Understanding Capital Allocation with Deepak Nitrite

Understanding Capital Allocation with Deepak Nitrite

“It is a capital mistake to theorize before one has data. Insensibly one begins to twist facts to suit theories, instead of theories to suit facts”- Sherlock Holmes (A Scandal in Bohemia)

Lately, I have been thinking about how some investors only look at an opportunity only through the perspective of numbers, then there are others who look at charts to decide and there are very few who look at the bigger picture while investing. I believe that investing is a mixture of both Art and Science. The softer aspects like the quality of management, the ability to scale a business/ability to execute, and the willingness to share the wealth with the shareholders comes under the Art Part. Whereas, the valuations, return ratios and the past track record (numbers) come under the science part. Most successful investors I have interacted with, have always emphasized the importance of marrying the qualitative with the quantitative in order to be a successful investor. The purpose of writing this article is to do one such activity, where I will be laying out a Hypothesis about a business and I will try to marry both the qualitative and the quantitative in order to draw conclusions. The name of the business is Deepak Nitrite, and let’s see what we can learn by marrying the softer aspects with the hard science of investing.

1)Qualitative Insight 1-In the recent concall (Q3FY21), Maulik Mehta, who’s the CEO of Deepak Nitrite was asked about do they have any competitive advantage in manufacturing Phenol. The answer to this question was extremely interesting as Maulik Mehta used two very interesting mental models to answer this question i.e Theory of constraints and the Principle of inverting to answer. Let’s read the answer, I think these are live case studies and qualitative insights which we should remember.

Maulik Mehta: before telling you about our competitive advantage, I will start by telling you what our competitive disadvantage is. Our competitive disadvantage primarily if I am comparing to global marquee players, is that they manufacture Phenol and Acetone right next to their Raw Material Sources. So, normally they do it attached to a refinery. In many cases that allows them huge kind of latitude in the way, they plan their Raw material availability. Our greatest advantage was also the greatest disadvantage, we did not have a lot of capital that we could deploy and we did not have a lot of land that we could put this plant into. We took our theory of constraints in a very strong way. Therefore, we deployed our limited capital in an extremely conservative way. For us every Paisa was important, every square foot was important. What we were able to put up is a plant that has the lowest thermal footprint, lowest water footprint, and the maximum amount of phenol and acetone produced per square foot of Land.

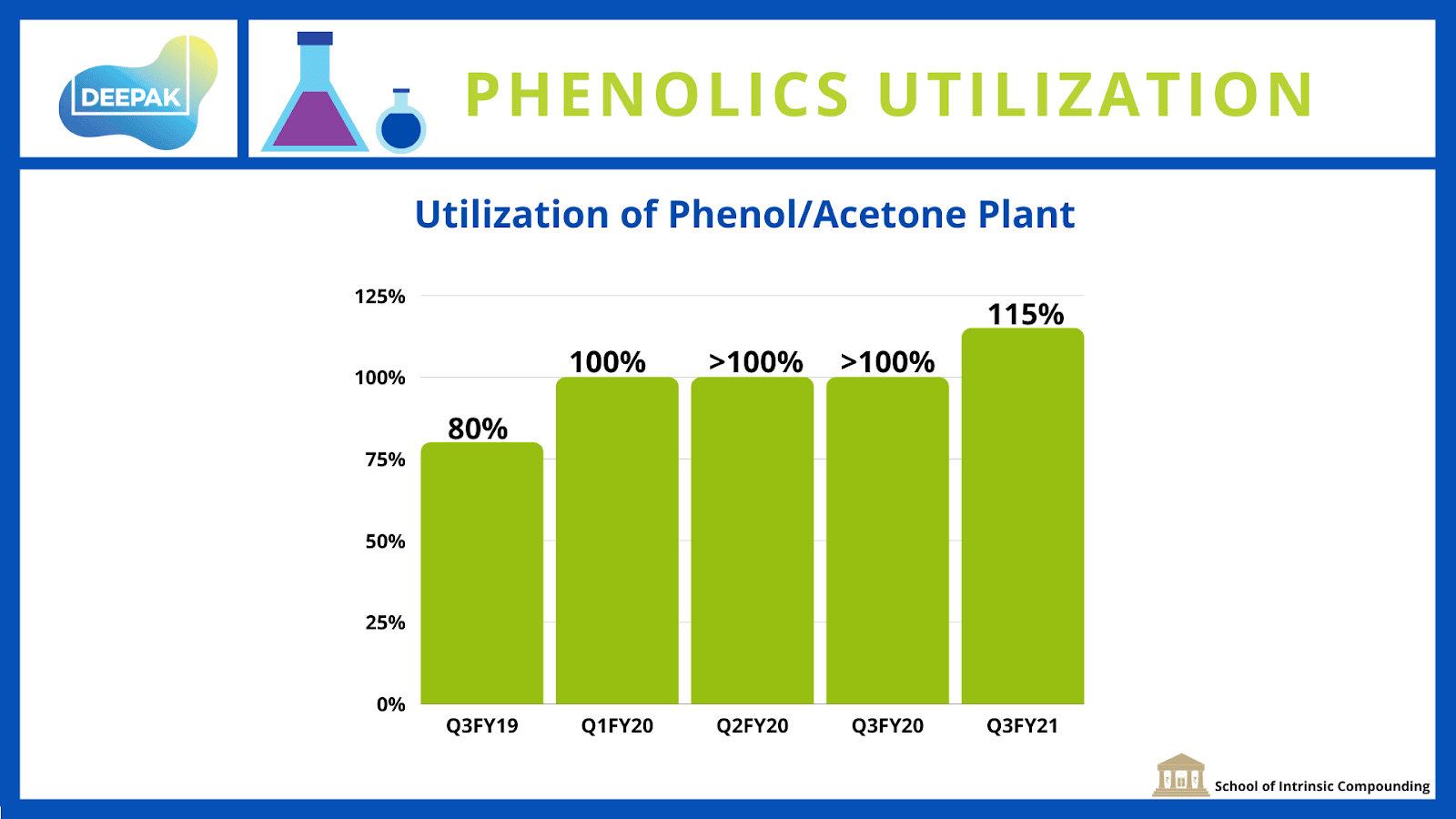

This was a qualitative insight into the thought process of the management as when they announced the 1400 crore Phenol Project, their Fixed assets were only at 500 crores back then. Now let’s search for proof in the numbers.

Numbers do the talking: at the time of commissioning the plant, Deepak’s management gave guidance on achieving capacity utilization of 75% in the first year, 85% in the second year & 95% in the third year(Q3FY19). Let’s see what has actually played out in the numbers:

Execution has been off the charts and moreover, they enjoy operational efficiencies as their Phenol Plant is 10-15% more efficient than the global competitors.

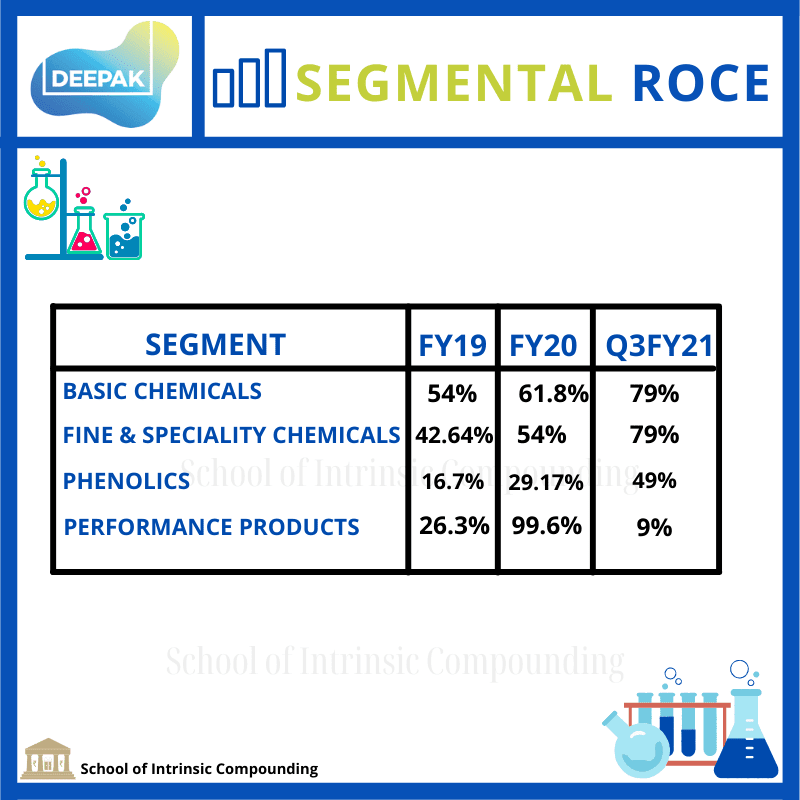

2)Qualitative Insight 2-Deepak Nitrite’s management understands capital allocation. Let’s read what they had to say in their earnings call.

“The way we choose Products is very rigorous which we call Deepak’s right to win. Any new product that we get into must have a payback period of 3 years. We have quintupled our R&D expenditure as we see robust set of opportunities.” (Q3FY21).

Numbers do the talking: The segmental ROCE numbers apart from the performance products business (which is cyclical) tell the story in terms of the product selection and the capital allocation framework of the management at Deepak Nitrite. (could look optically high as some of the segmental assets might be fully depreciated)

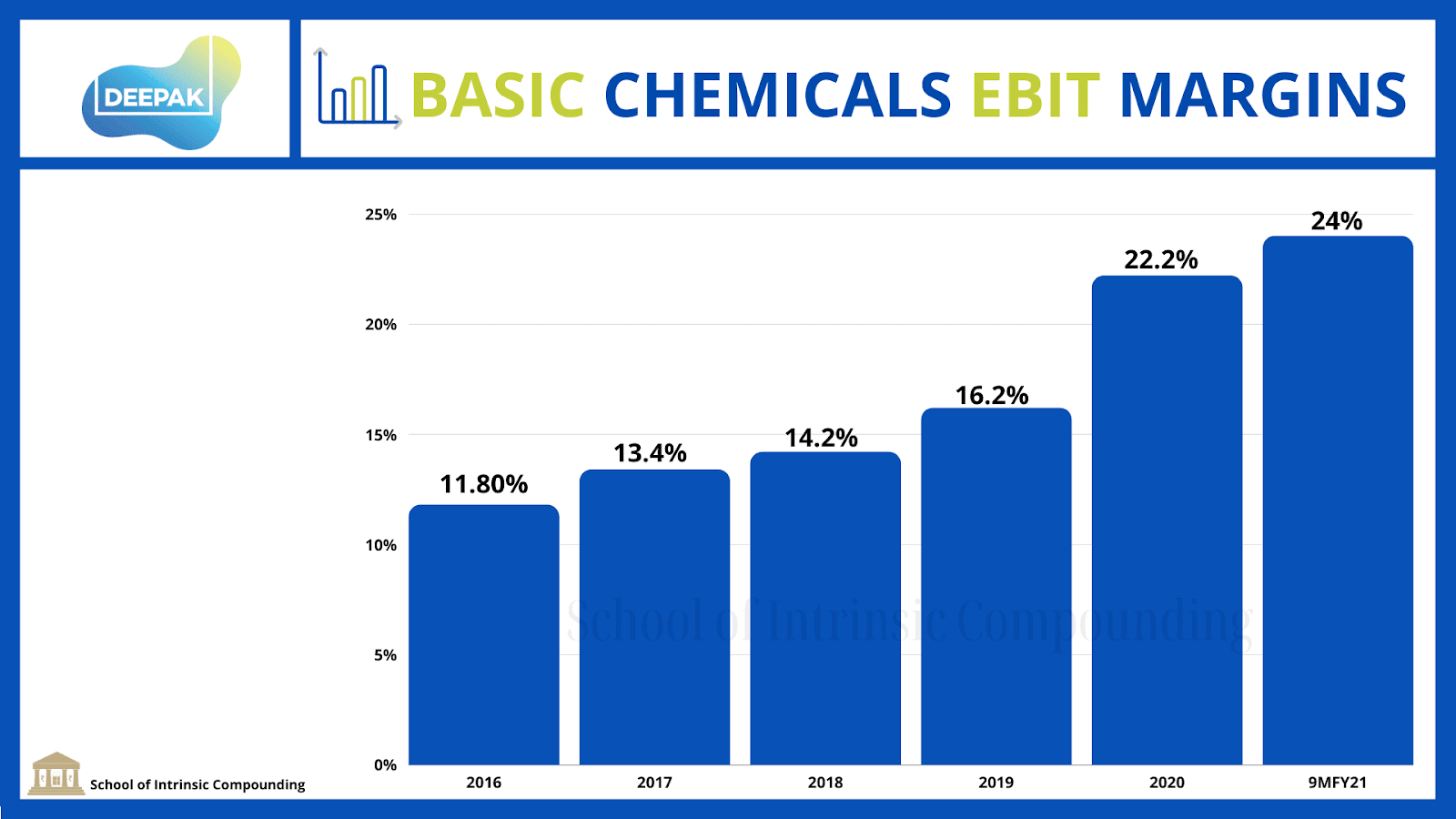

3)Qualitative Insight 3-Deepak Nitrite has Process chemistry expertise as they are aiming to combine the expertise of Deepak Nitrite with Deepak Phenolics in order to create new value-added intermediates. When they were recently asked about their efficiencies in the Basic chemical business, they replied that it’s been an effort of more than 50 years of looking at a boring set of numbers over and over again. Moreover, most of the products/intermediates that they will be launching will be in the agrochemicals and the pharmaceuticals space. Let’s see quantitatively how in their basic chemical business in spite of high volume products they have been able to maintain/expand their margins.

Numbers do the talking: in the basic chemical business, Deepak has taken several initiatives for improving the operational efficiency and to structurally improve the margins. Basic chemical business in most chemical businesses serves as the necessary feedstock to get into downstream products. Let’s check the margins of DNL in the Basic chemicals business:

-Qualitative Insight 4: Long-term thinking seen by the capex plans of the company, and identifying opportunities to create vertically integrated business verticals where one chemical feeds into another segment for a much higher margin product. (Think about the Fine&Speciality Ebit Margins of 40-44%).

Numbers do the Talking: DNL has recently acquired a 127acre land Parcel at Dahej which they will develop over the next couple of years. Deepak Nitrite has also announced a capex of 600-700 crores for FY22, and they have recently quintupled their expenditure on R&D coupled with new value-added intermediates which will be launched in Deepak Cleantech.

This is one example of how one can marry the Quantitative with the Qualitative. Repeating this exercise over and over again with different businesses and management can help us partner with strong managements who walk the talk early in the journey of wealth creation.

Disclosure: Nothing on this website should be construed as investment advice. Please consult your financial advisor. We are not SEBI registered Analysts/Advisors. We are not accountable for any loss or gains that might occur to you from this or any analysis on the website. The author holds the stock as a core position in the portfolio, his views can be biased.