Tariff or No Tariff ? 🤺

Market Breadth

The week started off with a big fall led by all the tariff tensions and anxiety amongst the street but as Trump announced a 90 day pause on the reciprocal tariffs and getting into the proper tariff war with China. Both nations do not seem to back off on the tariff war situations. The US has imposed a 145% tariff on Chinese imports while China has imposed 125% on US imports. Also China has restricted a few rare earth mineral exports from China.

In contrast, sectoral indices reveal pockets of relative strength—particularly in Financial Services, Banking, and, to some extent, FMCG—where 1M or even 3M returns are more resilient. Meanwhile, other sectors (like Metals, IT, and Pharma) have faced more persistent pressure.

Relative Performance

Here are the Top 10 themes that are showing better relative performance vs the Nifty 500. Small Finance banks are showing strength led by the improved collection efficiencies in the microfinance segment. Also FMCG names are doing relatively well because of the interest shift towards the defensive.

Stay on top of markets: StockScans.in delivers powerful, real-time screeners tailored for the Indian market.

{We recently conducted an interesting webinar on Aroma Chemicals & Their Hidden Potential (included in our SOIC Membership).

Join our SOIC Membership now with the exclusive New Financial Year offer

Coupon Code: SOICFY2026 (valid for 48 hours)

Enrol for 1 year or 3 years: https://learn.soic.in/learn/fast-checkout/97666?priceId=36137 } }

The Tariff Situation and Implications for multiple sectors

The report emphasises that the current tariff environment is not just a short‐term trade policy adjustment—it is a strategic manoeuvre with deep geopolitical and macroeconomic implications. The U.S. has recently shifted its trade stance by imposing a broad reciprocal tariff regime on about 95% of its imported goods from 180 trading partners.

For example, while tariffs on countries such as India and Vietnam have been raised to 26% and 46% respectively, China faces a peak rate as high as 54%. This sweeping increase is designed to force a rebalancing of trade flows and encourage the revival of domestic manufacturing. However, it also exposes vulnerabilities: the U.S. trade deficit has doubled since 2019, and its debt levels have skyrocketed—from 10.2 trillion USD in the aftermath of the 2008 crisis to a staggering 35 trillion USD, equating to roughly 124% of its GDP.

In the backdrop of these changes, China’s rise is particularly noteworthy. China has not only managed to record large trade surpluses (with a surplus of around USD992bn in 2024) but also increased its strategic financial clout by owning significant stakes in U.S. treasury bonds and leveraging initiatives like the Belt and Road Initiative (BRI). Moreover, recent advances in key technology areas—such as open-source AI developments exemplified by Deepseek AI—and moves toward digital trade frameworks (e.g. Digital RMB) signal that China is rapidly reducing the long-held U.S. advantage in high technology, further complicating the global economic order.

The increase in tariffs is ranging from 18% for the EU to 49% in Cambodia. China will have more than 111% increase post recent announcement.

The US has a significant trade deficit with its top partners with a deficit of USD bn of 295, 172,85,68,66 and 64bn with China, Mexico, Germany, Canada, Japan and Korea. The deficit with India stands at USD45.6bn.

US exports include oils and technology intensive products in nuclear reactors, Machinery, Electronic equipment, vehicles, aircraft, space, opto equipment, medical equipment and high-end lifesaving medicines.

US imports are common usage products like computers, mobiles, gems and stones, crude oil, automobile, plastics, pharma, furniture etc. this shows the impact of US strategy to focus on higher value-added technology items and leave others for manufacturing in low labour cost destinations.

*Fun Fact - The pursuit of global economic and political dominance and hegemony fuelled the First and Second World Wars between Germany, Italy, and the US and its allies. This era of conflict was followed by the Cold War between the USA and USSR, culminating in the dissolution of the USSR. Notably, all these conflicts were driven and dominated by countries with robust industrial foundations.

What are the plausible impact on the global business environment -

Global supply chain yet again going for a toss

Global GDP growth rates to moderate and inflation rates to rise especially in US

Increased volatility in commodity prices like gold, silver, crude etc.

Gold can remain firm as a haven in the uncertain times

What is in India from all these situations?

The India-US relationship has grown significantly, with India now a key strategic ally. Despite this, trade tensions persist, with President Trump labelling India a major abuser of trade barriers. India's primary exports to the US include gems, jewellery, electronics, and textiles, while it imports mineral fuel, aircraft, and machinery. India maintains a trade surplus with the US, driven by a substantial service export sector.

The share of exports to GDP is around 22%, which is in line with or lower than most competing Asian countries like Vietnam, Japan, Korea, Thailand, and Malaysia. This is because India's economy is focused on domestic consumption due to its large population.

Impact on multiple sectors from the current situation:

Domestic Manufacturing & Capital Goods:

Although the U.S. government’s tariff strategy is meant to spur domestic manufacturing, the reality is more nuanced. Many large industrial players, particularly in capital goods, are already hitting cyclical peaks in profitability. A slowdown in global trade and disruptions in supply chains due to heightened tariffs may further compress earnings. Companies involved in defence and core engineering sectors, however, may experience resilience, especially if they benefit from policies boosting government capex.

Consumer and Retail Sectors:

Tariff hikes are expected to ripple through consumer prices. The increased cost of imported common-use products such as electronics, vehicles, and even everyday items like furniture could dampen consumer sentiment. Even though domestic sectors like retail are positioned as defensive plays in the current environment, the lingering uncertainty could still put pressure on spending and ultimately on short-term earnings.

Healthcare and Pharmaceuticals:

This segment appears relatively insulated from the direct adverse effects of tariff escalations. Domestic healthcare providers and pharmaceutical companies—especially those with a focus on essential services—are expected to outperform. Healthcare, particularly hospitals and domestic pharma, stands out as a brighter spot, thanks to structural demand and less vulnerability to global trade disruptions. But US export based pharmaceuticals companies still face the risk of tariffs as multiple times trump has indicated for tariffs on pharma imports

Information Technology:

The IT services sector, heavily reliant on global outsourcing, is likely to face a slowdown due to reduced ordering by clients amid global uncertainty. With the slowing environment the discretionary spending might go for a toss by the business on IT services which might lead to still a slower growth environment for the companies

Electronics:

Electronics was India’s top export to the U.S. in FY24 ($11.1B), driven largely by Apple iPhones assembled in India (50% of exports). India’s cost advantage remains intact as competitors like China (>100% tariff) and Vietnam (46%) have higher tariffs as of now. Also Smartphones, Tablets and laptops imports are exempted from the tariffsTextiles & Apparel:

The textile sector remains a key export sector for India, with shipments to the U.S. reaching $2.8 billion in FY24, which is approximately 28% of India’s total textile exports. However, India's share of the U.S. apparel import market remains at approximately 6%, which is notably lower than China's 21%, Vietnam's 19%, and Bangladesh's 9%. India's reciprocal tariff is lower than Bangladesh's 37%, Vietnam's 46%, Cambodia's 49%, and Thailand's 36%. Due to an abundant supply of local raw materials, India can capitalize on this advantage over the long term by increasing capacity and realigning its supply chain. The home textiles sector appears to be in a more advantageous position due to existing capacity and an established supply chain that can meet U.S. demand.

TCS Q4 Result review - Slow Slow Slow

TCS reported a muted quarter, with weak headline numbers and a margin down fall. Q4 revenues grew by 2.5% on a CC basis marking it to be one of the slowest quarters in the past 4 years. The full year growth was 4.2% on CC basis. Also the operating margins had a 30bps decline and no positive notes by the management that the margins or the revenue growth might pick up in the near term.

Also TCS only added 625 employees in the current quarter compared to the previous quarter and on top of it the company has delayed its salary hikes on the basis of a slower demand environment.

What this shows is that the largest IT service provider in the country is slowing down led by the slowing down of decision making by the customers which again shows that the discretionary spending by the business in the major geographies are slowing down.

The imposition of tariffs by the Trump administration, followed by a partial pause for countries other than China and an escalation of tariffs against China, among other measures, has led to heightened macro uncertainty and geopolitical tensions and risks slowing down global economic growth. We believe that a combination of higher uncertainty and growth slowdown is not a favorable environment for IT services demand

Higher spending on hardware and AI infrastructure layers to enable generative AI development and adoption and the possibility of using generative AI to generate significant productivity in IT services.

It seems the company was in the downfall phase and the “fundamental breakout” is nowhere to be near for the company seeing over the overall scenario.

To understand more about the slowdown in the IT sector in the country do watch the IT sector analysis video

Management meet corner - SOIC Research

Windlas Biotech Management Meet

Overall Business Strategy and Vision:

Windlas Biotech's core strength lies in manufacturing, positioning itself as a reliable and quality-focused partner for various players in the pharmaceutical market.

The company aims to cater to every kind of player that emerges in the market, acting as a channel for them, regardless of whether they focus on branded or generic products.

The focus is on volume growth, and the company believes the market volume growth is currently underreported, particularly in the trade generic segment.

Windlas Biotech aims for consistent parallel growth by adding geographies and products.

The company is not planning to enter the US market in the foreseeable future (at least 10 years), citing a different business model requirement that doesn't suit their current approach. Their primary focus remains India and the rest of the world (excluding the US).

Domestic Market (Trade Generics and Branded):

There is a significant unmet need in reaching rural populations (e.g., 2000 villages in a UP district), suggesting a different model is required compared to branded approaches focused on urban centres.

The growth of companies targeting the trade generic segment depends on a healthy balance between growth and receivables recovery. Windlas Biotech has implemented systems to manage this, such as stopping billing if the first payment isn't received after a certain amount.

Branded companies are increasingly looking at the Over-The-Counter (OTC) market to build brands, as the trade generic space poses a different set of challenges.

Windlas Biotech sees a natural advantage for manufacturers (not just brand owners) in the current market due to their quality systems and understanding, especially as branded products in the trade generic segment can face channel conflicts in metro cities.

The company has a customer base for both branded and trade generic products.

Trade generics and the institutional business have both shown phenomenal growth in recent years for Windlas Biotech.

The company offers full flexibility to its teams to survey the market and decide on suitable products for the trade generic segment, but branded products are generally more successful in metros.

Windlas Biotech ensures the quality of its trade generics with a QR code on every pack, allowing customers to access the Certificate of Analysis (COA).

Distribution and Stockists:

Windlas Biotech works with stockists, sharing margins with them and often offering them exclusivity for a particular area, allowing them to potentially earn more than with single-product-focused branded players.

The company continuously adds and removes stockists, focusing on active stockists who generate business and adhere to payment terms. A trial period exists to assess a stockist's reliability.

The company believes in a direct stock model to better understand the market, track sales, and manage payments, avoiding the dilution of margins and lack of visibility associated with distributors.

Selling styles and skills required for trade generics differ from those for branded products, with trade generic distributors often being more proactive in building revenue.

Contract Manufacturing Organisation (CMO):

The growth in trade generics and institutional business directly contributes to Windlas Biotech's CMO segment.

The company consistently works on adding new customers and expanding the product portfolio within the CMO segment.

Windlas Biotech has been successful in reducing customer concentration among its top clients, indicating a broadening customer base.

The business development teams have specific targets for acquiring new CMO customers, separate from growing business with existing ones.

The company focuses on understanding the customer's needs, their growth areas, and if Windlas Biotech has any unique offerings in those therapies when acquiring new CMO clients.

Exports:

Windlas Biotech is actively exploring export opportunities, particularly in Europe.

They have obtained approvals from South American authorities and have made acquisitions (MA) in Europe. One MA is in Germany.

The European regulatory approval process is slow.

Germany's market is largely tender-based, which has influenced Windlas Biotech's acquisition strategy there.

Product liability is a key consideration in the European market.

The company is taking a step-by-step approach to exports, focusing on learning and building a sustainable business.

Windlas Biotech is open to further MA in both domestic and export markets, particularly for dosage forms that can accelerate their export growth by providing a front-end presence or existing MA. They are looking for good assets where 1+1 can equal 11.

While not providing specific timelines, the management sees significant potential in the export business.

Injectables:

Windlas Biotech has invested in and upgraded its facilities, including for injectables (Plant 5).

Injectables will serve all three verticals (CMO, trade generics, and exports).

Achieving decent capacity utilisation in the injectables segment and seeing its financial impact will take time.

The company has stabilised around 10 products on the injectables side.

Export of injectables is expected to take time, with plant and product approvals needed, potentially extending into FY29.

Financial Performance and Margins:

Asset turnover is expected to improve due to the capital expenditure made.

The company has a long-term perspective on growth and profitability, advising against looking at vertical-wise growth on a quarterly basis.

Trade generic margins are 3-4% higher than regular CMO margins, while export margins are 3-4% higher than Trade Generics.

The company expects margins to improve due to operational efficiencies and increased revenue from higher-margin businesses like institutions and, eventually, injectables.

The target is to reach a 14-15% EBITDA margin, though the timeline depends on various factors.

Employee costs have increased due to minimum wage increases, injectables hiring, and business development team expansion. This increase is not expected to be at the same rate next year as hiring has largely been factored into the current financials.

Operational Aspects (Manufacturing & Quality):

Windlas Biotech undergoes frequent audits (70-80 times a year) by different customers, contributing to their learning and quality improvements.

The company is strongly prepared for Schedule M compliance, having proactively addressed requirements through infrastructure upgrades, expertise development, and software implementation to reduce manual processes and improve quality systems.

Supply chain efficiencies are a continuous focus area.

The company has a three-year roadmap for continuous improvement in its systems and processes.

Future Outlook and Growth Drivers:

The management is very positive about the future and expects continued growth across all segments.

Key growth drivers include expanding geographies, adding products, and increasing the number of active stockists.

The company believes the domestic market offers significant opportunities, especially in reaching underserved populations with trade generics.

Successful penetration of the export market and achieving higher capacity utilisation in injectables are crucial for future growth and improved profitability.

Acquisitions (MA):

Windlas Biotech is open to MA opportunities in both domestic and export markets.

The primary focus for MA is to acquire dosage forms that can accelerate export growth, provide a front-end, or possess existing marketing authorisations.

They are looking for businesses with good assets where synergy can be achieved.

Shareholder Returns (Dividends, Buybacks):

Windlas Biotech has a dividend policy and intends to continue distributing dividends.

The company has also undertaken a share buyback in the past and remains open to future buybacks, but the decision will be made based on future circumstances.

Schedule M:

Upcoming implementation of Schedule M positively. They believe that serious players with strong quality systems will tend to benefit from it.

The company has been proactively preparing for Schedule M compliance. They had already invested in and upgraded their older facilities.

They undergo frequent audits, around 70-80 times a year, by different customers. This continuous auditing process has helped them learn and stay aware of the requirements that were eventually outlined in Schedule M.

The preparations for Schedule M involved several aspects:

Infrastructure upgrades: Some changes required modifications to the physical facilities.

People expertise: Developing the necessary skills and knowledge within their teams was crucial.

Software implementation: They focused on moving away from manual processes by implementing software to improve quality systems and reduce errors. This also helps in trend analysis to identify areas for improvement and implement interventions, creating a live reading system.

Windlas Biotech states they have been successful in moving towards these requirements across infrastructure, people's expertise, and software.

The management considers quality a continuous and never-ending process. They have a three-year roadmap for continuous improvement in their systems and processes, even beyond Schedule M compliance. This roadmap involves progressively pushing for more system and software integration to reduce variability in reporting and enhance trend analysis.

It is leading to a consolidation of suppliers. Customers are showing dissatisfaction with their current suppliers, possibly triggered by non-compliance or quality issues, and are looking for better alternatives.

When a batch of a customer's product is found to be Not Standard (NS) and is listed on a regulatory website, the customer's management becomes very involved. They start scrutinising their entire supply chain, including where their other products are manufactured, audit history, and the supplier's track record. This indicates that Schedule M and increased regulatory scrutiny are making branded companies more cautious about their outsourcing partners.

Regarding small and medium-sized manufacturers, the implementation of Schedule M might lead to some shutdowns. While the total number of companies shutting down might not be drastically high compared to the overall number of manufacturers (around 12,000-13,000), there is definitely some consolidation happening.

The extension process for implementing Schedule M requires manufacturers to fill out a form detailing their current non-compliances, the money required, and the timelines for achieving compliance. The seriousness with which the regulatory authorities are approaching this is evident in the design of the form, which aims to discourage unnecessary extensions.

Discussion with a government official who stated that if a company cannot meet the quality standards, they should close their factory, as the priority is the safety of patients consuming the medicines, not the profitability of the business. This underscores the regulatory seriousness surrounding Schedule M.

Key market announcements

New Product / Order/ Launches

Bajaj Healthcare: Bajaj Healthcare acquires Genrx Pharmaceuticals for ₹10.85 crore.

BEL: BEL receives Rs. 2,210 Crores order from Indian Air Force.

Havells: Lloyd launches Luxuria Collection, expands AC manufacturing capacity.

Hyundai: Hyundai introduces new EX variant of EXTER Hy-CNG Duo.

Sunpharma: Sun Pharma launches Fexuclue® for Erosive Esophagitis.

Suprajit: Suprajit signs licensing agreement for ABS technology with Blubrake.

Fredun Pharma: Fredun Pharmaceuticals secures Rs. 150-180 million tender from TNMSC.

Madhav Infra: Received LOA for NH-146 project worth Rs. 323.82 Cr.

EKI Energy: Selected as Carbon Consultant for Varanasi Smart City project.

Greaves Cotton: Greaves Electric Mobility launches Ampere Reo 80 electric scooter.

ITI: ITI Limited initiates S-NOC for BharatNet Phase-III Project.

Prestige estates: Launch of 14 Mn sft residential projects across key markets.

Signature Global: Signature Global reports record pre-sales of INR 102.9 billion in FY25.

Aurbindo Pharma: Aurobindo Pharma receives final ANDA approval for Rivaroxaban Tablets.

Ashoka Buildcon: Emerged as lowest bidder for Central Railway project.

Zydus Life: Zydus receives USFDA approval for Jaythari (Deflazacort) Tablets.

NBCC: NBCC sells 560 residential units for Rs. 1153.13 crore.

Ola Electric: Ola Electric launches Roadster X motorcycle with advanced features.

Sky Gold: Secured 200 KG/month export order, enhancing capital.

CIPLA: Cipla receives USFDA approval for Protein-bound Paclitaxel.

Greaves Cotton: Greaves Cotton partners with Chara Technologies for rare-earth-free motors.

BHEL: BHEL signs MoU with Nuovo Pignone for compressor revamp.

Capex and acquisitions

Suraksha Diagnostics: Suraksha Diagnostic acquires 63% stake in Fetomat.

Global Health: Company received offer to acquire land for hospital.

Tata Power: Tata Power to install 100 MW Battery Energy Storage System in Mumbai.

Thomas Cook: Sterling launches Borderland Amritsar, its first resort in Punjab.

Metropolis: Metropolis Healthcare acquires Dr. Ahujas’ Pathology & Imaging Centre.

DP Abhushan: D.P. Abhushan opens second showroom in Ratlam.

Coromandel: Coromandel and Ma'aden sign MoU for fertiliser supply.

Zim Laboratories: Collaboration with Globalpharma to commercialize Oral Thin Film products.

Shilpa Medicare: USFDA approval for Varenicline Tablets, 0.5 mg and 1 mg.

EPACK Durable: Proposed capacity addition of 6,00,000 washing machines.

GRSE: Received Letter of Award for two Coastal Research Vessels.

Cochin Shipyard: CSL signs MOU with Drydocks World for ship repair clusters.

NTPC: 90 MW capacity of Dayapar Wind Energy Project operational.

Lemon Tree: Lemon Tree Hotels signs license agreement for new hotel in Siliguri.

Sasken: Sasken acquires 100% of BORQS International for $40 million.

Spectrum Electric: Signed MOU for Rs. 100 Crores expansion in Maharashtra.

CEAT: CEAT invests ₹345 Lakhs in Tyresnmore Online Private Limited.

Morpen lab: Morepen to add 1000 medical representatives for expansion.

Samvardhana Motherson: Motherson to implement cost optimization of EUR 50 Mn.

R&B Denims: Commencement of garment manufacturing business by R&B Denims.

SRF: Entire project commissioned and capitalized at Rs. 239 Crores.

Avalon: Avalon Technologies to invest in Zepco Technologies.

Deepak Nitrite: Approval for 3,500 Crores capex for new manufacturing facility.

One Source: OneSource receives Brazilian GMP approval for Unit 2.

Fund raise

One source: Approval of rights issue for 48.89 Cr equity shares.

RACL Geartech: Board meeting to approve fund raising through equity shares.

Change in Management

MM Forgings: Postal ballot for appointing Smt. Rama Sivaraman as director.

Pitti Engineering: Resignation of COO Varun Agarwal effective 7th April 2025.

Honasa: Resignation of Chief Marketing Officer Ms. Anuja Mishra.

Yatra Online: Resignation of CFO Rohan Mittal and appointment of Anuj Sethi as Interim CFO.

Others

M&M: Incorporation of Mahindra Advanced Technologies Limited as a subsidiary.

Rane Engine: Approval of amalgamation of Rane Engine Valve and Rane Brake Lining.

Rushil Deco: Fire at Atchutapuram MDF plant disrupts production.

LT Foods: Received Rs. 265 Crore insurance claim for fire incident.

Idea: Allotment of 36.95 billion equity shares to Government of India.

Raymond: NCLT sanctions demerger of Raymond Limited's real estate business.

Privi Speciality: Maharashtra government sanctions industrial promotion subsidy of 262.96 lakhs.

Mitsu chem plast: Mitsu Chem Plast aims for ₹1,000 Cr revenue by 2028.

Prestige Estates: Incorporation of Prestige Vaishnaoi Hospitality Private Limited.

Hindzinc: Vedanta Limited penalized for unauthorized disposal of fly ash.

Ceinsys Tech: NCLT approves amalgamation of Allygrow Technologies with Ceinsys Tech.

Goodluck India: Goodluck India reports strong volume growth in Q4 FY25 and FY25

Jyothy labs: Closure of Laundry Service Operations by April 30, 2025.

Elgi Equipments: Divestment of entire stake in CAST completed for $154,586.

Vadilal Industries: Vadilal Industries' credit ratings upgraded by India Ratings.

Dynamic cables: CRISIL upgrades credit ratings for Dynamic Cables.

VIP Clothing: VIP Clothing partners with Zepto for quick commerce.

JASH: Jash Engineering Limited has achieved revenue growth of 40% and projecting sales of 860 cr in FY26

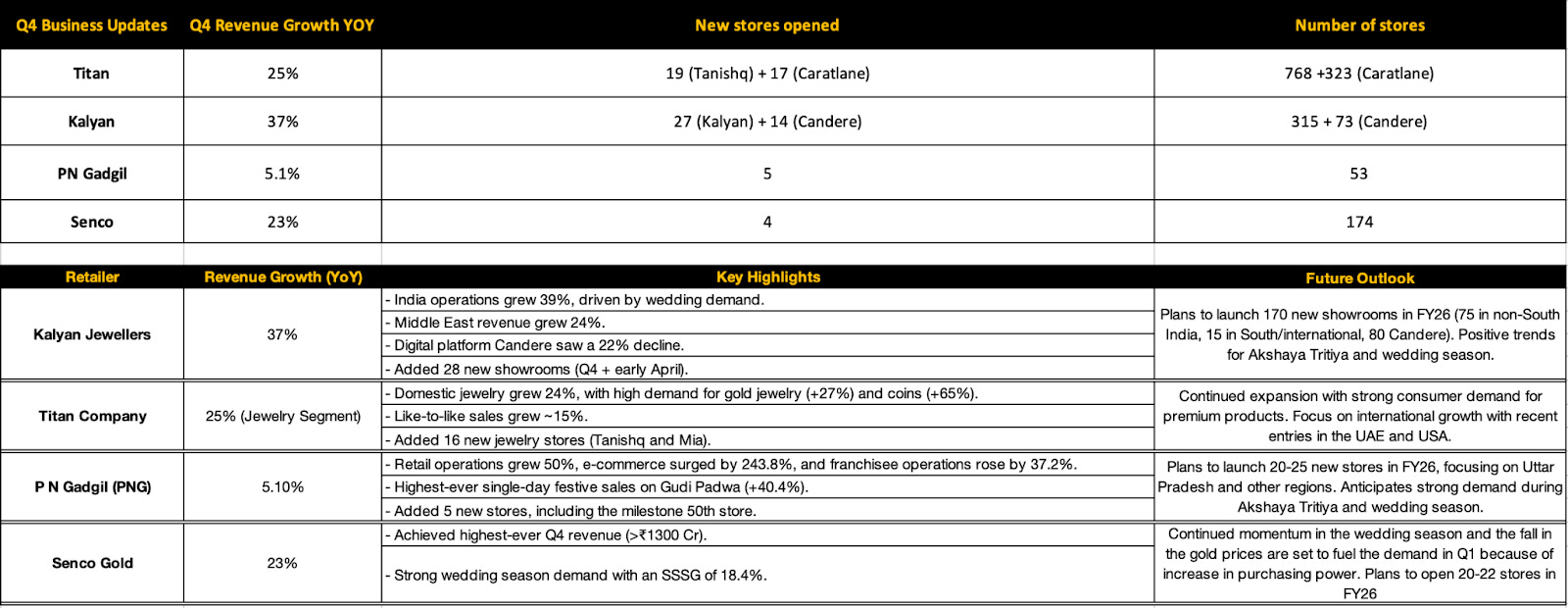

Peer to Peer comparison - Jewellery sector business updates

Strong numbers by most of the large retailers in the country. Also expectations of a good upcoming quarter led by the Akshay Tritiya and the continued wedding season in the next 2 months.

Key mental models and a book recommendation

This has a lot of very beautiful mental models that one can use in different scenarios in life and of course in individual stock picking. One of such concepts that is relatable to the current environment is “Chaotic systems and Butterfly effect”. Predicting the future behaviour of chaotic systems is difficult or impossible because modeling outcomes require perfect understanding of the starting conditions. Any inaccuracies can result in incorrect and drastically wide predictions.

The current tariff war situation is such where as much as you try to predict and quantify the situation the more it becomes complicated to understand and your predictions might vary from the actual outcomes.

Also, the “butterfly effect” that the small events sometimes are more than enough to turn the world upside down. We tend to assume systems are deterministic and tiny differences should not matter. Most of the time in day-to-day life situations it might be true but it’s false for the chaotic situations. Without perfect accuracy, we can’t make comprehensive predictions about them. It’s only possible to make probabilistic predictions. So for such chaotic situations one should not get into the game of prediction but make some probabilistic predictions and have insurance for such situations.

Share your feedback and thoughts in the comments below!

Disclaimer:

SOIC Intelligent Research LLP is a SEBI-registered research analyst with SEBI Registration No. INH000012582. Registration granted by SEBI and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors. Investment in the securities market is subject to market risks. Read all the related documents carefully before investing.

https://open.substack.com/pub/mdavis19881/p/trumps-tariff-catastrophe-and-the?r=19b2o&utm_medium=ios

Hello there,

Huge Respect for your work!

New here. No huge reader base Yet.

But the work has waited long to be spoken.

Its truths have roots older than this platform.

My Sub-stack Purpose

To seed, build, and nurture timeless, intangible human capitals — such as resilience, trust, truth, evolution, fulfilment, quality, peace, patience, discipline, relationships and conviction — in order to elevate human judgment, deepen relationships, and restore sacred trusteeship and stewardship of long-term firm value across generations.

A refreshing take on our business world and capitalism.

A reflection on why today’s capital architectures—PE, VC, Hedge funds, SPAC, Alt funds, Rollups—mostly fail to build and nuture what time can trust.

“Built to Be Left.”

A quiet anatomy of extraction, abandonment, and the collapse of stewardship.

"Principal-Agent Risk is not a flaw in the system.

It is the system’s operating principle”

Experience first. Return if it speaks to you.

- The Silent Treasury

https://tinyurl.com/48m97w5e