luggage segment is expected to increase.

Apart from marquee brand Safari, the portfolio also includes other brands like Genius, Genie, Magnum, Activa, Orthofit, DBH, Egonauts and GScape. In terms of price hierarchy, Safari’s products fall at the bottom end of the pyramid, as they are more of a value for money (mass products) unlike VIP and Samsonite which have presence in economy and premium segments as well. Safari has consciously tried to increase its contribution from hard luggage over the last few years. There is a growing trend toward hard luggage.

Hard luggage has allowed changing the perception of luggage from utility to fashion in the minds of consumers. o Safari’s in-house manufacturing units are dedicated to only hard luggage. Currently this hard luggage plant is working at 60-65% capacity utilisation and should reach 90-100% capacity in 2- 3 months’ time. By the end of December, the company will double the capacity of this plant.

Safari has mass market positioning relative to VIP and Samsonite which operate across segments

Safari’s Hard Luggage Collection & Soft Luggage collection with exclusive variants

Safari’s new backpack collection is attractive

Backpacks collection for Safari has seen stark improvement with attractive SKUs and better designs. Trade margins range between 20-40%. Price of HL is slightly cheaper than SL of comparable size. SL had collection labels of 2020 and the stock appeared dated given ongoing supply chain issues from China. Shelf space for Safari has seen improvement in hypermarkets (equal presence of all 3 brands).

New Products

Entry in new product categories (ex- laptop bags, back packs etc). Expanding distribution channel from CSD to hyper market, MBO, EBO and Ecom. Setting up of offices in China, as Safari imports Soft Luggage from the dragon nation. Acquiring brands like Genius, Magnum, Egonauts, Gscape and Genie. Investing heavily in promotions.

The Company entered another product category with the launch of new luggage range under the Genie brand targeted at women consumers. Products designed specifically keeping the needs of women in mind, targets a large but unmet need within the luggage category. The Company has also started selling the Genie products through its brand website.

New product launched under the Brand name - Genie

Segment-wise Performance

The luggage category had a huge demand boost throughout the year apart from the first quarter. The trend of rising consumer preference for zippered hard luggage category continued as it is perceived to be more premium and durable. This trend was also accelerated by relatively higher availability and lower pricing for zippered hard luggage compared to soft luggage.

The Company continued to invest in zippered hard luggage by continuing to expand its range of polycarbonate zippered cases as well as launch of polypropylene zippered cases. Due to supply gaps from smaller unorganised players and a sharp uptick in marriages, the demand for the soft luggage was also robust and is expected to remain strong. While the backpack category declined during the year, the phased opening up of schools, colleges as well as office from fourth quarter is expected to drive a sharp bounce back in this segment.

Hard Luggage capacity expansion to boost growth & margin profile Safari has lined up an expansion plan of Rs500mn (~Rs225mn towards land & building and ~Rs275mn towards P&M) to expand HL capacity at Halol. To meet the rising demand for hard luggage, the Company is also setting up a new manufacturing plant through its wholly owned subsidiary in Halol, Gujarat for additional capacity for polypropylene zippered hard luggage.

Company is going through a capex expenditure of Rs 70 Crore which is funded by debt of Rs 30 Crore and remaining by internal accruals, capital structure is expected to be sustained with debt levels likely to remain moderate. The group is having a surplus cash funds with a cash balance of Rs 59.43 Crores as of March 31, 2022. The financial risk profile is expected to remain strong, backed by healthy accrual and moderate debt-funded capital expenditure (capex), over the medium term.

With a large-scale shift away from China sourcing to India and Bangladesh, the available production capacity for the industry continues to fall short compared to the market demand. The Company has been actively investing both in expanding owned production capacity for hard luggage, and in helping vendors expand their facilities for soft luggage and backpack production

Raw Material Volatility

The main raw materials like polypropylene and polycarbonate are mainly procured thereof from manufacturers/producers who are well reputed keeping in mind the need for quality and consistency. The upward movement in raw material and sourcing costs as well as adverse currency exchange rates have kept margins under pressure throughout the year. To manage this, apart from the shift in sourcing the company has taken multiple price increases in the latter half of the year and will continue to work towards further improving price realisation through product mix improvement.

According to the company, inflation was at its peak in Q3FY22 and Q4FY22. In the current quarter the company sees the raw material prices ease off- the commodities and components prices are softening. The ocean freight prices have also come down since July 2022. These all changes should reflect in their earnings from Q3FY23 onwards.

Margin Fluctuations

Gross profit increased 139.1% YoY to Rs1,126mn with a margin of 38.4% as compared to a margin of 39.2% in 1QFY22 and 38.7% in 4QFY22. Increasing share of own manufacturing (HL is produced in-house) in the portfolio is likely to act as a key margin lever and reduce reliance on China.

EBITDA increased 493.2% YoY to Rs. 417mn with a margin of 14.2% as benefits of operating leverage kicked in. PAT increased 985.1% YoY to Rs. 266mn with a margin of 9.1%.

Safari reported exceptional performance with 44% top-line growth over preCOVID base. Company reported revenue of around Rs 705 Crore in fiscal 2022. Growth rate is expected to sustain over the medium term especially in fiscal 2023 backed by enhanced capacity in the hard luggage segment, expansion plans in tier 2 and tier 3 cities pan India, wide range of products, and expected recovery in travel and tourism. Further there has been a sustained shift in consumer preference towards branded products.

Operating margin improved to 8% in fiscal 2022 (as against operating losses incurred during FY21). Operating margin is expected to improve further in fiscal 2023 as seen from the Q1 fiscal 2023. Improved capacity utilisation levels with improved volumes, expected price hikes, lower discounts offered and higher contribution from hard luggage and shift to larger contribution from polypropylene based products has contributed to improved operating margin.

The company is expecting good growth driven by a robust uptick in hard luggage as we continue to see the transformation from unorganized to organized segment, which given Safari's positioning is the biggest beneficiary. It is carrying on the momentum of an insignificant player in 2012 growing by leaps and bound over the years. With a focus now on in-house manufacturing and softening of RMAT prices (peak in Q4FY22).

Planning to move in-house for value addition

The Company recently commissioned its Polypropylene (PP) plant this new unit will also help the company to increase its sales of PP-based hard luggage. PP-based hard luggage is cost-effective compared to PC (Polycarbonate)-based hard luggage. Margins in PP hard luggage are highest followed by PC hard luggage followed by soft luggage. The company has incurred a total capex of Rs 500mn which could give them an additional revenue of close to ~Rs.4000mn at peak utilization.

Capacity expansion is expected to reduce reliance on outsourcing and boost margins as manufacturing profit will now accrue within the company in addition to trading profit. Further, PP based HL expansion will act as another margin lever as PP prices have been relatively stable unlike PC prices.

Safari Industries to be one of the biggest beneficiaries given its focused approach on the mass segment. Moreover, the company now focusing more on in-house manufacturing (new PP) which is margin accretive. Finally, the company is augmenting its distribution and entering new geographies which should help sustain growth. The Company continued to grow ahead of the market and the Company offers a competitive and innovative range, catering to consumer needs in all significant product categories.

With a strong focus on engaging younger consumers, the Company continued its efforts on building the Safari brand via strong advertising presence on digital platforms. To enhance its physical and mental brand availability, the Company added several retail stores in prestigious high footfall locations.

The Company also started a new International Business division focussed on export of luggage and backpacks. In the initial phase, the focus of this division will be to expand business in geographies with large Indian diaspora taking advantage of the latent equity of the 'Safari' brand in this segment.

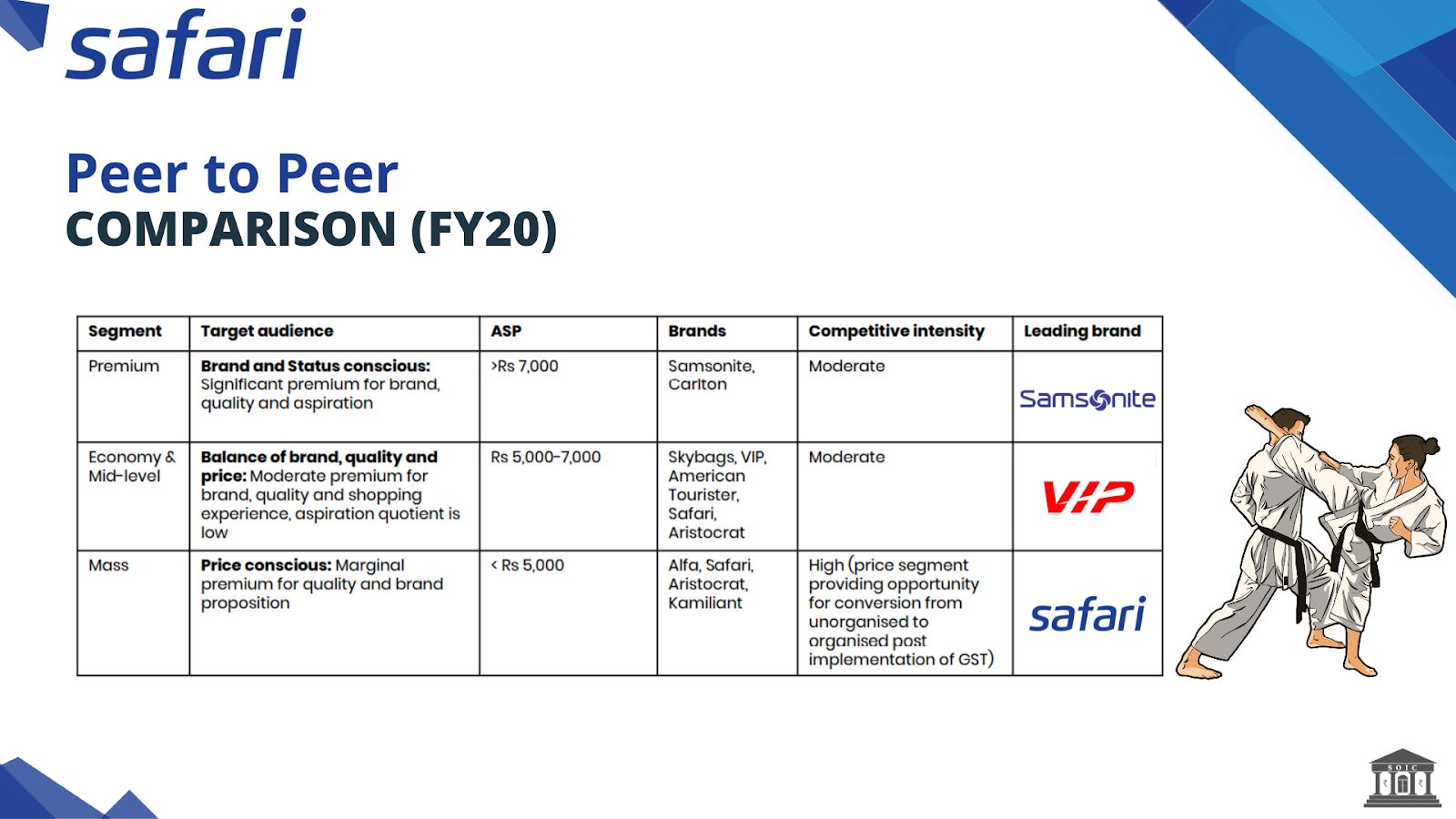

Peer to Peer Comparison (as of FY20)

Industry Updates

Safari management has indicated that demand for luggage continues to remain robust as the economy opens up. They foresee this to continue going forward, with the current demand conditions outweighing supplies. With the pandemic largely under control in the latter part of the year, the travel industry is seeing an unprecedented boom with consumers looking to get out of their houses after long period of lockdowns.

Marriage demand has also been strong led by the opening of the economy and easing of restrictions. For a large part of the year, the demand in the backpack segment remained muted due to limited opening of schools and offices, but there was a strong bounce back at the end of the year.

The E-commerce channel saw the strong demand throughout the year, as the pandemic has accelerated the jump in digital penetration as well as e-commerce adoption for higher ticket purchases. In Hyper channel, value retailers have shown strong growth, but the overall growth in the channel has been impacted due to poor participation in the market revival by one of the largest players in the sector.

The General Trade segment also saw a strong revival in demand with the pandemic leading to consumer preference for walking into high-street stores rather than the enclosed environment of Malls and due to the market vacuum created by store closures of a large Hyper market player. The demand in the Canteen Stores Department segment was stable during the second half of the year.

The overall long-term outlook for the sector remains very robust with a travel coming back in a big way, opening of schools and offices, and marriage demand seeing a strong upswing. Other structural factors driving industry growth continue to be in place such as accelerated shift in consumer preference away from unorganised labels to brands, increase in ownership of multiple bags and shortening replacement cycles.

Key Beneficiary of GST Led Demand Transition

Safari is one of the top 3 luggage brands and occupies a leadership position in the oligopolistic Indian luggage market. VIP and Samsonite are the other major players in the domestic market which largely cater to the mid-level and premium markets. Safari's product offerings are largely confined to the mass category since SAFARI is largely perceived as a "value for money" brand. Over the years, the company has successfully established itself as one of the leading brands in the mass/economy segment.

Moreover, implementation of GST reduced the price gap between products of organised/branded and unorganised/non branded players. The market share of unorganised players is on a decline as organised players continue to gain market share post GST implementation era. This transition is happening at an accelerated pace in the mass/entry segment since the price gap between the mass product of an organised player and premium product of unorganised has been reduced to - 15-20% only as per industry sources. This has largely benefitted Safari’s since it caters to the mass/economy segment which is further visible in the company's growth rate vis-à-vis competition.

Key risk

· Exposure to volatility in raw material prices and forex rates

· Subdued revenue growth and operating margins sustained below 7%, constrains overall business risk profile

· Working capital-intensive operations

· Stretch in working capital cycle or large debt funded capex/acquisition weakens the financial risk profile

Hope we were able to add value and you liked the analyses. Looking forward to your feedback and questions in the comment section below.

Disclosure: Nothing on this website should be construed as investment advice. Please consult your financial advisor. We are not SEBI registered Analysts/Advisors. We are not accountable for any loss or gains that might occur to you from this or any analysis on the website. The author and SOIC do not hold the stocks in their portfolio at the date this post was published.