SOIC ANNUAL LETTER 2022

“No man ever steps in the same river twice, for it’s not the same river and he’s not the same man.”- Heraclitus

Wishing you and your family a happy new year! :) This is our first ever annual letter (hopefully the first of many). I will be listing out some of my key learning’s from the journey in the last 5 years of investing and the last 15 months of starting SOIC. When I look back at it, I am immensely grateful to you and proud of the team of what we are building. I often wondered why no one was covering businesses bottoms up in the Indian markets. Many talk about Warren Buffett or Charlie Munger, but very few practice what they’ve actually done. That is to sit on their ass and read one business after the other. There is this story about Charlie Munger of how he read The Barron’s for 50 years in a row and he found one idea through which he made $80 million and in turn which he gave it to Li Lu who turned it into more than $500 million. I am not saying that you have to wait for that long, the key takeaway at least for me is to inculcate the habit of reading at least 1 business a day. All gyaan in the world about behavioural finance is good, but it won’t help you much in your journey if you do not inculcate this habit in your routine.

Let’s deep dive into some of the key learning’s from the past and what you take away from them. :) I will also briefly throw light upon some of the opportunities we see in the future:

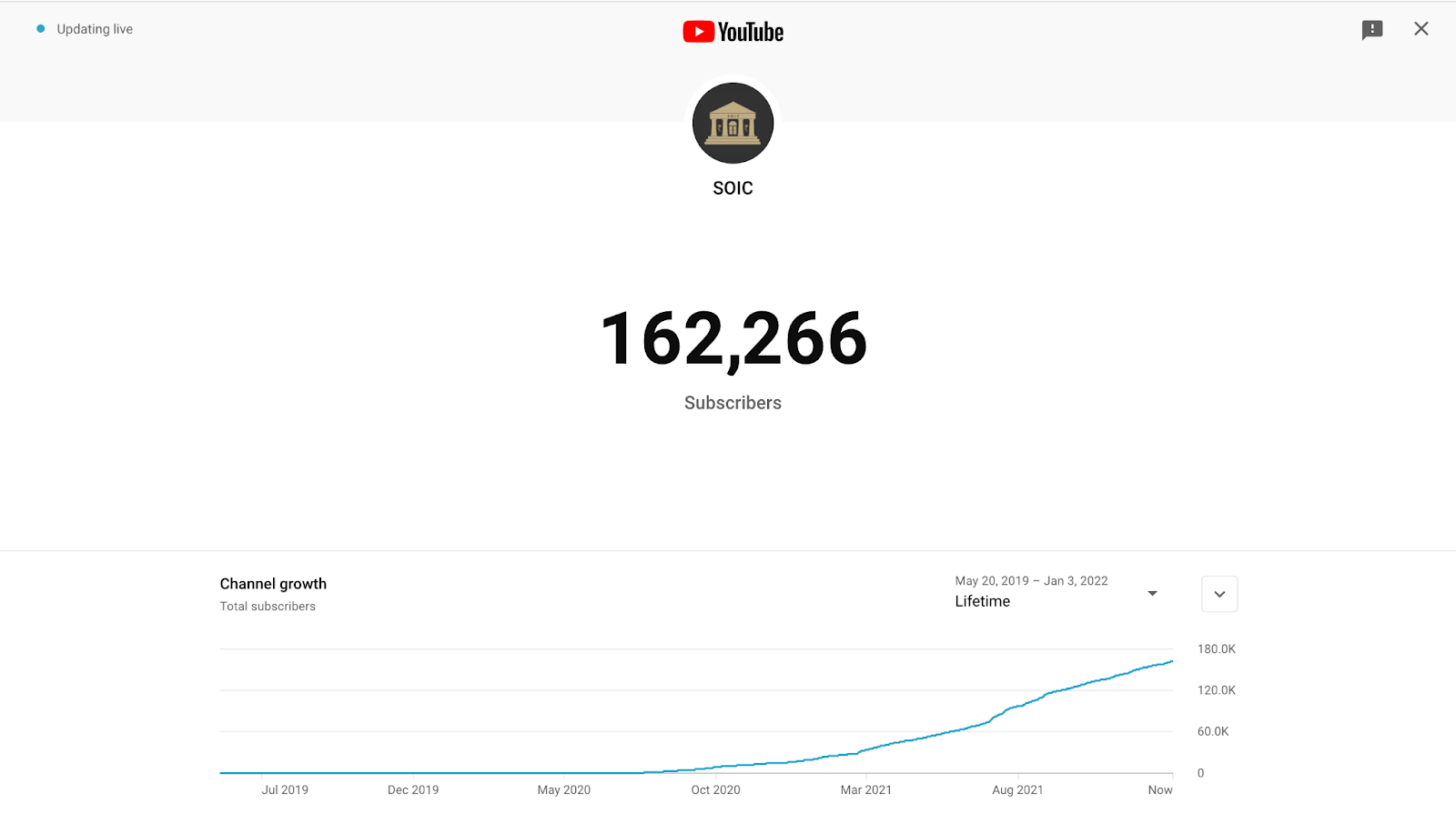

Compounding is a force to reckon with. The sooner people identify this, the better it is for them. Let me give you a brief example of how this played out right in front of me. When we started our YouTube channel, barely 100 people wanted to watch our content. Truth to be told, I had nothing better to do as there was also a deeper reason behind starting the channel. Since childhood, I have always admired teachers. Some of the teachers who’ve taught me, I really admired the depth of their knowledge and ability to explain complex concepts in a simplified manner. This is what we wanted to replicate, and apply it to the field of investing. I have looked at the CFA books, met a few CFAs, investment advisors and fund managers. Barring a few, everyone is only after one thing i.e. to complicate investing. What use does a Capital Asset Pricing model have for a retail investor trying to achieve financial freedom? What is the point of studying quant if you want to analyse businesses at the end of the day? In simple words, the truth is that complexity and authority bias sells. The wide gap that we personally thought was quite evident, is that no one wants to make retail smart. Who even teaches business analysis? With this simple idea to simplify how to analyse a business we started SOIC. Just a reminder, all degrees or charters are only meant to do what at the end in investing?Simple answer is to analyse businesses. We skipped to the good part. The initial 3 months of our journey were really difficult, but we remained focused on putting out quality content and to teach the key concepts. Slowly, the viewership started increasing and this was aided by a few white swan events. As some of our videos were liked and shared by wonderful Twitter handles such as Sajal sir (unseen value, forever grateful 🙏). Bit by bit the viewership and the subscriber count started rising. Fast forward to 108 videos and consistent posting on every Sunday, this is how the subscriber base on YouTube looks like:

Key takeaway is to genuinely believe in the power of compounding.If one concept that you can take away and apply it widely across the world are the two C’s. Consistency and Compounding. Before I leave you with this learning, please also read what Nitin Kamath, the founder of Zerodha has to say about the user growth at zerodha:

“It took us six years to get the first 100,000 customers and nine months for the next 100,000. It took us eight years to reach 1 million customers and only 1.5 years for the next 1 million. It took us almost ten years to get to 2 million customers, which was around the time COVID hit, and then we added our next ~6 million customers in just 18 months. Just for added context, we added 400,000 customers in October 2021, while it took us seven years to add our first 400,000. So yes, the last 18 months have been spectacular, not just for us, but broking businesses around the world.”

2) Know the game that you are playing: to quote Prabhakar Kudva from his blog, “the best of the investors know the game they are playing in their bones.” This also reminds me of a very famous saying, if you don’t know who you are then stock market is really expensive place to find that out. We have to realise that everyone is playing a different game before we listen to them. A retail investor who invests from a 2-3 year horizon will have a different mindset vs the investor who invests for 5-10 years. One important lesson here is not to judge investors on the basis of their time horizon. It’s fashionable to call yourself long term buy & hold. In truth, very few businesses are actually long term buy and holds. For us, at least the holding decision is dependent on whether the management executes or whether the long tailwinds are intact or not. Before you judge anyone, let me give you an example of an investor who bought and sold over 400 stocks in a span of 10 years.

Guess who the investor is? If you guessed Warren Buffett from the 1950s till he stopped managing his fund then you’re right. The point is to accept that in different phases of our financial life we might choose to invest differently. For a youngster investing might mean something else vs someone who has already achieved financial freedom. This is the beauty of the game, there are multiple truths. No one truth is right when viewed from a single perspective. Those who know their game, end up doing well in the long run in face of the noise.

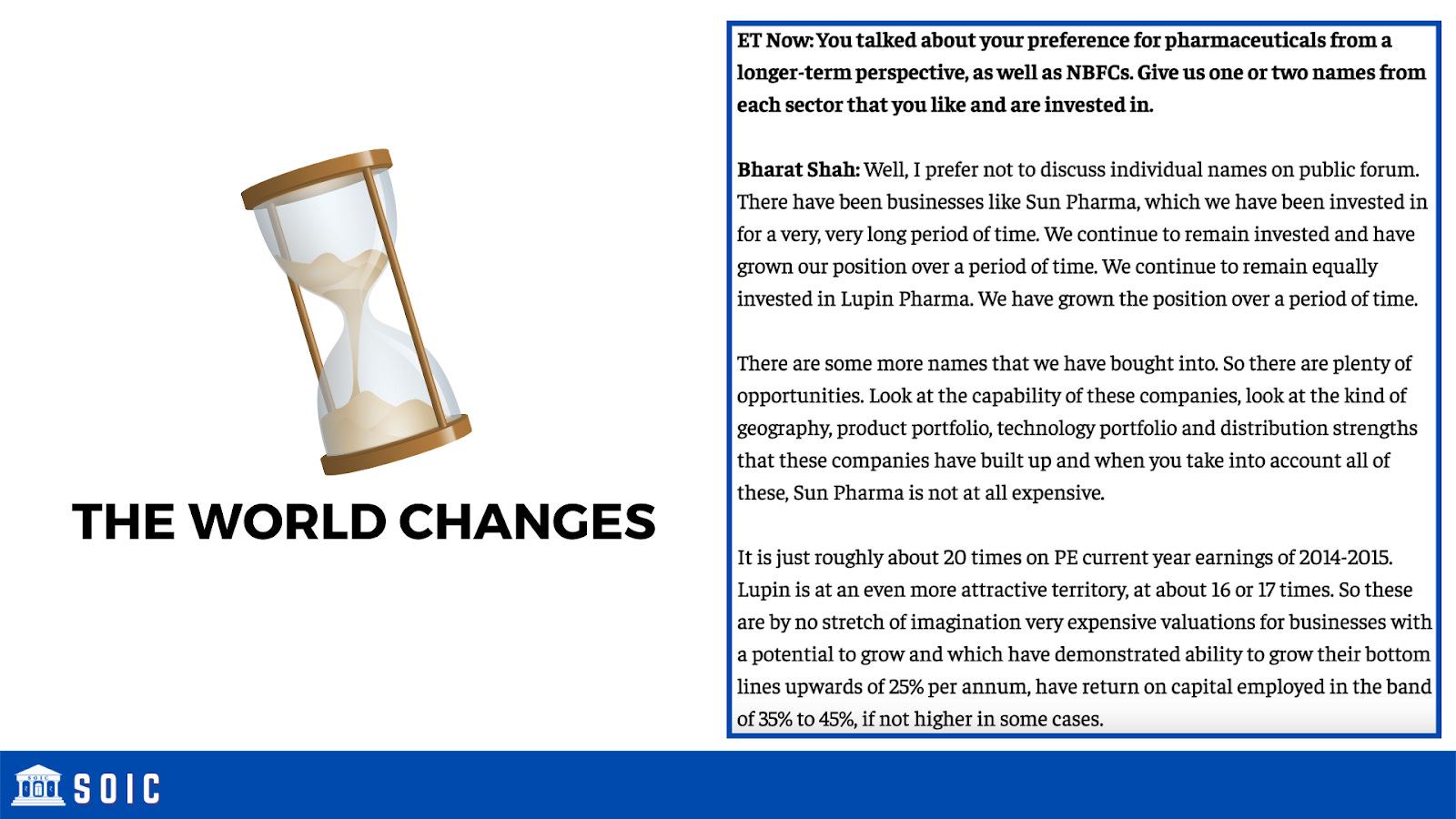

3) The world changes, it pays to be humble. One thing that is true across all investing time frames is that the world changes. No point in being arrogant in this game or thinking that you know enough. Just ask investors in 2015 whether they remember the rising chemical sector or not? Or ask the investors in 2014, did they see large generic Indian Pharma companies facing pricing erosion due to distributor consolidation in the USA? One of the investors I like a lot was invested in large generic pharmaceutical companies back then:

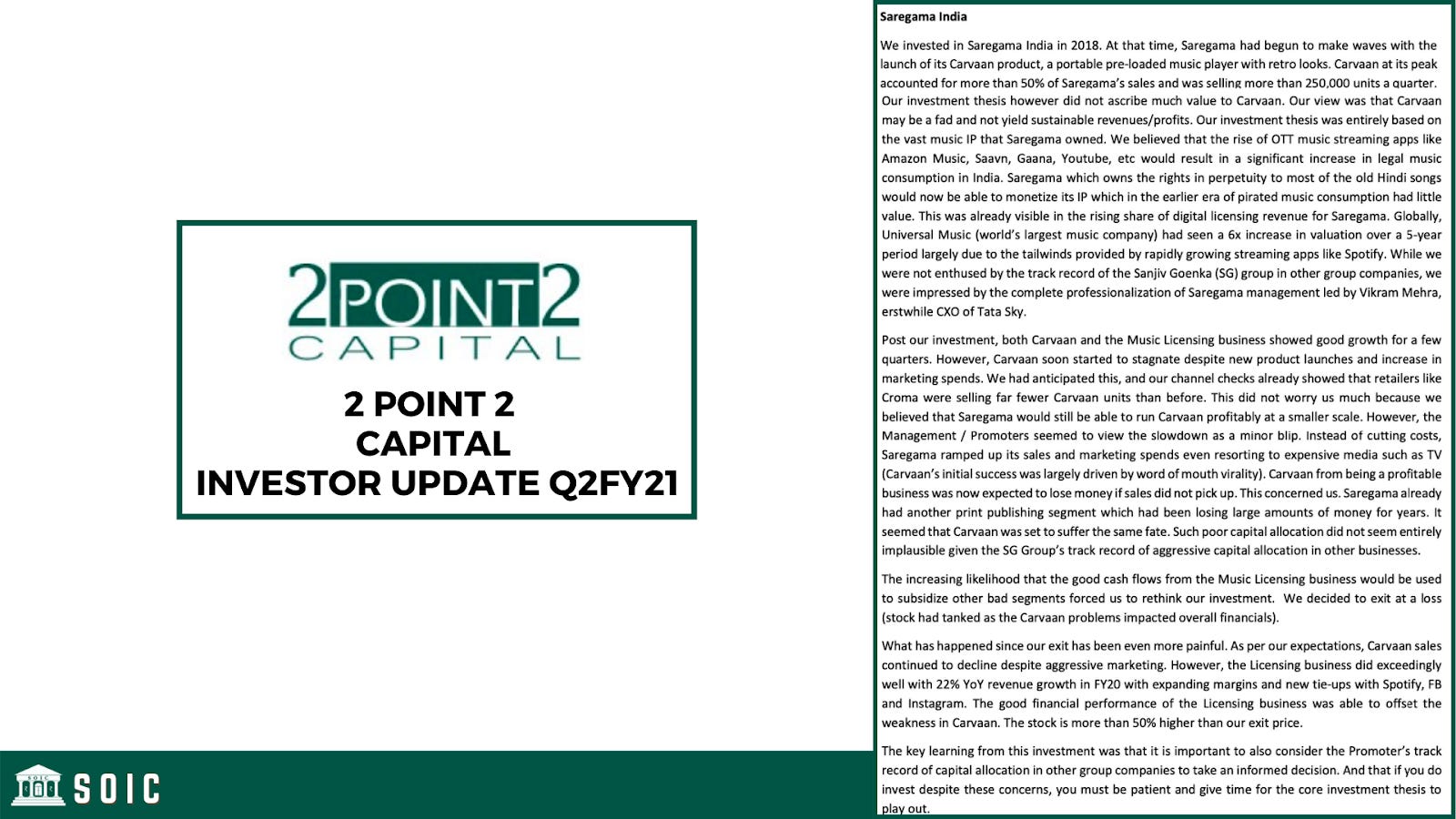

On a personal level, this realisation dawned on me with a few recent examples. I first read about Saregama way back in 2018-2019. Back then it was experimenting with the Caravan product and had a small music licensing business which most investors rarely bothered to ask about in the concall. I read vaguely about the business back then. However, what really piqued my interest was a newsletter by Mr. Amit Mantri when he pointed out his mistake of selling out Saregama and it has been up 50% from his selling point. This is where I would like you to stop and think about the difference between the price and Valuation of a stock. This letter which was published on 20th October 2020, was the point that reignited my interest in the business. After going through the con calls and witnessing that they announced 200 crores of incremental capital allocation in the highly profitable music licensing business, I changed my mind. Started buying aggressively in Jan. Another reason to change my mind was that a friend of mine kept asking me to look at this. I’m deeply grateful to him that he did so. Otherwise, I would have missed investing in a sector that wasn’t even known just 18 months ago. This was my highlight of the year, as my largest position became a 5 bagger and I kept averaging up till I was comfortable with the allocation and valuation of the business.

Another example of how the world changes. I always thought that hospitals are a gruesome business, till I came across a few hospitals which are actually doing 32% ROCE. I do believe this is another sector where the place is misunderstood by many investors and pms managers alike. This is what ends up creating opportunities for variant perception.

The key learning is to remember that it pays to be humble and to have an open mind. Wealth creating stocks can be found even in high PE companies that are set to grow exponentially. Forget these stupid labels of being a deep value investor or a growth investor. All intelligent investing actually in reality is value investing. (Trading is different)

4) What really matters

Four levers that matter the most when it comes to investing:

The first lever that matters the most is earnings growth. How rapidly the business can grow its earnings. Some tell tale signs to look for earnings growth are:

High capacity expansion plans, aggressive headcount addition when it comes to IT businesses (think Coforge or LTI), confirmed order books (think PI Industries), efforts to reduce costs, fast growing industries (think end user capex like in EKC’s case or HLE Glasscoat)and changing patterns of distribution (think Saregama or Goldiam International).

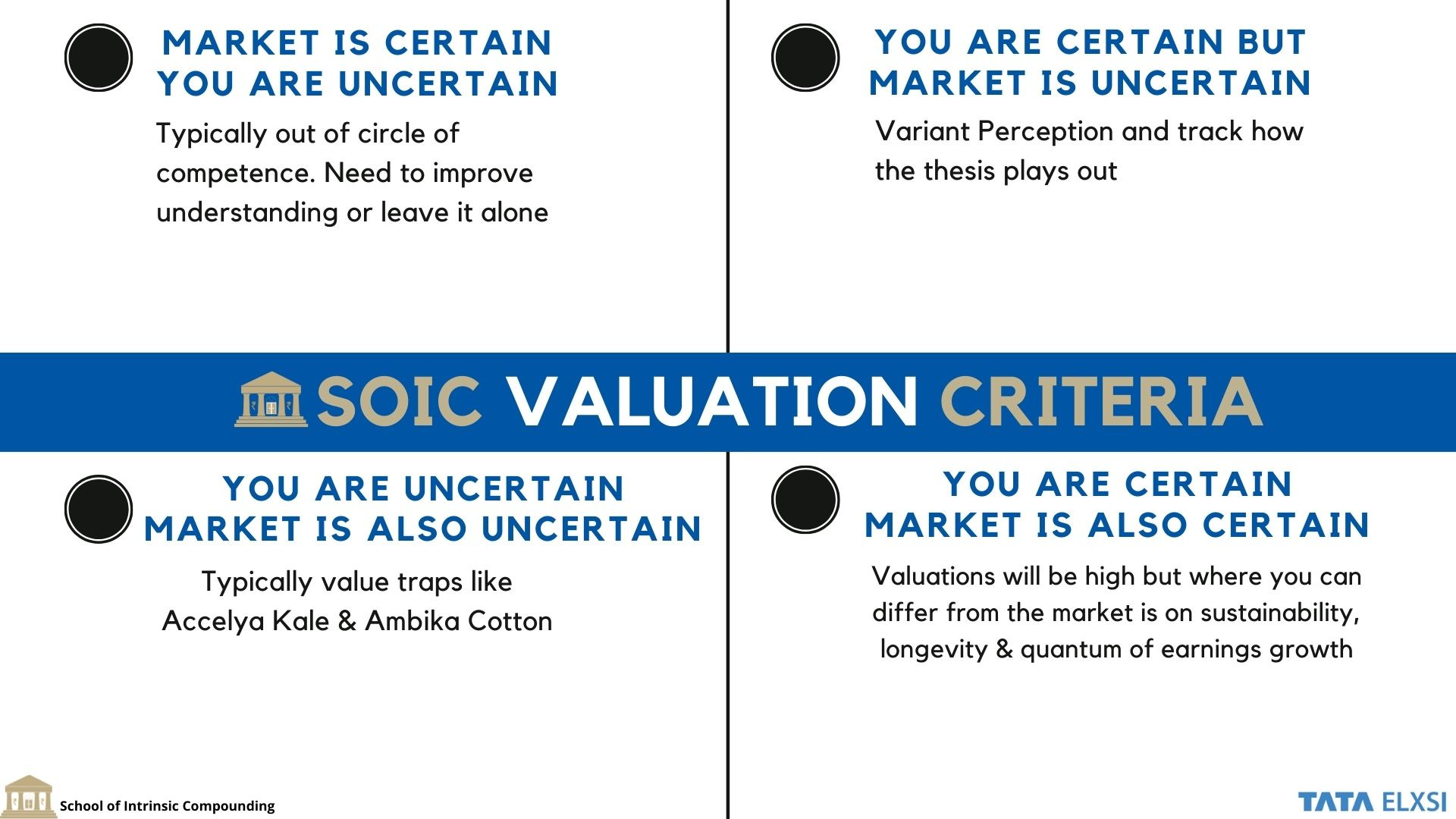

The second lever that matters the most are the starting valuations or at least the way you understand valuations. Here is how we perceive valuations:

We typically play in the second and the fourth bucket of valuations. We do not understand paying up for 10-12% growers. Much more comfortable in paying up for 30-35%+ growers. In the second quadrant, I look for out of favour sectors or companies where starting valuations are dirt cheap (e.g. HCG, Pix or Equitas types).

Third lever that matters the most is whether the ROCE is on an improving trajectory or at least it remains stable. I typically like companies that are doing brownfield capex or debottlenecking vs greenfield. At lesser capital spent I can chug out more returns on capital employed, this is what it effectively means. Do study Fairchem, Alkyl in 2019,EKCs upcoming debottlenecking or Pix’s brownfield. Watch our Variant perception video to understand more. :)

Fourth and the final lever is what the investor does with his buying, holding and selling decisions. Your understanding of the business and risk & reward are the bridges that stand between you and your eventual outcome (excluding luck for a while). I have leveraged anchor bias and use 4-6-8-12% rules for my PF allocation. 12% ideas are only two in the current portfolio and remaining are between 4-8%. At no time the personal portfolio ever crosses 15-20 stocks. This is it for my argument between concentration vs diversification. Not too concentrated to die and neither too diversified to suffer from mediocre returns or sleepless nights of tracking too many businesses.

5) Finally let’s put it together with the process with case studies

Let’s look at the process and outcome or the eventual outcome in some of the case studies:

Alkyl Amines (2019)

Process: good management, solid industry structure, duopoly, indirect proxy for the pharmaceutical industry, good margins, upcoming huge capex of methyl amines and consistent dividend payouts and finally earnings triggers were there. Got in at a PE of 13 times.

Outcome: stock was rapidly rerated as we got lucky due to acetonitrile realisations spiking. Margins went beyond our wildest expectations. Unfortunately, I ended up selling it when it was a 4 bagger. Never imagined the narrative that will get attached to the business. One of the key learning’s has been that the narrative for businesses also evolves with the changing valuations and as more and more people discover the story. This is something that I am still learning, to view a stock differently with the quality of investors that come in at different stages of its journey.

Healthcare Global:

Process: fastest growing therapy, Capex coming to a full stop, free cash flow generation, with 12-15% top line growth, new centres have just broken even and are already doing 22%+ EBITDA margins in existing centres, EBITDA will grow much faster and the company is deleveraging with the PE fund coming in.

Outcome: time will tell, initial signs are encouraging.

IIFL Finance: incremental ROE is already above 20%, housing finance AUM touching 20,000 crores, wholesale book has been sold, deep undervaluation.

Suven Pharmaceuticals: bought post demerger, best margins in the pharma space, capex completing, was available at 14 times PE for a business with 35% ROCE.

Outcome: made a 2.5 bagger and sold the stock after they announced a huge maintenance capex which I am not competent enough to understand.

Others: Saregama, Navin, Equitas Hold co, Deepak Nitrite, Neogen,EKC,Hikal, Lauras, Pix Transmission, Arman Finance, Pi industries, Pix transmission,IEX (sold) etc. I run my own family portfolio too, that is a bit more diversified to 20-22 stocks.

Some bad outcomes and bad processes.

Sequent:

Process: Epic API Business, segmental analysis tells me formulation business is sitting on massive operating leverage (will be doing 5-6% EBITDA margin here vs potential of 20% at least ), only approved API Plant for the regulated markets, secular growth industry and one of a kind player.

Outcome: sold when it came back to the buying price. The primary mistake was the inability to factor in the cost that the PE Fund has upfronted via the P&L hiring consultants and what not. Will I keep tracking this? The answer is absolutely! Unlike many human endeavours, the same company can offer you a second chance when the real butterfly emerges. That is margins in Sequent’s case.

DCB Bank: mere ROE aayege story just like what investors think of IDFC First Bank. Best thing to do in financials is to let the double digit ROE Emerge before taking a plunge in turnarounds. As these types of businesses have a very long runway for growth in my view.

I close the year with a 68% gain as of date vs 59% for nifty small cap 100. Last key learning has been over the years, is that this is a probabilistic game that we are playing. Do not get attached to nutty formulas like I will buy below PE ratio of 10 or some other formula. If the business changes, all these formulas will go to the dustbin.

Always remember: sizing hai khaas Baki sab ________?

Let me know what you think?

I promise to write more this year, because writing ultimately ends up helping me clarify my own thoughts. Waiting to read your comments below.

Have a great year ahead everyone! :)

Excellent read

Loved it, thank you man. Looking forward to more of these.